AMT Top Ten Miscellaneous Raindrops for 16th of February

10. Bitcoin is trading within sight of 52,000.00 USD, the digital asset was trading near 38,700.00 on the 23rd of January, which is over 34% in less than a month. That’s a lot of air in the balloon folks.

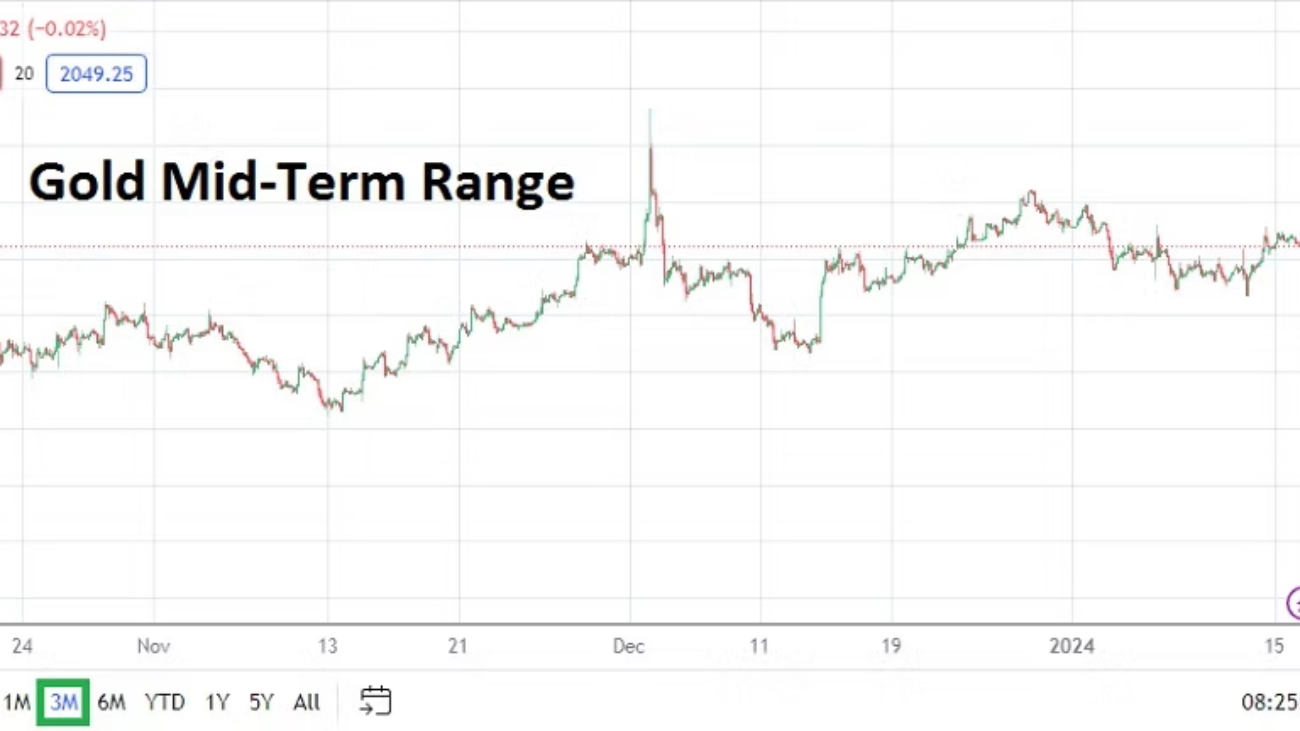

9. Gold: The precious metal has climbed above 2000.00 USD, this after a drop to 1985.00 USD on the 14th of February. Sentiment is uneasy.

8. Not April Fool’s Day: Iran has announced ‘plans’ to build a naval base on Antarctica, after declaring ‘property rights’.

7. WTI Crude Oil: The price of the commodity continues to battle the 77.00 USD level. Higher energy costs will not be looked on favorably by inflation hawks.

6. U.S Treasuries: Yields should be watched today after having provided anxious results this week, U.S equity indices will continue to react to the ‘bonds’ market.

5. Nvidia: After delivering superlative results in 2023, the company has announced the release of Chat with RTX, which allows independent AI chatbot capabilities to interface with your own documents, videos, etc., providing insights from personal queries.

4. Chinese Property: Investments dropped by over 9% in 2023. China’s government faces a clash between socialistic ideology in order to help the market versus practical supply and demand realities.

3. U.K: Gross Domestic Product numbers came in with negative results yesterday for Britain, the combination of recessionary GDP and stubborn inflation is stagflation. Bank of England faces a difficult decision. Will the BoE get proactive and cut interest rates before the Federal Reserve? GBP/USD is below 1.25800 this morning.

2. Data: Stronger than expected U.S CPI statistics caused bedlam on Tuesday, but yesterday’s Retail Sales came in weaker. The ‘disappointing’ consumer spending numbers were likely welcomed by the Federal Reserve and financial institutions. Producer Price Index statistics will be published today, surprise inflation results could jostle financial markets.

