AMT Top Ten Miscellaneous Entries for the 22nd of March 2024

10: Jefferson: Jon Meacham’s Thomas Jefferson The Art of Power provides well written historical and psychological insights concerning one of the U.S Founding Fathers.

9. Shohei Ohtani: Major League Baseball has a gambling scandal. Claims that Ohtani’s interpreter ‘stole’ over 4 million USD from the player to pay off gambling debts beg for questions.

8. Saudi Arabia: The nation has announced it plans on investing 40 billion USD into Artificial Intelligence sector companies via its Public Investment Fund (sovereign wealth fund) and potential business partners.

7. Steve Jobs: Apple’s innovation and tech leadership appears to be weakening as the absence of its deceased leader fades into memory, and competitors grow.

6. Bank of Japan: Monetary policy was finally shifted on Tuesday, an interest rate of 0.10% was instituted, today’s National Core CPI data came in at 2.8%. USD/JPY is currently around 151.400 suggesting financial institutions believe the BoJ Policy Rate may have to be raised again.

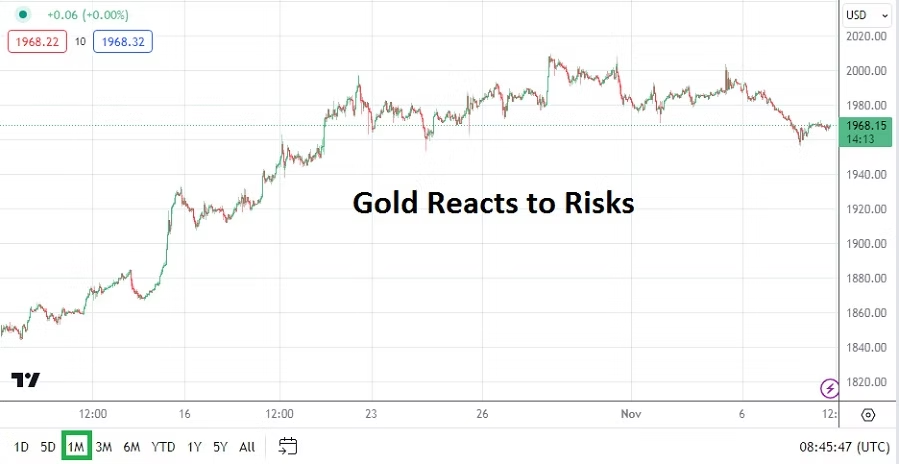

5. Gold & Forex: The precious metal challenged 2223.00 USD on Wednesday after the Fed’s FOMC rhetoric but is trading near 2165.00 as of this morning, this as the USD has gotten stronger again producing FX volatility.

4. Hot Chocolate: Cocoa finished yesterday at 8477.0 USD per metric ton, the commodity cost 2880.0 USD one year ago. What and who are manipulating the market?

3. China: Official Foreign Direct Investment statistics are supposed to be released soon. China argues that the fall of foreign investment capital is being reported with bias and not taking into consideration the impact of coronavirus, global monetary policy changes, and cyclical investment fluctuations. However, the FDI numbers remain troublesome and should be watched.

2. Risk Appetite: Major U.S equity indices including the S&P 500, Nasdaq Composite, and Dow Jones 30 are challenging record highs as behavioral sentiment remains exuberant, along with Japan’s Nikkei 225.

1. Interest Rates: The Federal Reserve has hinted three interest rate cuts ‘could’ happen this year, this while inflation in housing, transportation and food remain significant for U.S consumers. The Fed seems to be indicating it believes U.S jobs data will get worse. Political shadows hover over the central bank as the presidential election draws closer. The Fed only has 6 FOMC meetings left and appears to be playing with fire.