Profits: Optimistic Wagers and Preserving Self as the Party Rages

New Federal Reserve Chairman Kevin Warsh certainly doesn’t want to have problems with President Trump. On the 17th of June the FOMC meeting via the Fed will make their interest rate decision known. Who really believes that during the first month on the job at the helm of the U.S central bank that Warsh is not going to fight to keep interest rates in place?

Those who are expecting an interest rate hike in June of a quarter of a point (0.25%) are most likely wrong. Yes, the price of WTI Crude Oil is high and the situation in Iran via narrative varies from one moment to the next per the reported incidents on the Strait of Hormuz.

However, just like the Fed there is a certain amount of reality that must be dealt with regarding human nature and behavioral sentiment regarding Iran and how it is dealt with via market participants. From the department of no news is good news: financial institutions and investors would like the noise to be kept to a minimum so they can continue doing their jobs and not be criticized themselves for potentially wrong outlooks. The art of making sure disclaimers are up to date is important for everyone who wants to stay employed.

WTI Crude Oil 1 Year Chart as of 1st June 2026

USD centric weakness was seen late last week in many currency pairs, but a quick glance at the majors: EUR/USD, GBP/USD and USD/JPY actually show the pairs traversing rather cautious values. The EUR has gained slightly for instance, but at its current levels around 1.16410 some may believe it is a safe equilibrium. (One that may be able to be taken advantage of by those with the ability to bet on mid-term higher trajectories).

Central Banks globally also want to keep the noise down in their various locations. Inflation concerns persists worldwide depending on the amount of knock-on effects that higher energy costs have on national economies.

Also adding additional intrigue to the storyline of wanting to keep quiet while volatility threatens the gates, is that many people with comfortable jobs in various government institutions do not want to step out of line and sacrifice their careers for the sake of being proven right. They would rather be proven wrong, but would like to do this quietly without facing consequences.

The fact that we are now in a situation in which we are afraid to undertake critical thinking aloud is going to cause problems down the road, but for the moment most will simply go on with their various duties and pretend all is well.