1. Forex: Day traders witnessed whipsaw results early this week and should remain cautious going into this weekend. Patience will be needed as USD centric outlooks adjust to nervous shifts in behavioral sentiment.

AMT Top Ten Miscellaneous Insights for the 9th of February

10. Super Bowl AMT Prediction: Kansas City Chiefs 27 – San Francisco 49ers 24. After winning the MVP Travis Kelce will hug Taylor Swift and announce his retirement.

9. Jazz Fusion: Please listen to the song School Days played by Stanley Clarke while delivering a supreme bass guitar riff.

8. Tech: Google has announced its Bard A.I will now be known as Gemini in a rebranding. ‘Bard’ was a rather poor name, but is Gemini much better? Let’s ask Gemini what it thinks about the Google marketing team.

7. Banking Animal Kingdom: Central Banks parroting the same rhetoric globally as they choose to be ‘prey’ instead of ‘predators’, driving financial institutions and traders batty in Forex.

5. Deutsche Pfandbriefbank AG: A large slump in bond values for the German bank has sparked additional fears of exposure for banks involved with the commercial real estate sector. CRE appraisals remain unrealistically high in many European and North American cities as lending risks climb.

4. Cocoa: The price for the commodity was 4055.00 USD per metric ton on the 8th of January, as of yesterday it was 5666.00, a rise in cost of 39.72% in a month. Our sweet tooth just got more expensive.

2. China Economy: Deflation continues to be reported via the CPI and PPI statistics. Also, value of properties for housing and commercial real estate face significant headwinds. The real estate sector including ancillary infrastructure is at least 21% of China’s total GDP.

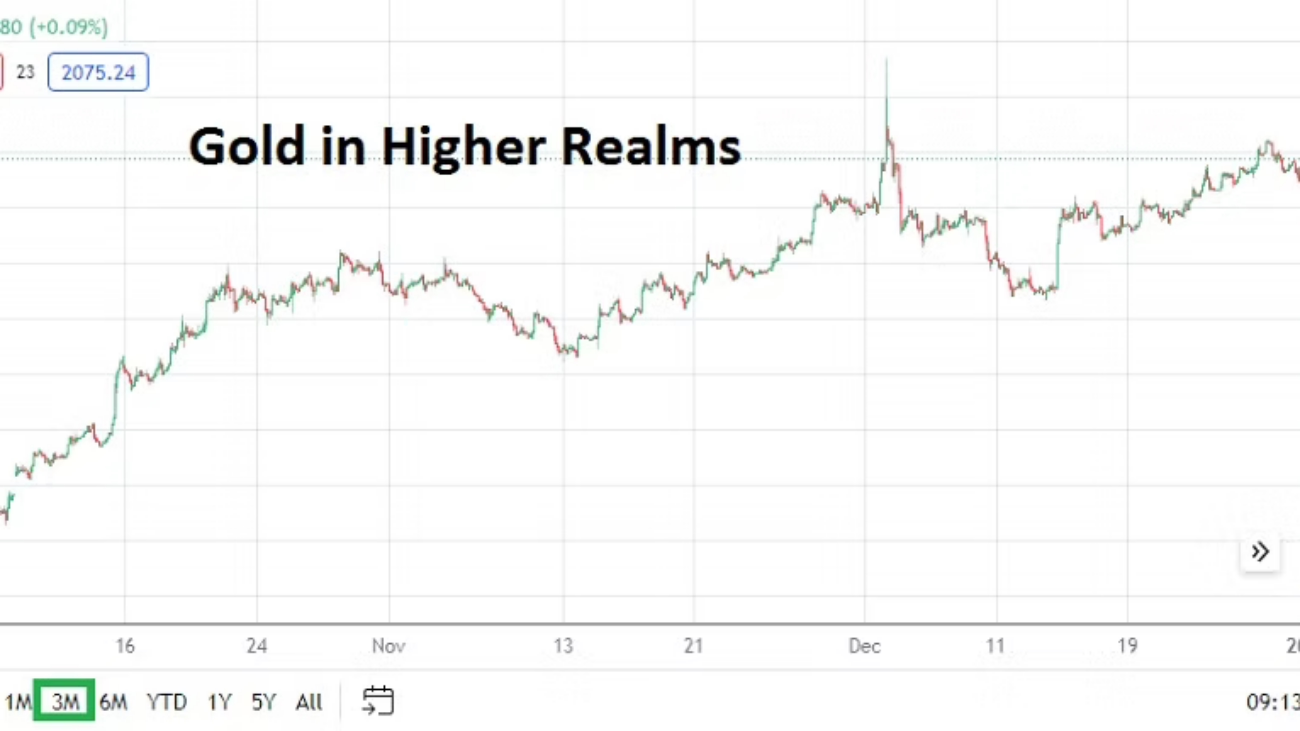

1. Risk Appetite: U.S equity indices finished Thursday’s trading achieving apex highs. The S&P 500 is challenging the 5000.00 level. Gold is near 2033.00 USD and WTI Crude Oil is above 76.00 USD as of this writing.

