Hurricanes, Wars, U.S Election and Inflation Reports Noise

Between hurricanes, wars, the coming U.S election what could possibly go wrong for day traders? Oh wait, the U.S will also issue their Consumer Price Index reports today to throw some fuel onto the Federal Reserve outlooks of financial institutions. As the loud headlines get attention and try to scare us, it should be noted that markets have actually behaved rather calmly this week. Perhaps volatility was already traded heavily into assets the past week and a half, and tranquility is returning. However, there is the possibility that experienced smart money has simply positioned investments and speculative endeavors, and now await outcomes via objectives in order to react.

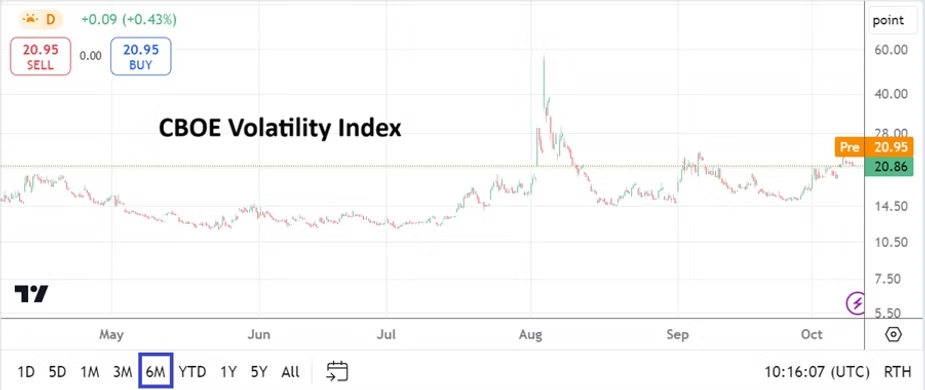

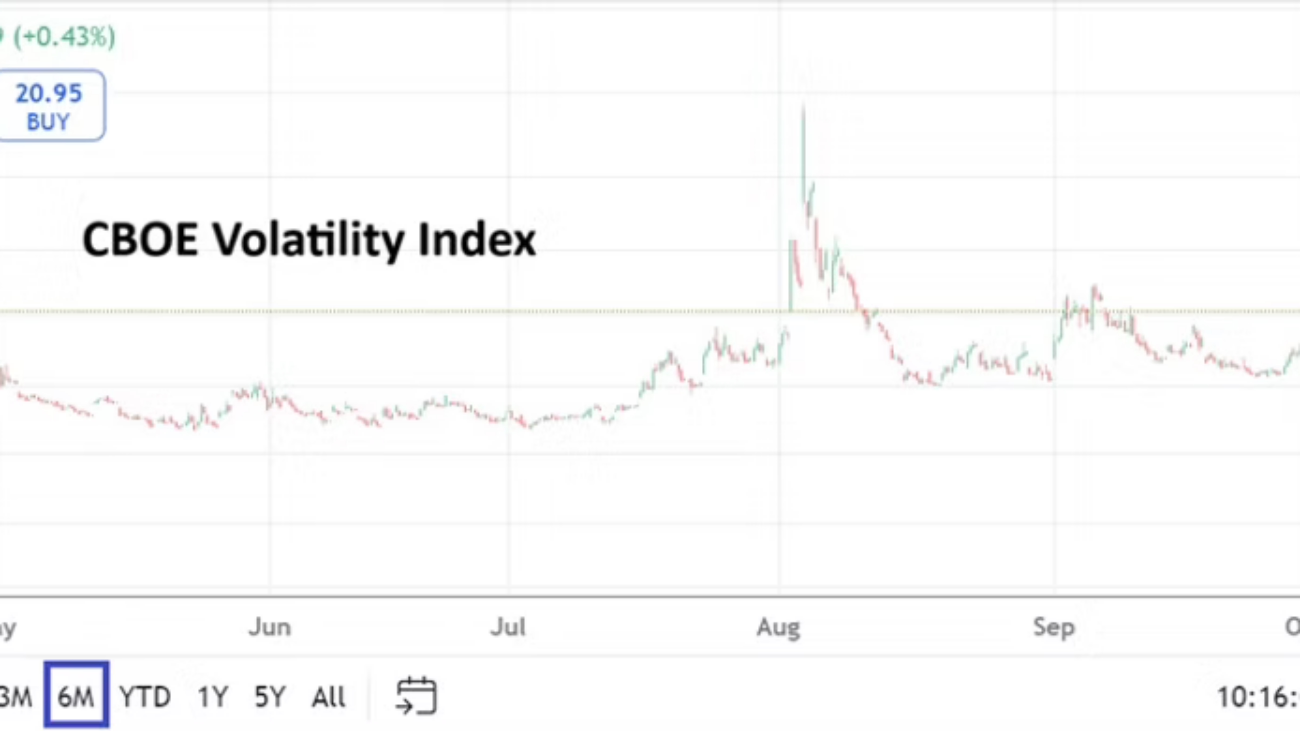

CBOE Volatility Index Six Month Chart on the 10th of October 2024

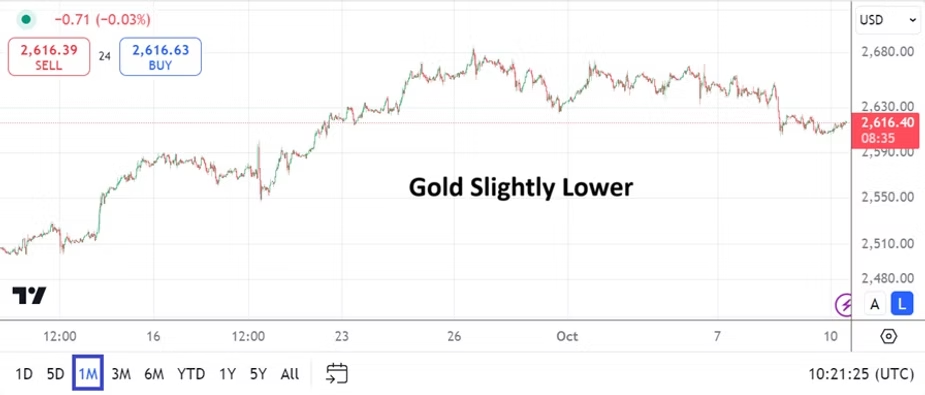

The Chicago Board Options Exchange’s Volatility Index (VIX) has risen since the last week of September, but remains within known realms. Gold while definitely within the higher levels of its long-term price range has ebbed lower during the same timeframes. And WTI Crude Oil while flirting with short-term highs today, actually remains within the known realms of its six month range. In other words while short-term day traders potentially get caught up in fearmongering rants and tremble, financial institutions continue to trade with an outlook that remains rather tame mid-term.

Gold One Month Chart on the 10th of October 2024

Financial institutions were dealt a perplexing blow last Friday when the U.S Non-Farm Employment Change hiring numbers came in stronger than anticipated. However, what is not getting enough attention is another revision downwards to the previous month’s totals did happen. Today’s Consumer Price Index statistics and tomorrow’s U.S Producer Price Index results are expected to show that inflation remains under control. If the coming data meets estimates or can show a slight decrease this could ease the fear of some financial institutions regarding what’s coming next from the Federal Reserve. If higher inflation numbers are displayed this would spark more volatility.

