The Return of AMT's Top 10 Illustrious 'Weekly' Salvos

First we must congratulate those who were willing to climb out from under their rocks (and bomb shelters) to offer musings. But let’s not digress….. to the AMT Top Ten List we go.

AMT Top Ten for the 22nd of March 2026

10. March Madness: The NCAA Men’s Basketball Championship is underway. Some of the more hated schools remain catalysts. Our pick, the University of Arizona Wildcats.

9. Bitcoin: Traversing above 68,000.00 USD currently almost feels like an accomplishment considering BTC/USD was near 63,000.00 in early February and again in early March. But do not blink your eyes. BTW, MSTR (the much loathed MicroStrategy by some AMT folks) went into this weekend below $136.00 per share.

8. South Africa: The USD/ZAR finished Friday near 16.96800 depending on bids and asks. On the 29th of January the currency pair was close to 15.65000. The South African Rand has done well over the long-term, but it is correlating to the broad Forex market concerns. Day traders should not take things personally, and accept that risk adverse moves – particularly as a major war rages is part of speculation. Near-term viewpoints can differ with long-term prospects.

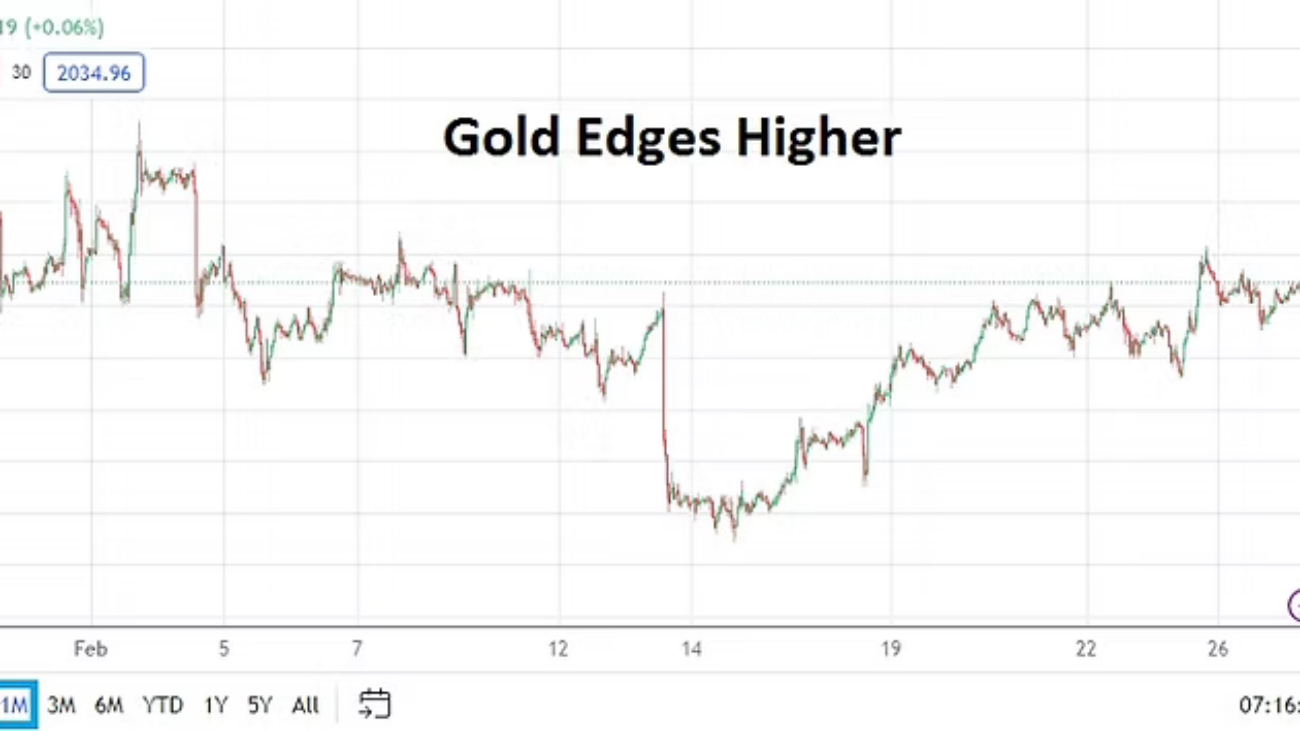

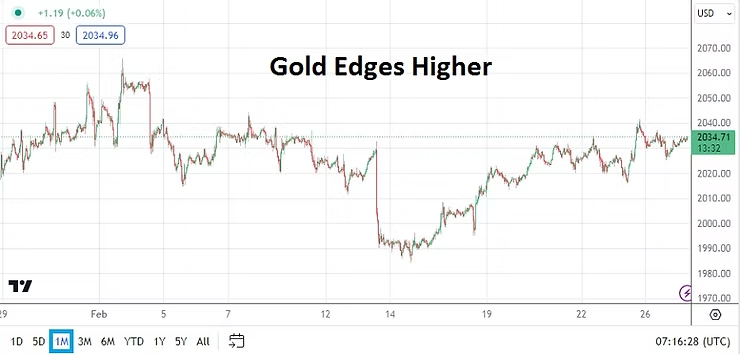

7. Not Glimmering: Gold at the start of the Iranian war was around $5,260.00, it has fallen to a mark of $4,491.00 this weekend. Showing gold’s speculative momentum beforehand hand, outmatched current values. Where next?

