Retail Traders Caught Out by Shifting Sentiment as Data Hits

Forex speculators who relied heavily on technical data solely last week were likely punched in the gut by the rather surprising numbers from the Consumer Price Index results in the U.S last Wednesday, particularly if they were on the wrong side of trading trajectories. U.S inflation has shifted sentiment within many large investors with a rather seismic move regarding mid-term outlooks. Financial institutions which have been counting on cuts to the Federal Funds Rate have had to take a step backwards.

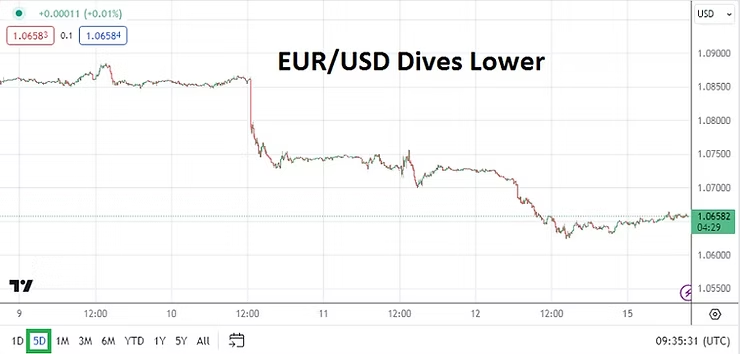

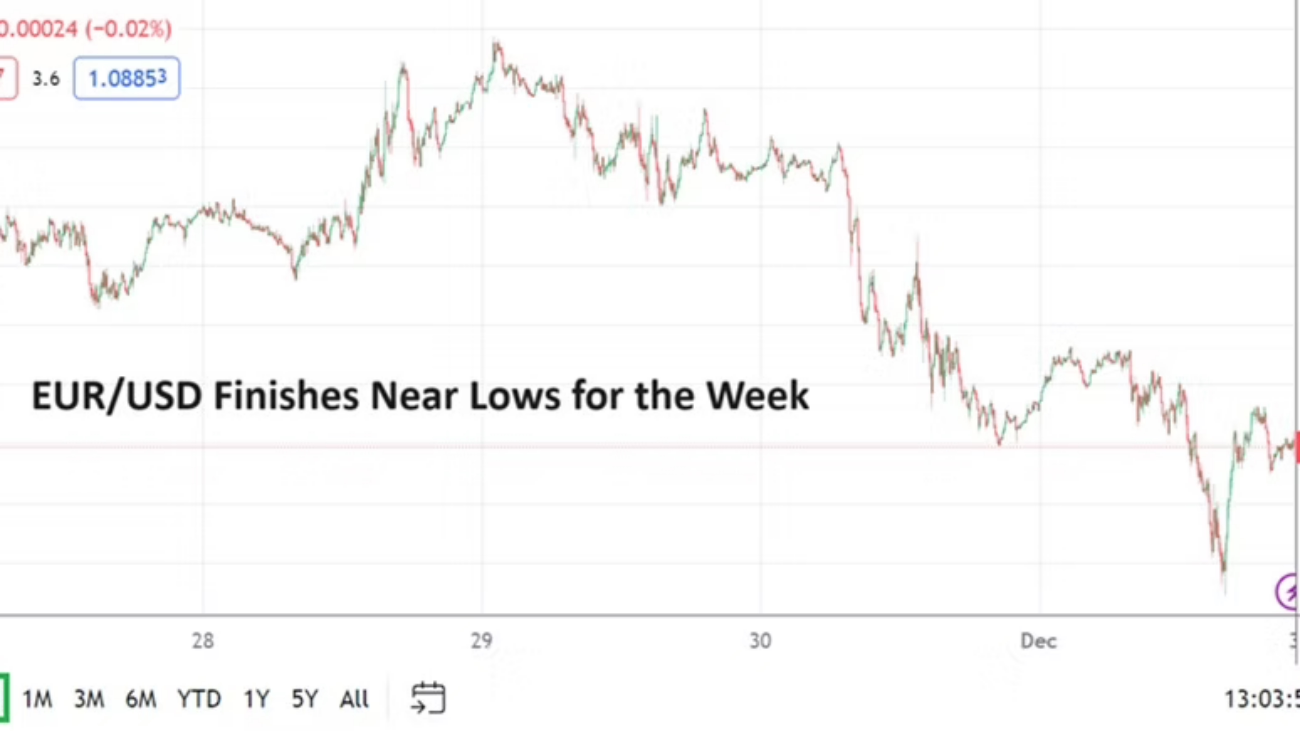

EUR/USD Five Day Chart as of 15th April 2024

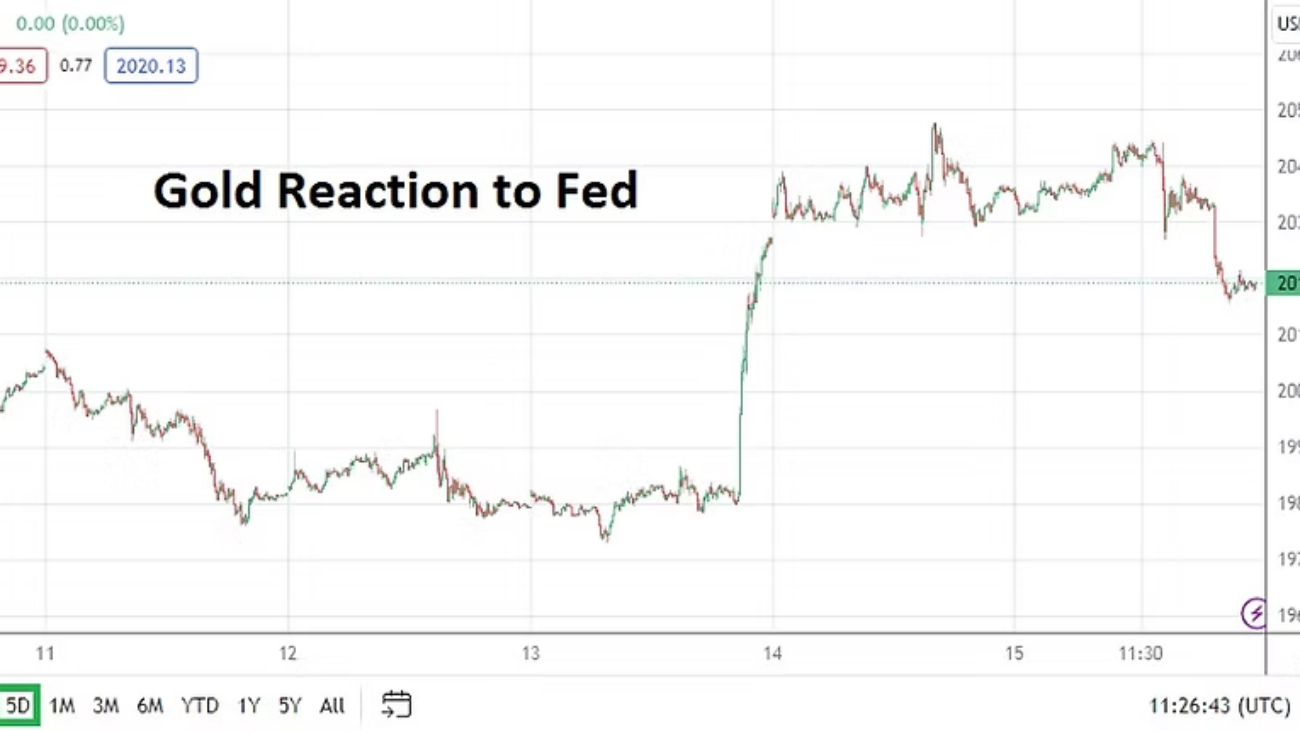

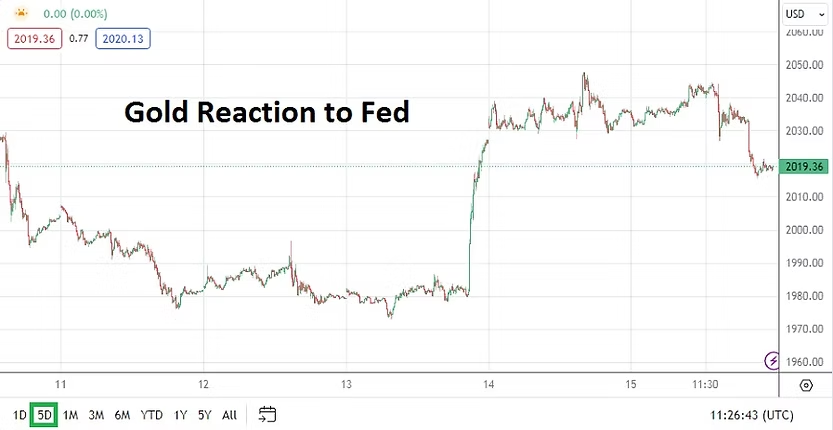

The dynamic momentum in Forex hit major currency pairs in the middle of last week and washed away support and resistance levels within a blink of the eye. Behavioral sentiment turned U.S Treasuries yields upwards and the major equity indices also experienced nervousness. Volatility also continued in Gold as new record values were produced, and then were followed by a rather strong reversal lower which likely hurt over-leveraged day traders.

Gold Five Day Chart as of 15th April 2024