WTI Crude Oil Six Month Chart on the 10th of October 2024

Certainly, USD selling got ahead of itself by the end of September. Day traders need to understand there are seldom one way avenues in Forex. Intraday reversals aside, when equilibrium and outlooks do not mesh via the insights of financial institutions, volatility occurs. The buying of the USD since September’s end has been noteworthy, but it was not entirely unexpected. The CPI and PPI reports from the U.S on the calendar will provide impetus. Let’s see if the markets remain calm as a swirl of other risk events linger in the air. Risk adverse tendencies have caused caution in the broad markets.

USD Cash Index Six Month Chart on the 10th of October 2024

Traders need to know there will be one more jobs report from the U.S on the 1st of November. There are some people around us that no doubt believe the U.S government is showing better than expected jobs numbers to try and ramp up support for certain political candidates. However, if analysts do their jobs well enough and point to the revisions downwards that have been consistently seen, this could help alleviate fear of conspiracies.

The Fed is still in a position to cut the Federal Funds Rate by another 0.25 on the 7th of November. Yes, the FOMC Statement is coming only two days after the U.S election, so the Fed’s decision which will be garnered during meetings on the 6th and 7th will carry some significance depending on who has been elected U.S President. While U.S economic data has been mixed via a combination of jobs numbers which had been faltering until last week, and consumers suddenly showing greater confidence and manufacturing sentiment in important sectors with improved optimism, interest rates are still high. The Federal Reserve has a dilemma and likely will want to try continuing to incrementally cut borrowing costs when they have the opportunity.

