Unpredictability of President Trump and the Markets

Everyone wants to know what will happen in the future in the financial world. Most everyone also knows that this is impossible. However, clarity about the mid-term is a legitimate focal point that financial institutions strive. Risk managers define their considerations on assorted perspectives depending on their backgrounds.

While some may like him and others clearly are are not fans, President Trump has a reputation for wanting to get things done. His calling card for a long time has been an ability to make business deals. President Trump however has put himself in a rather difficult position and the next two weeks may prove to be an important milestone. One in which those who like the President and those who don’t will be given more credence to debate.

The Federal Reserve will announce their FOMC decision on the 30th of July. Tariff deadlines will supposedly come on the 1st of August. President Trump has made it clear he does not like the lack of aggressiveness which Fed Chairman Jerome Powell is displaying. Trump has called for the Federal Funds Rate to be cut and Powell has not acquiesced.

President Trump has openly spoken about trying to replace the Fed Chairman, but at this juncture the Trump White House knows this will be difficult unless they can prove Jerome Powell has done something maliciously. Not lowering the Federal Funds Rate because of a fear inflation will develop because of potential effects due to tariff fallout is a legitimate reason not to act. Even if the Fed Chairman is wrong, he appears to still be working on a basis which is based on an economic interpretation.

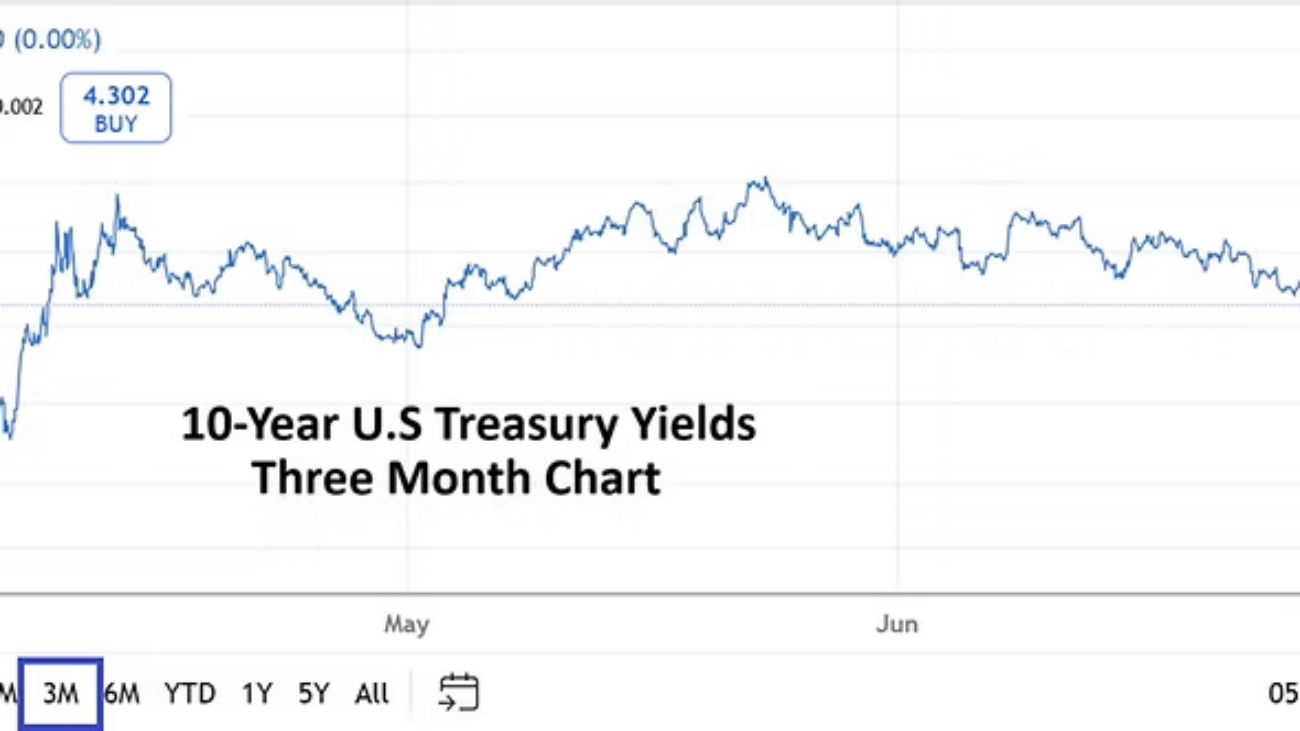

For the next two weeks the broad markets will hear about the Trump and Powell disagreement. It has been argued the Federal Reserve should have lowered the Federal Funds Rate a few months ago, clearly this was not done. However, the USD did trade with weaker sentiment in Forex from early April until the beginning of July. In the past few weeks the USD has garnered some strength, but remains within the lower part of its long-term realms via the U.S Dollar Cash Index. The weakness in the USD was likely due to financial institutions betting on rate cuts to come over the mid and long-term, and which they still believe will happen.