USD: Hidden Jobs Data Shows Potentially Intriguing Weakness

Forex traders like many market participants react to the ‘noise’ of U.S headline data results. The recent U.S jobs numbers published last Friday is certainly an example. The USD surged in strength on the backbone of more hiring via the Non-Farm Employment Change numbers. Also the Average Hourly Earnings beat expectations showing the cost of labor had become more expensive.

The U.S Federal Reserve stood in place last Wednesday before the jobs report. Pointing towards some troubling inflation, and mentioning the labor market was tight, the Fed refused to give a timetable regarding potential Federal Funds Rate cuts. The U.S central bank is showing more patience about coming interest rate cuts than many hoped on and had wagered.

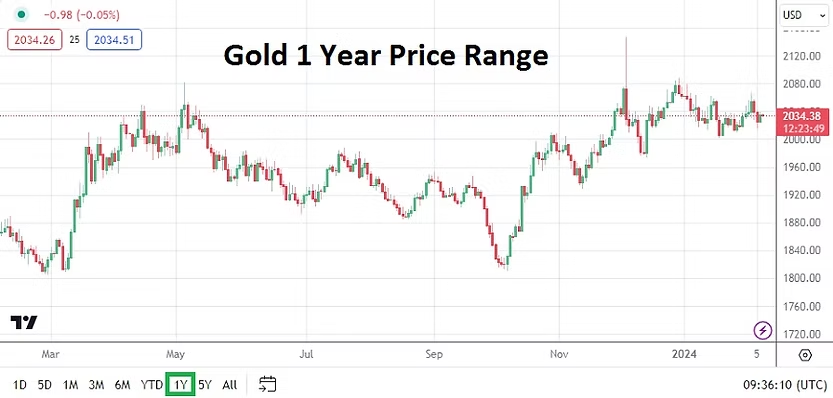

Gold One Year Chart as of 7th February 2024

Yet, there continues to be signs of anticipation for a weaker USD in the mid-term. The price of Gold remains within its higher elements, and U.S Treasury yields remain lower (although it must be said the past two weeks have seen an incremental move higher). And as a sign of potential inflation erosion, energy prices continue to be polite, which means the costs of logistics may continue to ease (except to say concerns about Suez Canal availability and chaos in the Red Sea are certainly risks).

WTI Crude Oil One Year Chart as of 7th February 2024

The fact that gold remains solid in value, and energy prices remain relatively low, and that support levels in Forex via the USD continue to drift near realms seen on the 13th and 14th of December is an intriguing behavioral sentiment clue. Perhaps it is a sign large institutional players believe they know something others are not considering regarding the future direction of the USD fundamentally.

There are always risks for day traders. Having solid information which is correct and can affect values in Forex, commodities and even equities is important for speculators, but is also hard to find when there are limited resources regarding market intelligence.

U.S Jobs Numbers Headline may be Misleading

Importantly, while last week’s jobs numbers on the ‘surface’ scared many large players who believed the USD will get weaker, thus causing the significant reactions via reversals in many major currency pairs teamed against the USD; there is some evidence from the U.S jobs statistics that needs consideration which was not widely reported. It is important to read beyond the headlines.

The amount of hours worked in the U.S on a weekly basis has eroded. Added to this consideration is that the stronger hiring numbers may still have been affected from seasonal needs due to the holiday season. This sets the table for the next U.S jobs numbers as a significant report on the 8th of March, and one that will have a big impetus on Federal Reserve’s monetary policy outlook and USD.

Perhaps it is conjecture to speculate the average workweek for employees decreasing is a telltale sign of weakening employment numbers to come, but it might prove to be a useful insight. Layoffs via U.S corporations continue to make news as companies seem to be bracing for a downturn in U.S economic health in the coming months. If the layoff theme remains noisy it will create the need for action from the Federal Reserve regarding monetary policy.

EUR/USD One Year Chart as of 7th February 2024

What does it mean for day traders? There are absolutely no guarantees, but the major currency pairs ability to stay within their mid-December prices is a likely sign that financial institutions have analysts which are looking beyond the headline numbers from the recent U.S jobs report, and have also seen the hourly workweek data. In other words support levels in many of the major currency pairs could prove durable. There is no doubt reversals and outliers will be demonstrated, and choppy Forex conditions will happen, but perhaps the current lows in many major currency pairs will start to exhibit resilience.

Trying to time short-term moves via behavioral sentiment that is generated by statistics found ‘hidden’ away in the jobs numbers is speculative. But if traders want to consider the potential of technical support, it might be worth a consideration to think the U.S employment picture isn’t as strong as the headline ‘noise’ is projecting.

AMT Top Ten Miscellaneous Raindrops for the 2nd of February

10. Risk Appetite: WTI Crude Oil almost serene around 74.00 USD, as bombastic rhetoric remains loud involving the Middle East.

