New Federal Reserve Chairman will Cause a Reaction in Forex Today

I offer readers a ‘what if’ proposition ahead. These are my opinions and I am simply trying to give my perspective on what may happen in the Forex market in the coming hours.

The Fed Press Conference later today will be must watch television for Forex traders, including retail speculators, large players and financial institutions. Federal Reserve Chairman Kevin Warsh will make his first appearance after a FOMC rate decision. Dynamic conditions in the broad Forex market should be anticipated – that doesn’t tell day traders much I know, keep reading, please.

U.S inflation has sparked higher this as energy prices have ignited upwards and caused logistics, manufacturing and agriculture to become more expensive. The Bank of Japan raised its interest rate by a quarter of a point yesterday to 1.00%. However, these two bits of evidence doesn’t mean the Federal Reserve will increase its interest rate today.

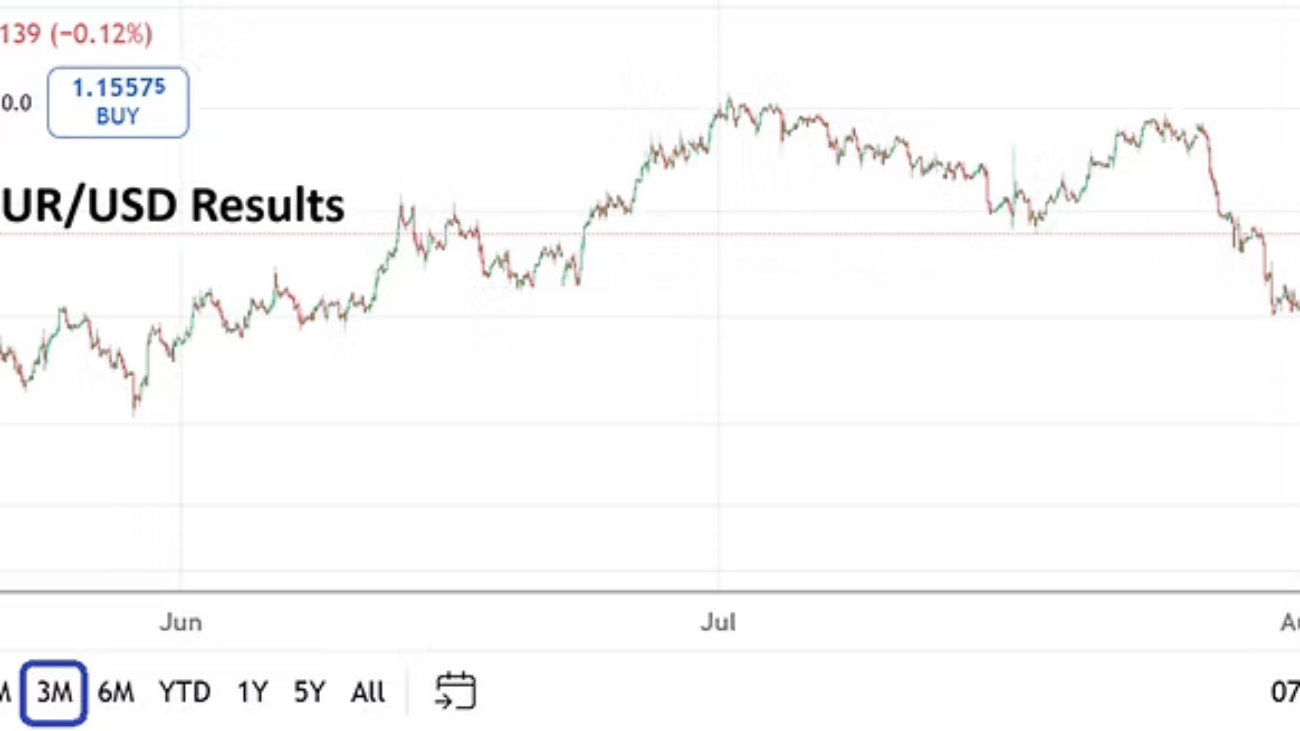

The U.S Dollar Index is trading near relative highs. The broad FX market is certainly cautious, but financial institutions may be leaning into the notion of USD centric weakness. Yes, the USD/JPY remains above 160.000+ for the moment, but the USD/SGD is flirting with its lower range and came within sight of the 1.28000 mark on Monday. So why is this important? Because folks are acting cautious before a potential storm.

U.S Dollar Index Six Month Chart as of 17th of June, 2026

Perhaps this will go down as an infamous egg on the face situation for me personally, but does Fed Chair Kevin Warsh really want to raise interest rates during his first FOMC meeting at the helm? Yes, Jerome Powell is still around as a voting Governor, but Warsh may find he has enough votes (and influence) to get a majority of other FOMC voting members to allow today’s decision to be a test case in favor of patience.

If the Fed holds the Fed Funds Rate in place and announces it will use the near and mid-term as a trial period regarding their belief inflation will lessen, because it believes energy prices over the mid-term will erode rapidly, that may be enough to cause USD centric selling later today. The Fed will not use the word transitory I suspect, but an argument can certainly be made that now is the time to actually elucidate on the subject of transitory inflation.

Monday’s trading in the broad Forex markets showed that financial institutions bought into the optimism of an anticipated U.S and Iranian agreement and what it could deliver – a glut of Crude Oil, including lower costs for its ancillary products. Financial institutions were also relieved that U.S equity markets survived the launch of the SpaceX IPO certainly. While yesterday’s broad market trading turned cautious and demonstrated sideways action in Forex, many major currencies are traversing near curious values. Equities also went sideways for the most part on Tuesday.

The U.S Dollar Index is swimming within its higher terrain via a six month chart (per a look above), yet financial institutions – if they hear dovish sentiment from the new Fed Chair today could spring into action and sell the USD quickly. Day traders need to understand even if this occurs that it will still be ultra-dangerous to bet ahead of the Fed rate announcement and Press Conference. This because volatility leading up to and following the FOMC Federal Funds Rate decision will create large spreads in Forex and choppiness that small retail accounts cannot handle most of the time – particularly when too much leverage creates wildfires.

While the before and after of the Fed interest rate announcement will garner the headline news, and create a reaction on Wall Street for the S&P 500 and Nasdaq 100 immediately; it will be wise to pay attention to Fed Chairman Kevin Warsh a half hour later when he steps into the spotlight for the first time. There has been chatter that Warsh is not keen on trying to give too many signals regarding the Fed’s thinking regarding every move it is contemplating.

This coincides with thoughts that Kevin Warsh and Scott Bessent believe in a more high-tech and pro-active approach to interest rate and monetary policy based on forward looking data. The consideration of a more dynamic approach to interest rates has not been widely considered by financial institutions quite yet. If the new Fed Chair surprises reporters and onlookers at the Press Conference today with a new philosophy on the way the Fed will work, this will set the stage for potentially large behavioral sentiment shifts that were not wagered on quite yet. In other words mid-term outlooks regarding U.S interest rate policy may change in a handful of hours more than many people think.

Maybe I am wrong, maybe I am interpreting the political and financial landscape incorrectly, but these are my thoughts as a risk analyst – one who thinks the U.S White House would not mind seeing a weaker USD, a Fed that likely wants a different approach to interest rates – as they both hope for energy prices to lower (and may get their wishes fulfilled).