Speculative Opportunities Do Not Promise Immediate Profits as Cautious Outlooks Stir

The S&P went into this past weekend with slight gains made on Friday, but essentially finished where last week began. In early morning trading via the futures market the index has seen a slight decline. Retail short-term traders may decide that offers the potential to sit on the sidelines and watch what may be rather choppy conditions, this if they decide not to pursue.

Global markets including stock indices like the Nikkei and broad Forex have shown more discomfort early today. Short-term concerns and mid-term viewpoints are colliding and making momentum hard to sustain. The S&P 500 remains within its elevated realm, but there is a rather unpleasant taste many speculators have had to endure since the end of May, particularly if trading ambitions have been limited to near-term pursuits.

S&P 500 Futures Six Month Chart as of 13th July 2026

There will be a crowd of people at summer parties (or winter outings depending on which side of the equator you are on) discussing the gains made in the S&P 500 (and Nasdaq 100) since the end of March who will be quite keen to brag about their insights. However these same people have likely made their money via pension funds, mutual funds and other long-term endeavors guided by institutions managing their money. Because most short and near-term retail traders have likely been savaged by the results in the marketplace the past handful of months.

Trading within the current markets conditions for those who have smaller accounts and are relying on leverage to create profits have likely been bled dry of their funds if they have not used proper risk management. It is one thing to want to make a thousand dollars a week in the markets as a retail trader and quite another to actually accomplish the task.

Indices the past handful of months have been a churning machine in which volumes stir and create attractive chatter, but also deceive folks into believing they can win easily. The only folks winning consistently right now are brokers handling their clients’ retail accounts.

This doesn’t mean you have to stop and give up as a retail trader, but it should serve as a warning that not being overly ambitious and remaining patient are keys when trying to beat the markets. And again, let’s remember the average retail trader has about a 90% chance of failing when trying to speculate.

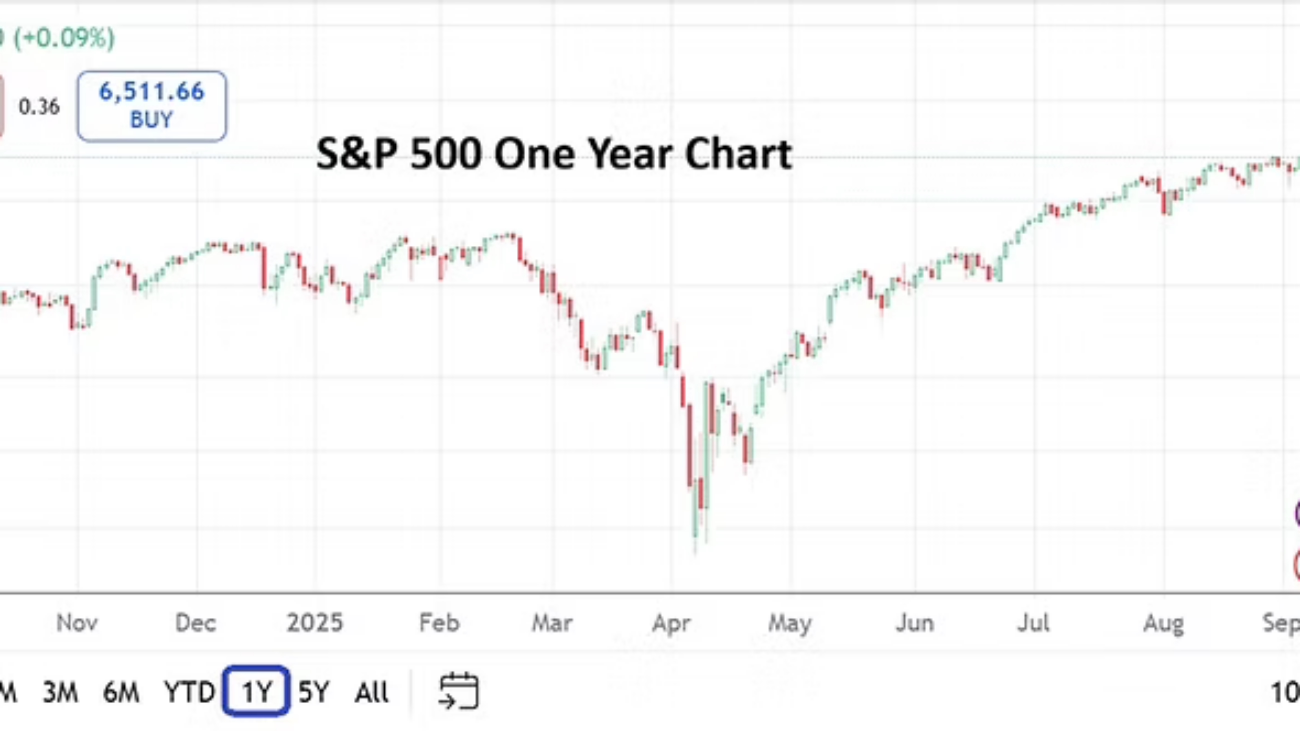

The S&P 500 did hit a record height in early June around the 7,620.00 vicinity. Its current values are well within sight of those highs too. Yet, headwinds continue to be seen via trading results intraday as financial institutions deal with wavering behavioral sentiment complicated by a myriad of concerns.

Yes, there will always be concerns in the marketplace, risk and reward are often compared to the potential of loss. If you are placing a bet in the markets that you believe can garner a thousand-fold profit, it is likely you are also risking a thousand-fold loss. And unfortunately the marketplace, nor your broker is going to lose sleep over your inability to understand what risks you are undertaking. You will hear that you have learned a tough lesson and the experience will help you become a better trader next time around by your broker, this as they offer you another opportunity to enter the markets on their platforms, but it still doesn’t guarantee you anything.

The rumblings from the Middle East continues to mitigate sentiment in the global markets. As of this writing WTI Crude Oil is around $73.70. If military conflict between the U.S and Iran continues to incrementally escalate, perhaps experienced players will be able to handle the noise and worries regarding higher energy costs and threats of inflation.

Equity indices are also running into problems caused by a realization that the costs of investing into companies working in the AI realm are now having to deal with rising costs, this as revenues do not meet expectations, and a lack of adequate physical resources to fuel growth in the sector are raised as concerns. And it is not a stretch to say the AI sector has helped drive more than a handful of equity indices higher. A legitimate fear regarding a downturn in AI related stocks and a possible knock-on effect is a sobering reminder that bullish trends do not last forever.

And then there is the shadow that is overhangs the Federal Reserve and interest rate calisthenics being worked out by analysts who are trying to convince others (and themselves) that their outlooks are correct.

Yet, we return thankfully to a simple notion and question, one that has very little to do with economics that are taught in university classrooms – are there enough buyers in the marketplace to sustain the upwards trend in the S&P 500? The answer doesn’t have much to do with fundamentals, and often is driven by pure sentiment. Pushing aside day to day travails, wagering on long-term upside remains almost the only wager that can be made. Sure, you can bet on downside; you can short stocks, buy put options that look for lower markets. However, matching negative outlooks with the correct timeframe is just as hard as it is to bet on positive momentum. For the time being it is easy to say the near-term remains murky for day traders. It is harder to predict actual direction