9. South Africa: President Cyril Ramaphosa expected to announce the country’s election date when delivering the State of the Nation Address on 8th of February.

8. Tesla: Negative media coverage and an always defiant Elon Musk gravitate towards each other, share price is around 188.88 USD.

7. China: Shanghai Composite Index (SSE) hovering near 2,730 as of this moment.

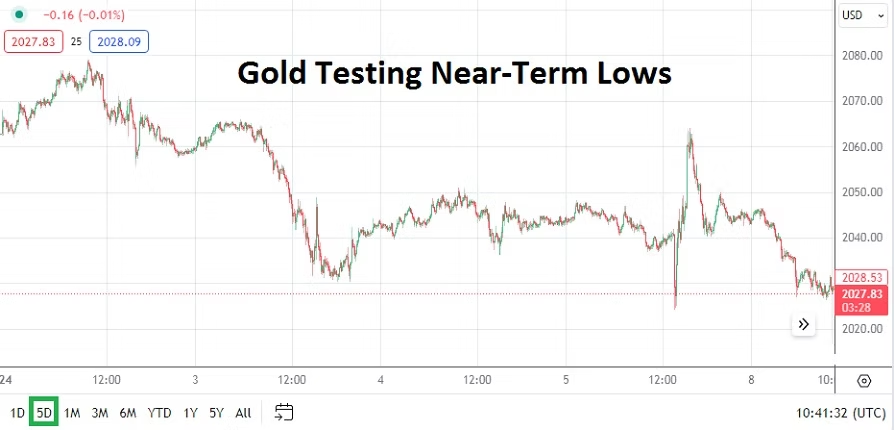

6. Gold: After near-term lows a challenge of highs as USD has gotten slightly weaker.

5. Central Banks: All bark and no bite yet, as financial institutions desire interest rate cuts from Federal Reserve, European Central Bank and Bank of England.

4. India: Nifty 50 Index near 21,865 as of this writing, it has gained more than 101% over the last five years – yes, plus one-hundred and one percent.

3. Forex Reactions: Recent short-term volatility and reversals seen as expected, patience still needed as USD mid-term outlook remains weaker.

2. U.S Equities: S&P 500, Nasdaq 100 and Dow Jones 30 have produced nervous results but still near record highs, as U.S Treasury yields have edged lower this week.

1. Data: U.S Non Farm Employment Change and Average Hourly Earnings today, this as some major corporations shed employees but labor market remains rather tight. Broad markets will react to the outcomes.

AMT Top Ten Miscellaneous Clues for the 26th of January

10. Sports: Australian Open Tennis Tournament Finals this weekend. And five episodes into Netflix’s Six Nations: Full Contact there has been NO mention of rugby national teams in the Southern Hemisphere. Bias?

9. Money Club: Microsoft has joined Apple with a market cap over 3 trillion USD, the only two companies in the world able to make this boast.

8. Democracy: India elections coming in April and May seem to have a predictable outcome, but the South Africa voting date has not been made official and the ANC is under pressure. U.S citizens appear set for a rematch of Biden and Trump in November.

7. Layoffs: Around 1,900 employees of Activision Blizzard and Xbox, both owned by Microsoft, will have their jobs eliminated. Microsoft spent about 68.7 billion USD to acquire Activision Blizzard – a deal that was finalized in October of 2023.

6. Nervous: Bitcoin still battling the 40,000.00 USD ratio. Binance Coin has fallen below 300.00 USD, BNB/USD traded near 200.00 USD in the middle of October.

5. Behavioral Sentiment: Gold remains near 2020.00 USD, U.S Treasury yields are in sight of three month lows, but energy prices have ticked upwards this week with WTI Crude Oil near 77.00 USD.

4. Forex Caution Sign: Day traders should be braced for price velocity today. Is the USD going to become weaker going into the weekend?

3. U.S Federal Reserve: FOMC Statement will be on the 31st of January. Yesterday’s GDP numbers came in stronger than anticipated, fueled by robust consumer spending. However the GDP Price Index results were well below their expectations. Some folks may be dreaming about a rate cut in March, but there is still plenty of data ahead.

2. Stock Indices: The S&P 500, Dow Jones 30 and Nasdaq 100 are within record heights. Japan’s Nikkei 225 is challenging values not traversed since early 1990. The values of these indices may be dizzying, but the trend has been hard to bet against.

1. Inflation: Core Personal Consumption Expenditures (PCE) Index reading is anticipating a 0.2% gain today. Last month’s outcome was 0.1%. The U.S Federal Reserve monitors this particular report closely. Financial institutions will react and any surprises will become a catalyst in the broad markets.

Choppy Forex Conditions and the Trading Week Ahead

Forex traders may be feeling a bit perplexed if they have blindly been looking for a weaker USD the past two weeks. While outlook for a bearish USD over the mid-term remains a theme from many analysts, day traders need to accept that intra-day results often create price fluctuations which make wagering on short and near-term perspectives dangerous. Trading conditions have been turbulent the past week and early this morning.