Day traders should not be too concerned with what will happen a few weeks away, particularly when they are interested in the results of trades consisting of a few minutes, half hour, and other limited durations. But they should always understand their positions in Forex, equity indices, commodities, and elsewhere have little to no effect on the real marketplace. Day traders need to be able to catch onto the technical trends and behavioral sentiment being created by larger players and financial institutions.

AMT Top Ten Miscellaneous Rays of Light for 23rd of August

10. Word of the Day: Like crepuscular animals which are active during twilight, large market players are ruminating as their summer hiatus draws to an end over the next week and a half. Plans for coming hunts are being formulated as leisure concludes for financial institutions preparing to work in the shadows.

9. Scrolling Failures: Lack of solid results on search engines are becoming a growing annoyance. Is it just us? An abundance of poor information via defined searches on the internet and finding what is sought is becoming increasingly problematic. Is AI being allowed to do too much while still too dumb? AI doesn’t know when it is wrong. Competitors to Google and others are sought.

8. How Dare Us: The postponement of imposed dates regarding energy policy changes are multiplying. The end for the classical use of oil, coal and nuclear is not near. Efficient power is evolving, but this will have to include ‘antique’ generation and grids. The demand for electric vehicles are being confronted with declining sales via U.S consumers. Tangible technology needs precise planning, not apocalyptic rhetoric which tries to scare people.

7. Middle East Calm: The storm is being limited within a tea cup for the moment. The potential for a dangerous boiling painful mess still exists. ‘Serenity now’ remains a mantra for those who need to pay attention as chagrin and anxiousness mix.

6. Fed Retreat: The FOMC Meeting Minutes released this week showed some Fed members remained cautious, while others banged the drum louder regarding interest rate cuts. However, a Fed Funds Rate reduction is almost a 100% certainty for the 18th of September. The question now is what the Fed will do in November. Fed Chairman Powell and a slew of other renowned global central bankers will speak today and tomorrow at the Jackson Hole Symposium. Financial institutions largely believe they know what is going to be said, but comments from Bank of Japan and Brazilian leadership could prove to be informative and entertaining for central bank nerds. Monday could be volatile for USD/BRL traders.

5. VIX: The CBOE’s Volatility Index climbed to the 56 vicinity on the 5th of August as panic grew via widespread overreactions to hyperbole ripping through the markets. The fear gauge is near the 17.55 ratio as of this writing. Market calm has resumed across the board as financial institutions and day traders have been able to achieve a pleasant tone again. Traders who use the VIX as a template regarding the potential of risks suddenly cascading into assets should keep their eyes on the index, which went to a low around the 14.45 mark on Monday. Yet, the slight incremental climb the past few days could be coming from folks still speculating on volatility which may not develop near-term.

4. Barometers: Gold is lingering slightly below 2,500.00 for the moment, this after having achieved a record high on Tuesday when it touched the 2532.00 apex. WTI Crude Oil is near 74.00 USD per barrel and is maintaining a polite value range. Speculatively, Cocoa is again above 9,000 USD per ton and Bitcoin has fought its way above 61,000 this morning. Risk appetite remains stable for the moment.

3. Forex: USD/JPY, EUR/USD, even the USD/ZAR have been able to hold onto their recent trends as USD centric weakness remains viable. Traders who were looking for huge moves in FX this week have likely been disappointed. Retail speculators need to understand financial institutions have been positioning for a weaker USD since the tail end of July. Market players may be quite pleased regarding current Forex equilibrium, which may allow technical traders the ability to take advantage of existing behavioral sentiment, this as reversals flourish and the next big wave of impetus is awaited. Next Thursday’s U.S Preliminary GDP numbers may deliver some noise.

2. Cassandras: Market experts who proclaimed a long-term stock market crash in early August have crawled back into their caves to take cover and percolate their next fear mongering tactics. This after the latest round of predicted catastrophes have vanished. While the major U.S stock indices are not at record highs, they have recovered plenty of lost ground and appear ready for more days in the sun.

1. Political Winds: The curtain closed on the Democratic National Convention in Chicago last night without a serious hiccup. Kamala Harris and Donald Trump now enter a crucial phase of campaigning, and will get plenty of attention as they go into attack mode. The next big event for Harris and Trump will be their televised debate on the 10th of September. Will the outcome prove to be a devastating storm for one of the candidates?