Not only were U.S inflation numbers important last week, but geopolitical noise became heightened. Perhaps the climb in Gold before the weekend was helped by the anticipated conflict between Iran and Israel which did play out. The price of the precious metal and WTI Crude Oil have been more tranquil early today, which may be a signal for the moment that large market players are calm.

Monday, 15th of April, U.S Core Retail Sales – after last week’s larger than expected increase in the CPI results, the spending report today will get attention from financial institutions. Last Friday’s Preliminary Price Expectations reading from the University of Michigan did not allow investors to rest when it came in with a 3.1% elevated mark. If today’s Retail statistics are above expectations, this could make Forex roil again.

Tuesday, 16th of April, China Industrial Production and Gross Domestic Product – these economic reports will be watched closely by international investors. While there have been murmurs that China’s economy is improving, and media reports that the Biden administration is trying to engage diplomatically, the industrial and GDP results are expected to be weaker than the previous month’s outcomes. China will also release Retail Sales figures.

GBP/USD Five Day Chart as of 15th April 2024

Tuesday, 16th of April, U.K Claimant Count Change – last Friday’s GDP report from Britain did not produce any significant surprises. The U.K economy continues to struggle, but like most spheres inflation remains a problem. The GBP/USD sunk violently last week, while many speculators may believe it is currently oversold they may want to remain cautious.

Because of the U.S Federal Reserve’s own perilous fight against inflation, there are some who believe the Bank of England may need to cut interest rates before the U.S central bank. However, given the lack of proactive characteristics from the BoE and ECB which have been on full display as they dance in step with the Federal Reserve, this makes a BoE cut before the Fed a skeptical notion for the time being. The GBP/USD will stay largely USD centric even in the wake of this U.K employment report.

Tuesday, 16th of April, U.S FOMC Members – a parade of Federal Reserve voting policymakers will speak at various events, this includes Fed Chairman Jerome Powell. There will likely be little in the way of surprises from the Fed members as they likely all stick to ‘party’ lines and emphasize a cautious outlook.

Wednesday, 17th of April, U.K Consumer Price Index – the inflation report could prove to be catalyst for the GBP/USD. If the CPI number does come in weaker than expected it could spur on behavioral sentiment shifts regarding the potential for changes to BoE policy. Because the GBP/USD was so volatile the past week, day traders should be prepared for rather combustible price action from the currency pair which may look counter-intuitive. Smaller speculators should remember that ‘smart money’ from larger players may be positioned for the results of the U.K CPI data already.