While analysis of monetary policies and economic data are vital, it is also important to remember there is a significant difference between the desires and needs of businesses functioning in global commerce, and the trading perspectives of speculators who are hoping to ride on the back of ‘insights’ provided by experts. It should also be considered that coming out of the holiday season many global corporations are now repositioning for 2024, and the financial institutions that work for these companies are also trying to get these outlooks aligned.

The USD has become stronger over the past day against many major currencies, but looking for a 100% reason to explain why this happened is likely misguided. Most U.S financial institutions were closed yesterday for the MLK holiday observance. While inflation data from the U.S Producer Price Index was weaker than anticipated last Friday and caused a brief spurt of USD bearishness, the greenback is lingering within the stronger realms of its near-term values against many currencies.

The idea that recent USD bullishness may simply be a sign that financial institutions believed the greenback had been oversold over the past couple of months may be correct, but this also opens the door for the potential of a reversal to develop and more USD selling as sentiment and economic data try to dance in a unified manner.

The week ahead may still prove to be choppy, but there are interesting bits of evidence that risk appetite lingers within the stomachs of many large investors. The slight rise in U.S Treasury yields recently may be worrying to some, but it should be acknowledged that the climb higher has been achieved while yields remain near mid-term lows. The same can be said for U.S equity indices which provided choppy conditions last week but certainly remain in highly valued realms.

Patience is a needed tool when trading, speculators looking for instantaneous results often lose money because they are being too aggressive. Risk taking tactics always have to be given importance.

Gold Three Month Chart as of 16th January 2024

Gold remains rather comfortable above the 2000.00 USD level. As of this writing the spot price for the precious metal is near 2050.00 USD. This is fascinating because it underscores the notion that long-term gold buyers appear to believe the USD will remain within weaker territory. But again, short-term and mid-term outlooks for speculative wagers are two very different things.

Tuesday, 16th of January, Canada Consumer Price Index – the inflation numbers from the ‘North’ are expected to be lower than last month’s results.

Shanghai Composite Index Five Year Chart as of 16th January 2024

Wednesday, 17th of January, China Industrial Production and GDP – recent economic reports regarding the deflationary troubles the nation is facing have been loud. The industrial and growth numbers should be monitored. The Shanghai Composite Index (SSE) is trading near values last seen in May of 2020, this is not a good signal.

Wednesday, 17th of January, U.S Retail Sales – the consumer data will have an affect on sentiment in the broad markets. The results are anticipated to match the Core Retail Sales gains from last month, and the broad number is expected to be slightly higher. Traders should be alert in case a surprise outcome occurs. If the statistics are close to the estimates, this could create some calm in Forex and perhaps set the table for USD weakness to be seen for a moment.

USD/JPY Three Month Chart as of 16th January 2024

Thursday, 18th of January, Japan Revised Industrial Production – while the report is not viewed as a major piece of financial impetus in the speculative world, the USD/JPY has been rather dangerous for short-term traders caught on the wrong side of recent bullishness. If the number comes in at minus -0.9% as expected, it will then likely take USD centric bearish sentiment to cause a reversal lower. The past two weeks in the USD/JPY have been difficult for traders looking for downside momentum. A stronger than expected industrial number from Japan would likely help USD/JPY bearish outlooks.

Friday, 19th of January, U.K Retail Sales – the British consumer spending numbers are expected to come in weaker. The GBP/USD is currently trading near early January values as choppy short-term conditions persists.

AMT Top Ten Miscellaneous Notions for 12th of January 2024

10. Music: School Days by Stanley Clarke. Recorded in 1976, the ‘song’ is one of the best jazz fusion pieces ever played.

9. Coaches: Bill Belichick and Pete Carroll have been ‘politely’ fired, Nick Saban has retired. NFL and college football remain the ‘Kings of Sport’ in the United States.

8: Taiwan: Presidential election will be held tomorrow. Expect noise from China this weekend regarding Taiwan’s sovereignty.

7. Forex: Volatility struck yesterday in USD based currency pairs, whipsawing as financial institutions reacted to the Consumer Price Index reports. More inflation data will come from the U.S today.

6. Gold and Crude Oil: Precious metal value has been ‘almost’ steady, and WTI Crude Oil price remains rather calm.

5. China Deflation: CPI and PPI numbers were lackluster this morning. Export numbers from the nation have also delivered troubling declines.

4. Houthis: U.S and U.K missile strikes in Yemen have been conducted, diatribes from the extremists have been sounded, and may cause some investors concerns and potential risk adverse trading considerations going into weekend.

3. Bitcoin: SEC ETF funds approval has been completed, and launch is set to allow retail traders and ‘investors’ to purchase the digital asset. BTC/USD is near 45,960.00 currently. CFD products from brokers will likely be introduced and flourish soon, which will be based on the ETF notional values and allow day traders to wager on upside and downward momentum.