The upwards momentum generated recently by the USD has put the greenback in a position that seems to indicate financial institutions are transacting their cash forward orders cautiously for the moment, while waiting on the next round of impetus. And that is where Federal Reserve clarity and tariff threats now shadow mid-term outlooks.

We have entered an unpredictable window and President Trump apparently doesn’t mind allowing a little danger into the mindsets of the financial markets. It is one thing to proclaim tremendous results and great, magnificent prospects, but how long will investors tolerate a lack of clarity regarding tariff agreements? President Trump has postponed the tariff deadlines several times and what should be considered is the potential that at some point he will have to take action to prove he means business. If the August 1st deadline is extended again this may not cause much of a shock, but it will not be met with optimism.

Instead, the main interpretation from financial institutions may be that Trump is struggling to get agreements done as he had promised. While that might lead to the idea that global commerce will continue on as is, this will certainly not help create the positive impetus which President Trump desired. At some juncture President Trump may begin to be perceived as the little boy that cried wolf. No one will pay attention and the markets will proceed without him. But President Trump will not likely let that happen, he does like attention.

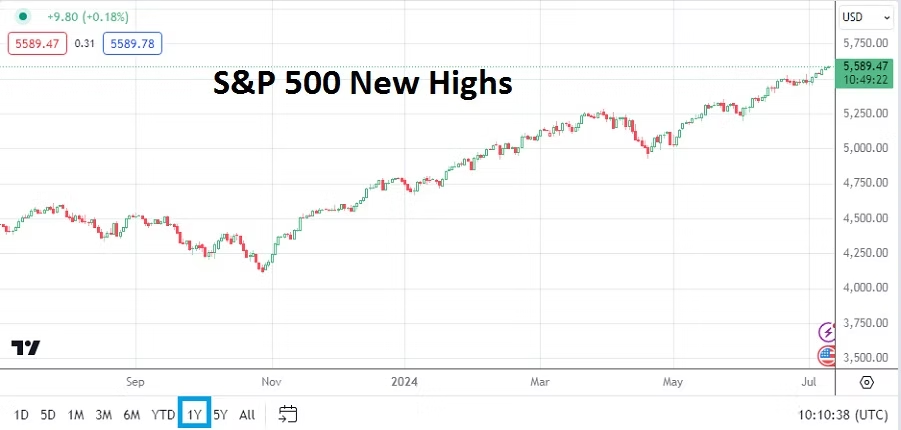

The Nasdaq 100 and the S&P 500 are near record highs, so there isn’t a lot to complain about by index investors. The U.S economy has shown signs of green shoots regarding better retail sales and the recent Philly Fed Manufacturing Index. The grey area for many remains inflation, which has been coming in rather well behaved although the most recent report showed a slightly higher outcome with the yearly CPI reading. However, the Federal Reserve actually has evidence that inflation has been tame. Yes, there are questions regarding the coming influence of tariffs on the U.S economy, but for the moment inflation has not risen.

The lack of clarity and not having a mid-term comfort level which is unperturbed may be problematic for small U.S business owners that face tariff concerns on their imported goods. And the bigger picture remains unclear for large U.S corporations – but they certainly continue to try being optimistic. And this is where it gets more dangerous, plenty of perspectives are being driven (inspired) by analysts who have confirmation bias. For instance the downturn in the USD from April until early July was amplified by many who saw this as a sign the USD was being punished by foreign governments opposed to President Trump. This in fact was highly unlikely, traders need to remain alert to false narratives.

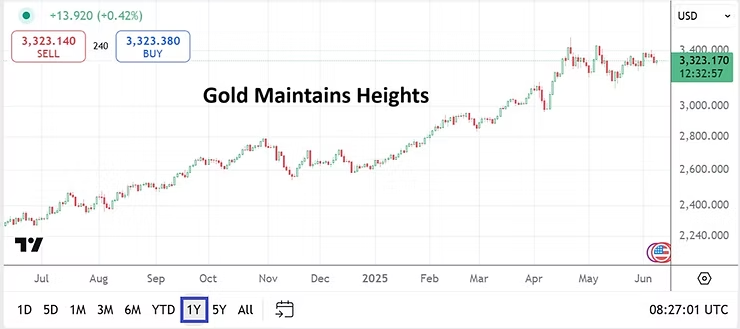

The next two weeks need to be treated carefully. There will be a running monologue among many analysts that changes daily as behavioral sentiment moves depending on what is being spoken about the Federal Reserve and tariffs. However, until there are actual answers the financial markets are likely to remain rather choppy. Self awareness will be crucial for speculators. Also, a large factor in the financial markets will be played by the U.S White House regarding how incoming results are presented. Until then day traders may want to watch technical charts and try to figure out where programmed trading lurks regarding support and resistance levels. Price velocity in Forex, bond yields and gold should be monitored.