Thursday, 18th of April, U.S Weekly Unemployment Claims – although not the most significant of reports usually, financial institutions are ‘waiting’ on a change of statistical direction via labor market evidence. If jobs numbers start to come in weaker than anticipated – meaning there are higher jobless claims – then the USD could react with some selling.

Friday, 19th of April, U.K Retail Sales – having endured a rather wild trading cycle, Great Britain will deliver one more important economic report to end this week. The GBP/USD will react to the consumer spending results.

USD and the Fed: Parade of Jobs Data Ready to Make Noise

U.S data last week created landmines for Forex speculators and the Federal Reserve. Global financial markets return to full action today following the long holiday weekend. Growth and inflation numbers from the States last week provided more unsettling results for financial institutions. While Forex has proven difficult for many traders, the major equity indexes are flirting with highs but also running into some intermittent headwinds.

US Dollar Index Six Month Chart as of 2nd April 204

In December of 2023 the Fed was interpreted as having confirmed it would be able to cut the Federal Funds Rate during the 2024 calendar year rather consistently. Dovish policy had been anticipated by financial institutions which began to sell the USD aggressively in November. But by the end of the Christmas week the USD had essentially hit lows in many major currency pairs, and as January started reversals intensified.

The last three months of trading has produced choppy conditions in Forex, but one thing is clear – financial institutions no longer believe the Federal Reserve will be able to aggressively cut the Federal Funds Rate. The Fed has now begun to show signs that it is nervous regarding U.S economic data, this as growth via GDP numbers has remained firm, inflation sticky, and consumers resilient. Clouds shadow Forex and day traders have been hampered by a lack of solid trends.

Gold Six Month Chart as of 2nd April 2024

Gold is trading near record price levels. The fact that the precious metal is touching all-time values as the USD has been strong has flustered some speculators. But traders need to remember Gold is affected by large players, including nations, that may be hedging USD bets and preparing for political instability. The price of Gold may underscore belief the U.S Fed will have to cut rates at least a couple of times this year no matter the economic facts on the ground, because this is an election year and if the central bank doesn’t deliver on its ‘promise’ jobs at the Fed may be at stake.