6. Silver: Above 120.00 USD briefly towards the end of January, the commodity is below 68.00. Wild betting has caused a drop of more than 42%. Too much exuberance.

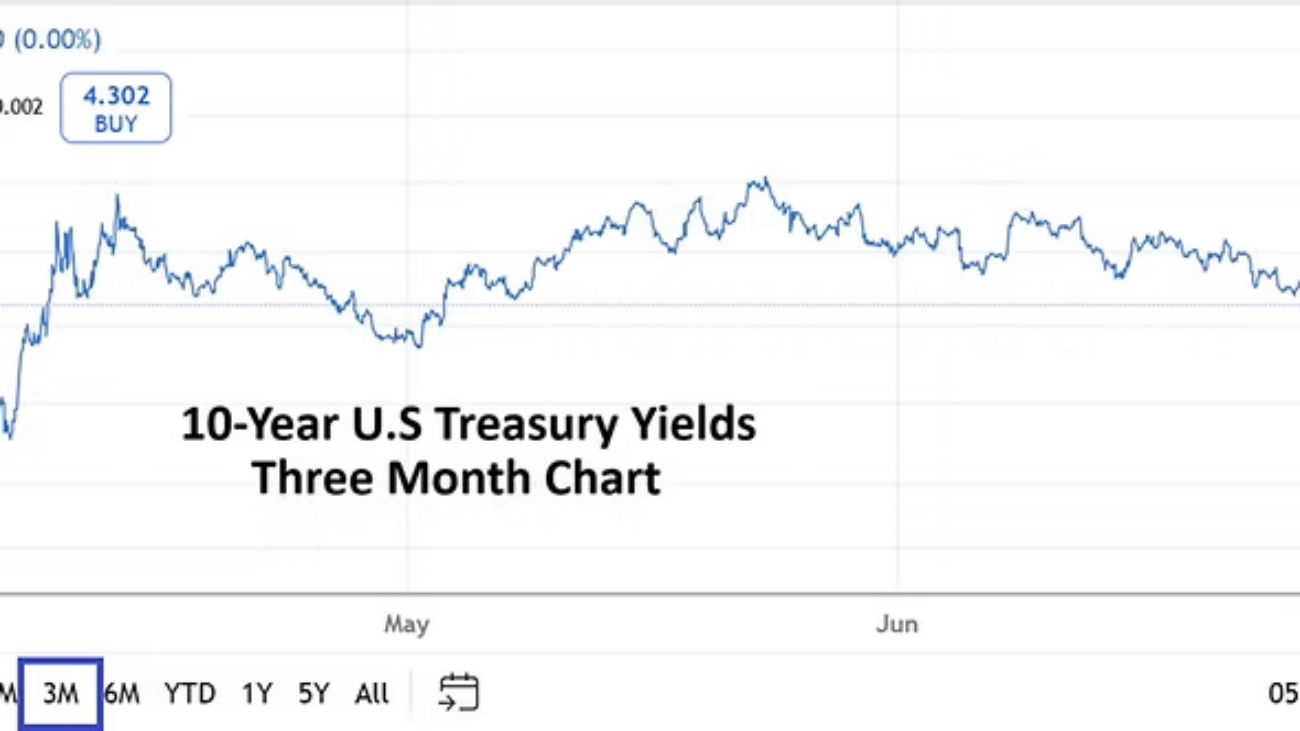

5. Risks: U.S 10-Year Treasury Yields were below 3.95% on the 27th of February, via Friday’s close rates are above 4.38%. Can you spell f.e.a.r?

4. Safe Haven: The U.S Dollar Index which had been showing solid downside is near 99.500, on the 27th of February it was around 97.850 – a rather legitimate rise. 100.000 may be a target by some large players.

3. Shrieking Hyperbole: WTI Crude Oil prices are certainly getting plenty of attention. However, voices expressing concern about WTI touching higher values starts to sound like an auction in order to get attention for the circus barkers. WTI remains near 100.00 USD and this mark is a barometer. The price is high and it can go higher, but expressed fear about $140.00 and $200.00 should be treated with disdain in the near-term.

2. Iran War: The conflict in the Middle East cannot be downplayed, but it can become fearmongering by Cassandras’. The U.A.E is still open for business and other nations in the Middle East are functioning. Yes, there is noise and the situation can grow more dangerous. But the potential of freedom for the people of Iran is a solid goal, though some may find this naive until it is proven. Can it become fact?

1. Coming Attractions: U.S stock markets are rightfully nervous. Friday’s close for the S&P 500 has brought it into terrain that challenges its 200 day moving average. The combination of weak technical attitudes and behavioral sentiment is a dangerous mix. Risk management may not be enough for day traders to survive current conditions, sitting on the sideline instead of betting on equity indices intraday may be more efficient and less lethal.