2. PPI Data: U.S Producer Price Index inflation results today could rattle the broad markets. No changes are forecasted. A surprise increase would worry those betting against the USD. Traders should also keep their eyes open for potential revisions to previous months.

1. Risk Appetite: Dow Jones 30, S&P 500 and Nasdaq 100 continue to flirt with apex values. The Nikkei 225, from Japan, is challenging highs not seen since 1990 as it trades above 35,575.00 for the moment. Equity indices remain optimistic.

Cautious Trading as Key Data and Outlooks Await Impetus

The start of trading this week could prove to be slightly adventurous for speculators as financial institutions return to the markets and start to take positions for their clients. Having survived the past two and a half weeks of holiday season trading, market action will now focus on immediate, mid and long-term goals and outlooks depending on time frames and targets. Slightly nervous trading was on display last week, but some traders may believe their is plenty of room for more optimism and may be suspicious of the results delivered.

Gold Five Day Chart as of 8th of January 2024

Day traders should look at some barometers before they participate in the near-term. Gold has come off highs seen late last week, but remains within the higher elements of its six month price range. Its selloff from apex values last week perhaps correlates to U.S equities and USD turbulence which has also been experienced.

Last Friday’s reaction to the U.S jobs numbers was fascinating. The numbers delivered an initial shock to folks who wanted to react quickly. Hiring the last month increased more than expected, which might have caused the momentary bullish surge in the USD. Only to be confronted swiftly by further investigation of the jobs data which showed previous months statistics had been revised downwards. This acknowledgement set off selling of the USD and technical whipsaw results.

Day traders participating in Forex this past Friday likely experienced a range of emotions. If the market correlations are correct regarding the USD and the reactions seen, trading in gold also seemed to mirror the price action. Interestingly, gold touched a low of nearly 2024.00 USD on Friday in the wake of the jobs report, surged higher to around 2064.00 and then reversed lower again.

The notion that gold is trading within sight of Friday’s lows is interesting for both the precious metal and trying to understand where USD sentiment will lean early this week.

Behavioral sentiment remains rather optimistic, however nervous headlines during the holiday season may have caused cautious shadows to grow darker, particularly as light trading volumes affected results. Today and tomorrow will prove interesting in the broad markets, this as financial institutions return in full and as they brace for U.S inflation numbers later this week.

S&P 500 One Month Chart as of 8th of January 2024

Nervous short term trading is likely today and tomorrow as price equilibrium is sought. U.S equity indices have backed away slightly from their flirtations with all-time highs, but even as selling developed the past week highs are still in sight and are likely still being dreamed about by many institutions. U.S Treasury yields will also be a good indicator for Forex traders early this week regarding how comfortable financial institutions are with their current outlooks.

Monday, 8th of January, Germany Factory Orders – a slight gain of 0.3% was reported today, which was below the 1.1% expectation. The German economy is starting to show signs of economic growth, but has major hurdles to still climb. The lackluster German numbers may keep the ECB in a rather neutral stance for the mid-term. Which might help a bullish EUR/USD outlook if the U.S Fed is seen as the first major central bank which will have to cut interest rates.

AUD/USD Three Month Chart as of 8th January 2024

Tuesday, 9th of January, Australia Retail Sales – the anticipated climb of 1.2% is significantly higher than the negative -0.3% result from last month. A good outcome via the Retail Sales could help the Australian Dollar reignite some positive momentum. CPI data will come from Australia on Wednesday, which will certainly affect the AUD/USD too.

Wednesday, 10th of January, U.S Ten-Year Bond Auction – though day traders may not be too involved regarding the sale of U.S Treasuries, the results from the auction will have an affect on Forex. U.S Treasury yields should be monitored.

Thursday, 11th of January, U.S Consumer Price Index – a slew of CPI results will get the attention of financial institutions. The inflation data is expected to show a slight decrease in the Core CPI result, but show a slight gain in the broad number. This will likely be the most heavily traded day since the third week of December. There will be a reaction from the inflation reports. If the numbers come in around the estimates this may help the bearish mid-term outlooks for the USD. If the results are shockingly stronger, the USD would turn bullish. Day traders need to be careful in the midst of the Consumer Price Index publications because volatility is expected.

Friday, 12th of January, China CPI – a decrease is expected from the Asian giant. Deflationary concerns are shadowing China’s economy. The expected number of minus -0.4% would actually be an improvement compared to the last reading which was minus -0.5%. The USD/CNY has been rumored to have been experiencing some ‘hands on’ management from China. Investors continue to be nervous about China’s economic outlook and would like to see signs of improvement.

Friday, 12th of January, U.K Gross Domestic Product – a gain of 0.2% is being anticipated. Any growth from the U.K GDP would be welcomed considering the recessionary data which has been lingering. The GBP/USD will react to the results and bullish momentum in the currency pair could be sparked by a better than anticipated number.

