USD/INR: Elevated Range as Questions about Values Persists

The USD/INR has traded the past week approximately between the 82.2200 and 82.7000 ratios. Plenty of discussion regarding what the Reserve Bank of India has been doing as they battle the strong USD has been whispered openly, and is being questioned from financial institutions and speculators. Day traders who have been trying to wager on the value of the Indian Rupee have likely found the waters difficult to swim. As of this writing the USD/INR is near 82.5200.

USD/INR Three Month Chart as of 8th June 2023

Last Wednesday’s sudden rhetoric, from two U.S Federal Reserve officials caused mayhem briefly within the USD/INR. The currency pair got hit after India’s official trading hours closed, and essentially moved in overseas accounts based on the spoken words from the two Fed members stating the U.S central bank should not raise the Federal Funds Rate on the 14th of June. These sudden Forex moves hurt many USD/INR speculators. After this rhetoric from the two well-regarded FOMC members, like clockwork U.S economic data provided a counter punch last Friday with better than anticipated Non-Farm Employment Change numbers, this while inflation results also remained persistent.

Three Month View of the USD/INR offers Sentiment Insights and perhaps Clues

The past three months of trading in the USD/INR have produced a rather rocky price trend. A low of nearly 81.5200 was seen on the 14th of April, which turned into a high of approximately 82.9000 on the 19th of May. Intriguingly while many USD/INR speculators may be looking at the U.S Federal Reserve and casting blame, questioning the potential interventions by the Reserve Bank of India remains relevant. The Reserve Bank of India has actually been rather tranquil regarding its use of interest rate hikes; it has not raised the key lending rate aggressively in India like many of its major global counterparts. Why is this?

Is there a potential the Reserve Bank of India and the government has wanted the Indian Rupee to get weaker? Deflating the Indian Rupee’s value in order to potentially create an unseen tax is considered an old trick by economists. This because some believe inflation is a way to tax people without actually raising interest rates, the deflated value of a currency makes it easier for governments to sometimes repay debt, based on the notion the money they are now using is cheaper compared to when the Indian Rupee’s value was better.

Where is the USD/INR Going to Go Next?

I am no economist; my specialty tends to be risk analysis. There is an old joke, ‘why did god create economists? To make weathermen look good.’ The point is that economists often get their outlooks wrong, but we cannot blame only economists for getting their outlooks wrong, many of us do. The USD/INR has a tough few days ahead, it must deal with nervous market sentiment generated from a lack of clarity via the U.S Federal Reserve. Looking for correlations in the Forex market is proving difficult for the moment for all short-term speculators. Choppy trading in the USD/INR has been noticeable the past few days, this Monday’s upwards trend has turned into near-term consolidated day trading. Other major currency pairs are turning in rather turbulent results also without a firm technical stance.

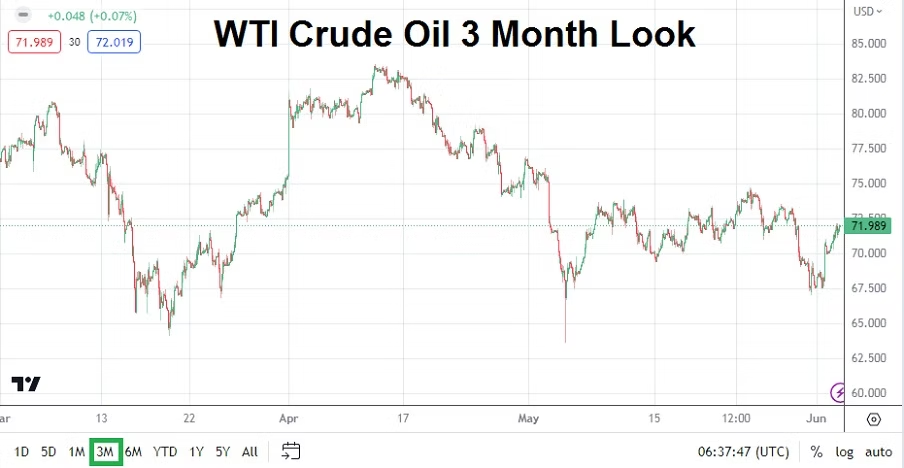

Gold Three Month Chart as of 8th of June 2023

After speaking with many associates in the financial sector the past week, it appears many people believe the Fed should stop raising interest rates for the time being. Some financial institutions seem to be leaning in this direction, but there are caution signs all over that warn about potential surprises from the U.S Federal Reserve.

Yesterday the Bank of Canada raised its Overnight Rate by another 0.25%, when most analysts believed they would pause. Another interesting sign is the current price of Gold near 1950.00. The recent lower price could indicate some financial houses believe the Federal Reserve may actually remain active regarding further interest rate hikes, this because the price of Gold has tended to rise when the perception existed the Federal Reserve is going to be dovish. Gold’s downward price action should raise suspicious eyebrows.

But then again, I am not an economist; I am merely a risk analyst. So my words to you are, be careful if you are wagering on the USD/INR before the U.S Federal Reserve’s pronouncements next Wednesday on the 14th of June.