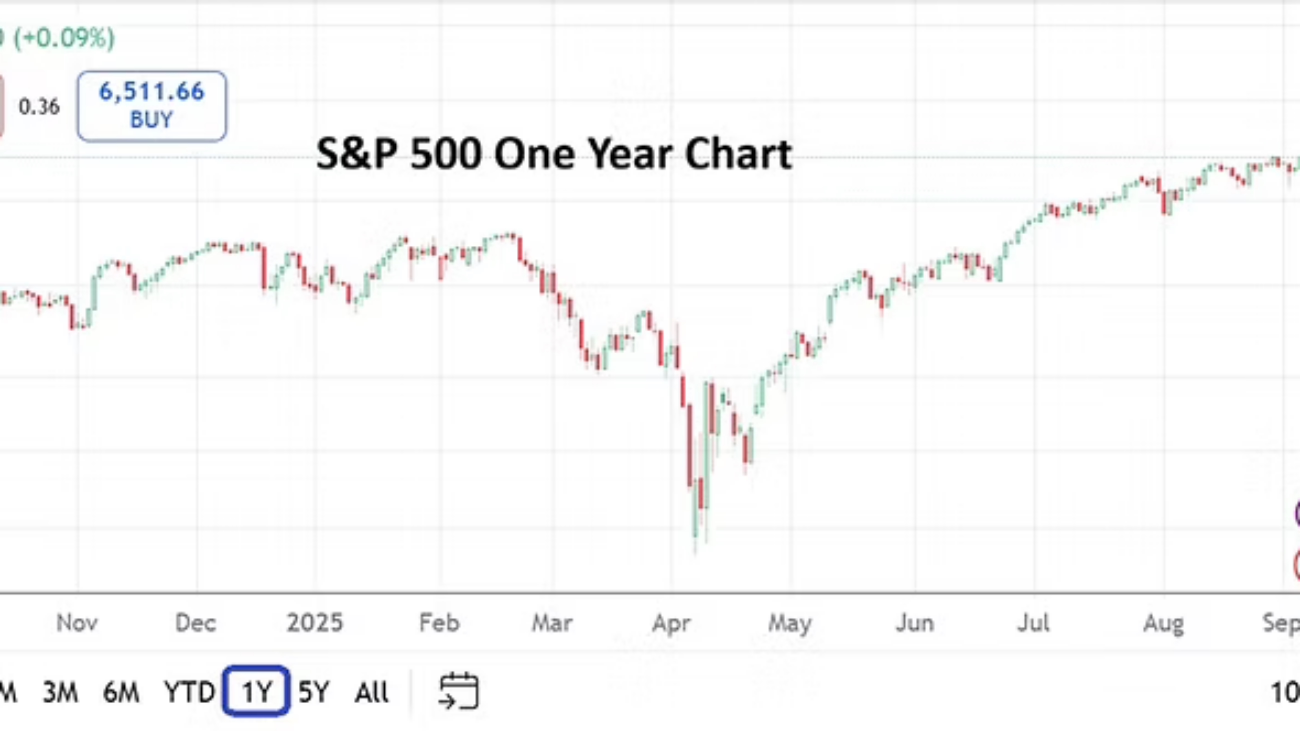

U.S equity indices have been having a massive upwards party since the end of March as record heights are attained. Certainly some long-term investors are simply throwing money into indices as a way to get positioned before the SpaceX IPO which is coming soon. There will also be the Anthropic IPO which is reportedly set for late 2026.

The SPCX which seems to be aiming for the 12th of June will create a valuation well above 1 Trillion USD for SpaceX. The perceived value of Anthropic is becoming a loud talking point among analysts in the tech sectors and they are keen to have the company join the 1 Trillion USD party. The cost of admission for bragging rights is getting more expensive.

There was a time when things like PE (price and earnings) ratios mattered on Wall Street. Some brave folks still whisper about such things in meetings and bars late at night, but many do not want to be insulted or possibly worse get marketing folks selling these high priced products angry. The reason for speaking softly about actual earnings regarding SpaceX is because the company is actually working via an earnings loss, and instead price to sales estimates are being offered as some type of guideline. Having said the above, it would be foolhardy to bet against SpaceX and Elon Musk. And it might be equally unwise to bet against Anthropic in a handful of months. And thus, the rush into equity indices because there is a genuine fear of missing out does exist. Afterall, we all want to be part of the party.

And that brings us back to Fed Chairman Kevin Warsh who has the backing of President Trump and Treasury Secretary Scott Bessent, he doesn’t want to insult these men either. Warsh may be quite good at what he does, he might be an expert and have real world business experience, and that might be a real clue for Forex traders who think higher interest rates are coming. Warsh will likely want to keep his first months on the job at the Fed on good terms with the White House and the Treasury. Kevin Warsh might be a free-thinker and know legally he is an independent leader of the Federal Reserve, but he also knows he was hired with a stated mission. There is a pro-business, free enterprise administration in power at the White House. Bessent, Warsh and Trump are on the same team.

So again, while some traders may believe the Fed will raise interest rates in June because of concerns of higher inflation, it most likely will not happen. While the Iranian war continues to make headlines in the financial world and dealt with via sentiment decisions, actual economic U.S data will start being watched in the coming days and weeks and might even influence perspectives. Investors will get bored of the Iranian saga as long as its narrative stays somewhat tepid. Meaning investors will start looking at CPI and PPI numbers coming from the U.S next week and talking about higher interest rates that will likely not be delivered in the upcoming FOMC meeting.

The price of WTI Crude Oil as boring as it is to say remains a strong sentiment gauge for traders intraday. Large players involved in Forex might believe this will involve higher interest rates, but on the 17th of June it is more likely that Kevin Warsh will say that for the moment the Fed chooses to watch energy sector costs with the belief prices will decline in the coming months. The Fed will not use the term ‘transitory’ which was used infamously during the Covid crisis and turned into a poison pill with inflation that was not effectively fought. What the Fed will likely do is say they want more info to be gathered and more clarity regarding the Iranian situation and its overall effect on oil prices for a little while longer. Some patience will be asked for and it might be granted by investors who want the party to continue via equities.

Day traders should expect cautious markets to prevail in Forex with choppy results as financial institutions weigh their behavioral sentiment and try to make believe they are not too worried about near-term inflation. The CPI and PPI readings next week will prove of interest, but the results may be brushed aside by market pundits.

In the meantime, the celebrations on Wall Street continue as folks march merrily into the frenzy. Retail speculators who want to pursue short or near-term profits on the Nasdaq 100, S&P 500 or Dow 30 indices need to be careful and might want to stay away from daily bets and instead engage in conservative positions that allow for a full week of results. The gains made since the end of March have been outlandish and likely will not be repeated anytime soon, but why try standing in front of a trend that can crush you.

Near-term considerations in these markets should be done carefully. The mid-term may be very different from where we stand today and our current outlooks. One thing that may bother some risk analysts is that it may prove wrong to bet against the current parade of optimists who insists on participating in dangerous conditions and profit, while they (the risks mavens) stand in place.