Trading Optimism for 2024 and Pursuit of Castles in the Air

Traders may feel like horses being kept in their stables right now. The desire to run freely in Forex and other markets is certainly being felt, this as many analysts have jumped onto optimistic bandwagons and are pointing to the U.S Federal Reserve and its rather dovish outlook for 2024. Gold in early trading this morning is lingering near highs and the USD remains within weaker territory when technical charts are inspected via one month results.

Gold Three Month Chart as of 2nd January 2024

Yet, thin holiday trading is full in effect. Light volumes will continue to be seen early this week after the New Year’s celebrations. Financial institutions will open their doors today, but their corporate clients around the world will have plenty of employees who will remain on vacation until the 8th of January. Thus, while day traders may feel enticed to wager in the markets with various CFDs, they should be careful and understand unbalanced positions may cause temporary chaos. Risk taking tactics should be carefully considered.

The desire to dream about castles in the air is a source of comfort for many new day traders. But remaining realistic about potential results, while not getting overly ambitious about targets is an important aspect for all speculators. While trends may look attractive in Forex, commodities and equities a well planned approach regarding risk taking is a practical road. Castles in the air tend to vanish.

Optimism will be a word frequently heard in the coming days and weeks, and here’s to wishing everyone a prosperous and peaceful 2024. The potential of a more dovish U.S Federal Reserve regarding monetary policy and declining Treasury yields sparking more risk appetite in equities as investors seek solid returns is alluring, however risks remain on the table. The economy of China continues to worry analysts and tensions in the Middle East are still a long way from being solved.

However, the biggest cause for speculative concerns during 2024 may come from elections in Taiwan, India, South Africa and the United States. Taiwan’s presidential vote is on the 13th of January. China will certainly be watching the results, and traders should expect to hear swords rattling afterwards and then hope the noise calms down.

USD/ZAR One Year Chart as of 2nd January 2024

Tranquil voting results in India will be welcomed by investors. India is becoming a noteworthy economic giant, its rapid growth and ascension as an important investment vehicle needs to remain stable. South Africa remains troubled domestically by concerns regarding corruption and inefficiency, its upcoming spring election results may not solve the problems it faces. There will be many elections in Africa this year, which could spur on considerations regarding geopolitical alliances and the price of commodities.

The U.S election late in 2024 will start to grow in noise as the months progress and by early this summer behavioral sentiment will begin to become nervous regarding the outcomes for the White House and Congress. The U.S appears to be braced for an election between Joe Biden and Donald Trump and this will certainly cause skittish storms.

Traders should feel confident about risk appetite in the global markets improving, but they should keep in mind that impetus coming from many different spheres can affect the financial world.

Tuesday, 2nd of January, U.S Final Manufacturing PMI – today’s Purchasing Managers Index is expected to show a slight improvement, but the results may fall on deaf ears because many market participants will not be around to react due to the fact they are still on vacation.

Wednesday, 3rd of January, U.S ISM Manufacturing Prices – this inflation survey from purchasing managers may be given a bit of attention, but its effect may be limited because of light trading volumes still being exhibited.

Thursday, 4th of January, Germany Preliminary CPI – the inflation data from Germany will get some consideration, and the result is expected to show a slight increase. Services PMI data will also come from European Union nations, the U.K and U.S.

Friday, 5th of January, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs reports will get the notice of financial institutions. The results for employment and wages are expected to be slightly weaker than the previous month’s outcomes. Typically these numbers would cause a stir, but unless there are surprises, most financial institutions may not react massively to the reports because it remains a ‘holiday’ week. If the numbers come in weaker than expected this could cause interesting reactions on the 8th of January and weaker USD sentiment.

AMT Top Ten Miscellaneous Viewpoints for the 29th of Dec.

10. Book: Cargill: Trading the World’s Grain by Wayne G. Broehl, Jr., a book that folks interested in physical commodities may find interesting.

9. Music: A Night in Tunisia played by Charlie Parker and Miles Davis on The Complete Savoy & Dial Master Takes.

8. NBA: Detroit Pistons have now lost 28 straight basketball games. Will the team get a participation trophy at the end of this season?

7. Post-Quantum: While ‘Artificial Intelligence’ grabs headlines, ‘post-quantum cryptography’ is a phrase and reality that corporations will need to learn increasingly.

6. Behavioral Sentiment: Risk appetite has remained firm during this holiday week, which may spark additional optimistic trading banter in January as trends are wagered upon.

5. U.S Treasuries: Yields have continued to move lower, and dovish outlooks regarding the U.S Federal Reserve inside many financial institutions may increase speculative zeal.

4. Gold: The precious metal remains near highs and the price of 2100.00 USD is hovering above, will this level start to be challenged and penetrated?

3. JPY and NZD: Both currencies remain bullish as they recover from long-term USD strength, this while mid-term price realms are being firmly challenged. Technical traders with long-term outlooks may want to start examining one year charts.

2. U.S Equities: S&P 500 on the cusp of record highs, the Nasdaq 100 is at apex values – while the Nasdaq Composite remains bullish, and the Dow Jones 30 continues to create new heights.

