Friday Barometer Regarding the BoE Decision and Gold Prices

The Bank of England’s rate hike of 0.50% cements the notion that global central banks remain steadfastly locked on inflation, and understand politically the implications on the public regarding higher consumer prices which are being experienced. The Bank of England ‘met’ before its Official Bank Rate announcement with corporate bank executives it was whispered, to discuss their concerns regarding the knock on affects of higher mortgage rates to come. However, this did not stop the BoE from being aggressive.

GBP/USD Three Month Chart as of 23rd June 2023

Is the BoE Move a Sign Regarding the Fed’s Next Decision?

The move by the BoE also is intriguing because the larger than expected hike puts into play the notion the U.S Fed may be raising the Federal Funds Rate in July. The reasoning is based on the idea the Bank of England wants to protect the British Pound from another interest rate hike from the Fed, thus ‘securing’ the value of GBP/USD Forex mechanics.

The U.S Federal Reserve, the BoE and ECB finally seem to have a grasp on import inflation implications. Although higher costs and dynamic pressures on exporting countries like China, India and others that face the gauntlet of these challenges remains critical, because these nations need to raise the costs of manufactured goods internationally when they sell.

Smart Money and the Value of Gold

Let’s talk about ‘smart money’ for a moment surrounding Gold – and please try to hold down your laughter – but the price of the precious metal is interesting and should be monitored even by folks who do not trade the commodity. Gold as of this morning is near the 1915.00 USD ratio.

Gold Six Month Chart as of 23rd June 2022

On the 4th of May the price of the precious metal momentarily challenged the 2080.00 level. On the 1st of June the price of the commodity was near 1985.00. Do you see a trend here? Please note, Gold isn’t going to zero.

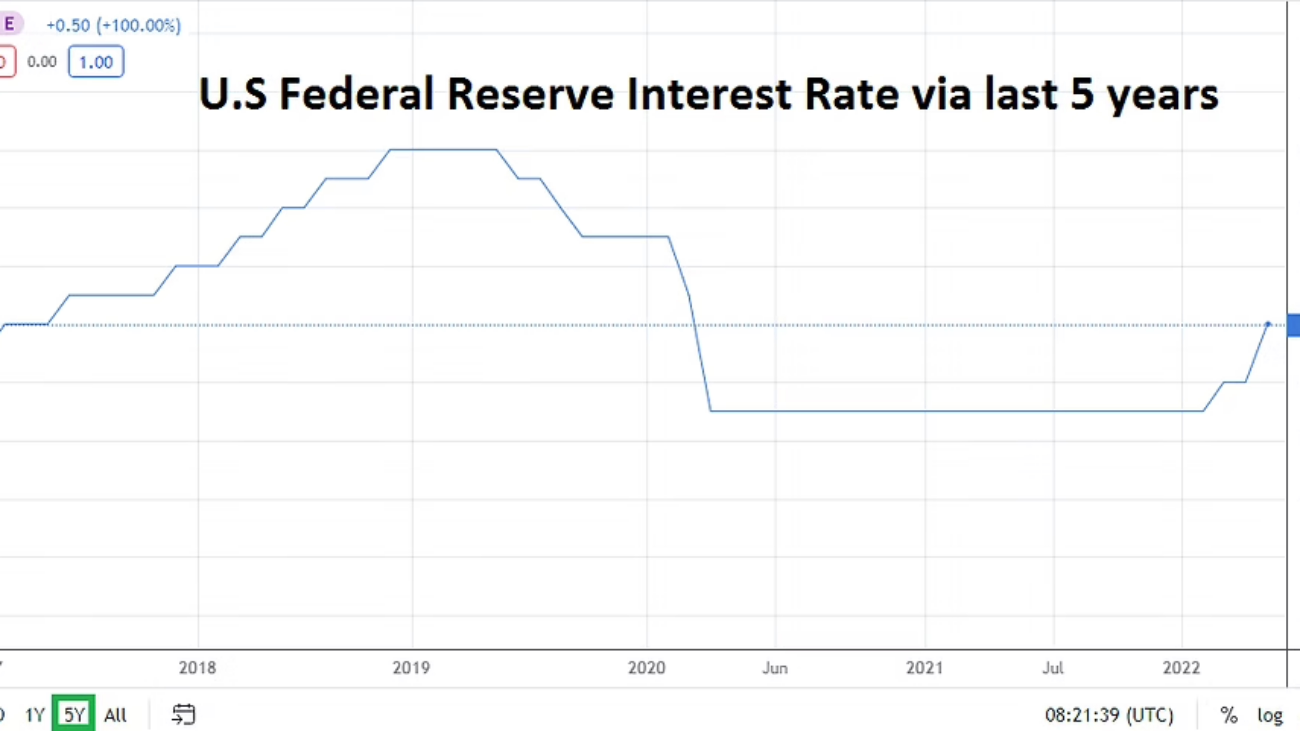

The point to be made is that the build up in the price of the precious metal from the 22nd of November 2022 when Gold was around the 1625.00 USD per ounce level, until early May anticipated the U.S Federal Reserve was going to become more dovish regarding their interest rate polkicy. For consideration look at the price of the USD during this time too, against many major currencies – the value of the USD also started to come down.

‘Smart money’ is showing signs of nervousness certainly since the start of June that more hikes are feared from the Federal Reserve. However, the price of Gold and the USD are not correlating well at this moment. This is a potential sign that Gold and the USD are both within speculative trading zones in which financial institutions are seeking ‘true’ equilibrium and are not comfortable. Fragility in the financial marketplace is likely to be seen until the Federal Reserve Federal Funds Rate announcement late in July. Expect financial institutions to price in their outlooks respectively depending on their outlooks.

Gold and U.S Treasuries: Inverted Interest Rate Implications

Gold definitely fluctuates within daily trading conditions, it is a speculative commodity, but it is also a solid barometer of risk management among the elite. If financial institutions are in favor of buying items like U.S bonds because of their guaranteed short term interest payments (look at the fact U.S Treasuries are mostly inverted – meaning shorter term bond interest rates are paying higher returns compared to longer term bonds) instead of buying Gold as an investment tool.

The Gold and USD Forex dynamics tells us that investment institutions are still very nervous about the Fed potentially raising interest rates a couple of more times this year. July and late this year appear to be reasonable bets. This Fed consideration and concern remains legitimate while looking forward as long as inflation remains elevated in the U.S. However, the Federal Reserve must also feel comfortable they will not kill mid and small sized banks, which by now should have shifted their business practices allowing for slightly higher interest rates to be delivered.