Anxiety and Surprising U.S Data for Day Traders to Consider

Global central banks stayed in their anticipated lanes last week as the Fed and ECB raised their key lending rates. The BoJ has admitted it is allowing its yield curve to increase, meaning the Japan government is cutting back on purchases of Japanese bonds. Forex produced anxiety and choppy results for day traders.

Gold 6 Months Chart as of 30 July 2023

Economic data from the U.S last week provided a strong Gross Domestic Product result on Thursday, and followed with weaker than expected Personal Consumption Expenditures and Personal Income statistics before going into the weekend. Meaning the U.S economy appears to be surprisingly solid, while inflation pressures do indicate they are in decline. The Forex market turned volatile on Thursday and Friday, gold which traded at nearly 1980.00 USD on Thursday went into the weekend near 1959.00.

VIX Index 1 Year Chart as of 30 July 2023

Stock markets in the U.S via the major indices continue to incrementally rise and folks waiting for a big sustained selloff are having their patience tested. Perceived volatility in U.S markets is very low and the VIX (Volatility Index) indicates many investors are not taking the time to hedge with options because their confidence is remarkably high. A cautious reminder for traders, one bad day could change all of the optimistic sentiment.

In the cryptocurrency world, folks should continue to keep their eyes on the Binance exchange and its Binance coin. Many digital assets seem to be suspiciously close to important support levels as this week begins and appear vulnerable.

Monday, 31st of July, China Manufacturing PMI – while U.S data surprisingly improves, China has not begun to show signs of a positive turnaround quite yet, and this reading is expected to be below last month’s outcome. China data is a solid barometer of global economic health and traders should give these results proper attention.

Monday, 31st of July, E.U Consumer Price Index Flash Estimates – the European CPI numbers are expected to come in slightly below the previous month’s reading. If for some reason these inflation numbers are higher than expected, this could cause some chaos briefly for the EUR/USD. A weaker number however offers no sound wagering basis for short-term day traders either. Behavioral sentiment appears to be ruling the EUR/USD landscape for the time being, and technical levels should be watched.

Tuesday, 1st of August, Australia Reserve Bank Cash Rate – the RBA is expected to follow in the footsteps of the Fed and ECB and raise its lending rate by 0.25%.

Tuesday, 1st of August, E.U Manufacturing PMI – Germany and France are anticipated to produce similar results to last month’s outcomes. Recessionary pressures are a concern in the E.U and better than expected numbers would be welcomed, but this may prove difficult to demonstrate as economic conditions remain challenging.

Tuesday, 1st of August, U.S ISM Manufacturing PMI – the results from the manufacturing sector in the States should be watched. A slight improvement is expected, but the reading is not expected to produce a wildly optimistic result. An outcome which slightly beats expectations, but is not too strong might make the USD slightly weaker. Global investment institutions are likely hoping for any signs that the Federal Reserve will have to become less aggressive. A lackluster to ‘fair’ ISM Manufacturing PMI result could be evidence larger Forex traders want to see if they are aiming for bearish momentum in the USD.

NZD/USD 3 Months Chart as of 30 July 2023

Wednesday, 2nd of August, New Zealand Employment Change – the jobs statistics are expected to show slightly weaker results from the nation. The NZD/USD remains within the lower elements of its long-term price range. There are many NZD/USD bullish traders waiting for a sustained reversal higher, but it is unlikely to be produced from these New Zealand jobs numbers.

Thursday, 3rd of August, U.K BoE Monetary Policy Summary and Official Bank Rate – the Bank of England remains in a difficult spot and it will likely raise interest rates by another 0.25%. Criticism of the Bank of England has been loud in Britain, but the BoE likely feels it has to remain in line with the Fed and ECB. Recessionary pressures continue in the U.K and inflation remains problematic. Concerns will be heard regarding property mortgages for home owners if the BoE hikes. The GBP/USD will certainly move depending on the rhetoric from the Monetary Policy Summary and talking points delivered by BoE Governor Andrew Bailey.

Friday, 4th of August, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs data parade will climax at the end of the week, this after starting on Wednesday via the ADP jobs numbers. Investors will watch the Non-Farm Employment Change data carefully and correlate them to the better than expected GDP results from the 27th of July. The wages data from the Average Hourly Earnings is expected to come in with a slight decrease. A weaker inflation result from the wages statistics could cause additional softness in the USD. However, recent data from the U.S has been hard to predict correctly, and day traders may want to sit on the sidelines until all the jobs numbers are digested.