1. 2024: A prosperous and peaceful New Year is wished for all.

Traders who want to pursue speculative positions this week need to understand that market conditions will be extremely thin. While the USD has certainly taken on a ‘softer’ dimension and financial institutions are demonstrating solid risk appetite, this week’s trading could produce lackluster choppy conditions.

Economic data will be light this week due to the ongoing Christmas celebrations, and the New Year’s holiday which will come next Monday. Forex markets can produce trading opportunities in the near-term for folks who want to wager on changes of direction, but some of the trajectories may be dubious and reversals could loom. Entry orders are urged for participants because spreads between bids and asks will likely be wide.

Gold Three Month Chart as of 26th December 2023

Gold remains within its higher price boundaries as the USD produces weakness, but betting on the precious metal this week could also be dangerous. Gold has certainly been trending upwards, but short-term speculative positions by large players could make the commodity agitated the next handful of days if they try to take advantage of light volumes. Day traders without significant bankrolls should be careful.

While economic data will be released, it is doubtful how much impact the reports will have on the broad markets. Active traders should monitor the coming statistics, but they should stay ‘more’ alert for possible outside influences which could shake confidence and shadow the rather optimistic behavioral sentiment which is currently being demonstrated.

News via international shipping should be given attention as the Houthis and Iran rattle their swords. While experienced traders will not be flustered by noise, the potential for escalating violence should be given attention.

USD/JPY Three Month Chart as of 26th December 2023

Tuesday, 26th of December, Japan Core CPI via the BoJ – inflation data from Japan has been published today and the Consumer Price Index came in below expectations. The USD/JPY remains on a downwards trajectory and should be given consideration.

Wednesday, 27th of December, U.S Richmond Manufacturing Index – this report being ‘highlighted’ shows the minimal amount of data being published this week. A decline versus the previous month’s negative outcome is expected. The likelihood that significant trading will be ignited via the results of this publication is almost nil.

Thursday, 28th of December, U.S Pending Home Sales – the data is expected to show a gain of 1.1%. However, it is next month’s report which will get more attention, this as investors look to see if the Fed’s soft monetary policy stance which was heard in mid-December, helps boost the housing market in the coming weeks. This immediate report however is likely to be met with a rather quiet reaction.

Friday, 29th of December, U.K Nationwide Home Price Index – this economic report like yesterday’s U.S housing numbers is destined to have little influence on short-term trading results. The GBP/USD will not be affected by this report in any great manner.

Leverage and the Holidays Often Leads to Costly Volatility

This may seem like an unfriendly reminder for this time of year, but holiday trading can lead to dangerous storms for traders. Keeping a realistic viewpoint regarding your ambitions during Christmas and New Year’s is important.

Most day traders cannot afford to have an outlook that is beyond the short and near-term. This is an ugly fact many speculators with less than deep pockets have to acknowledge if they are new to speculating. While large traders and financial institutions can maintain mid and long-term outlooks, day traders who do not have the funds to keep overnight positions need to operate in an entirely different fashion.

Trends via technical charts and fundamentals are crucial for all traders. Behavioral sentiment is a key ingredient too for all participants chasing assets. However, day traders also need to understand unique risk management limitations. The use of leverage is a vital dynamic, and can cause devastation fast when too much money has been wagered. The use of leverage by day traders effectively raises the probability that a trade will lose money.

Incremental changes in value to a Forex pair, commodity and equity share being traded on a brokers platform by a speculator using ‘borrowed’ money via an account that allows for margin often leads to quick outcomes that fail. Many brokers offer traders ‘polite’ leverage ranging from 10% to 100% in extra funds, this while enticing the speculator to the potential of profiting in a quicker and more robust manner. It should also be noted that when a broker is offering vast amounts of leverage, they are knowingly increasing a traders likelihood of losing. The use of leverage beyond 10% leads to plenty of expensive mistakes.

Unfortunately, the simple truth is if you can make fast money trading, you can lose fast money while trading. The use of the word speculating is simply a gentle way of not using the word ‘gambling’.

Traders tempted to pursue wagers during the next couple of weeks should remember a lack of normal volumes make many asset classes more volatile, meaning the use of leverage by speculators often leads to dangerous gyrations within their accounts.

Risk appetite has taken on a optimistic tone globally because of the upside U.S equity markets have been producing, while U.S Treasury yields are decreasing, but dangers still lurk. Day traders need to remain realistic regarding their pursuit of quick hitting trades during the holiday season, and make sure they use solid tactics while pursuing their outlooks. The trend may appear to be your friend, but short-term reversals in the wrong direction can cost money.

No one wishes for bad things, but speculators should also note that if risk adverse events occur during the holidays, that ‘negative news’ can often become amplified this time of year and cause more volatility. Speculative positions in Forex, Crude Oil and gold can produce rather wild results, and thin trading volumes can add to the swift changes in values.