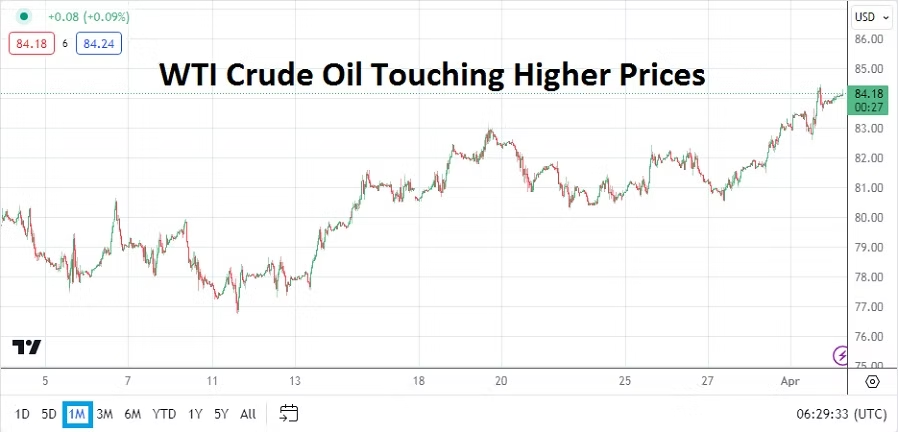

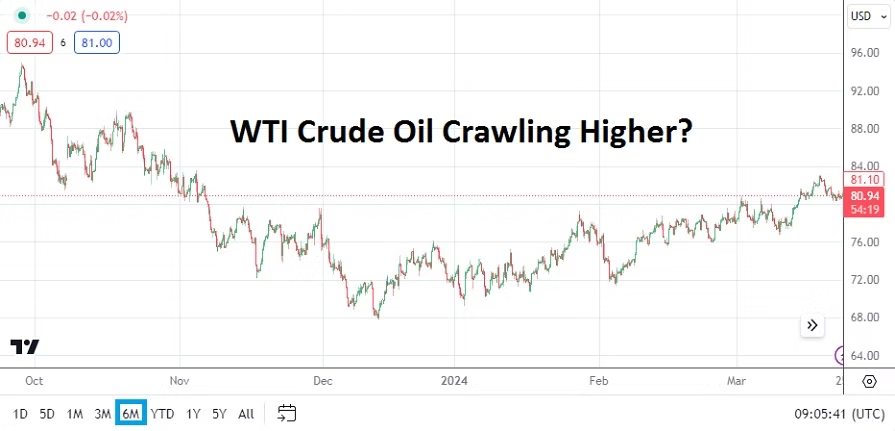

WTI Crude Oil One Month Chart as of 2nd April 2024

Not making anything easier for Federal Reserve policy is the higher price of WTI Crude Oil which has reached the 84.00 USD per barrel price. If energy costs go higher this will not help the fight against inflation. OPEC will be conducting a meeting this week. As an aside the price of Cocoa per metric ton is now over 10,000.00 USD, which is more expensive than Copper. While the price of Cocoa is not a game changer for global financial markets, the higher price will make chocolate more expensive, which some traders may find disagreeable as they try to relax and watch their speculative wagers while trying to nibble on their favorite snack.

Monday, 1st of April, U.S ISM Manufacturing – both the Purchasing Managers Index reading and the Price numbers came in higher than expected. The stronger results show the U.S economy remains better than anticipated by the Federal Reserve, which has been counting on its higher interest rate to slow down growth and inflation.

EUR/USD Six Month Chart as of 2nd April 2024

Tuesday, 2nd of April, European Manufacturing PMI – the European Union and Great Britain will release their business readings today. The results will demonstrate insights regarding sentiment. Financial institutions are worried the European Central Bank and Bank of England may have to consider lowering their interest rates before the Federal Reserve. The EUR/USD and GBP/USD will react to the results.

Tuesday, 2nd of April, U.S Federal Reserve FOMC Members – there will be appearances throughout the day in the U.S from various Federal Reserve members who will make the case for their monetary policy outlooks. It should be noted that Jerome Powell will be speaking on Wednesday. The JOLTS Job Openings will come out before the FOMC members speak. While the JOLTS report will not cause earth shattering reactions, the jobs data is the beginning of the parade regarding employment statistics for this week.

Wednesday, 3rd of April, U.S ISM Services PMI – taking into account the Manufacturing report came in stronger than expected on Monday, the Services data will be watched by financial institutions. If this report is better than anticipated, USD sellers will not rest easy. The ADP Non-Farm Employment Change data will also be released on this day.

Thursday, 4th of April, U.S Weekly Unemployment Claims – the Federal Reserve has been counting on employment strength to erode based on their notion that higher interest rates would create ‘lagging’ reactions in the jobs sector. Jerome Powell has said the Fed is anticipating weaker employment data. The results from the weekly report will not be as significant Friday’s data, but should be given attention by day traders in Forex.

Friday, 5th of April, U.S Non-Farm Employment Change and Average Hourly Earnings – the climax for speculators this week will be these jobs numbers from the States. If the numbers produce less hiring than expected this would help USD bearish momentum. Wages will also prove crucial regarding behavioral sentiment for financial institutions. Simply put, the Federal Reserve is anticipating that weaker employment numbers are going to be seen, if this doesn’t happen it might cause major volatility in Forex going into the weekend.

Forex Volatility and Coming Data Attractions for this Week

Nervous trading results have hurt many day traders and likely financial institutions too, as behavioral sentiment in Forex gets blindsided by rather mixed U.S data and the Federal Reserve not giving a definitive answer regarding monetary policy. The violent trading in the USD last week was expected, but the turbulence that many Forex pairs experienced on Thursday and Friday of last week was rather vicious. For all the perceived sophistication of Forex markets via financial institutions, the trading results last week point to a definite fear of the unknown.

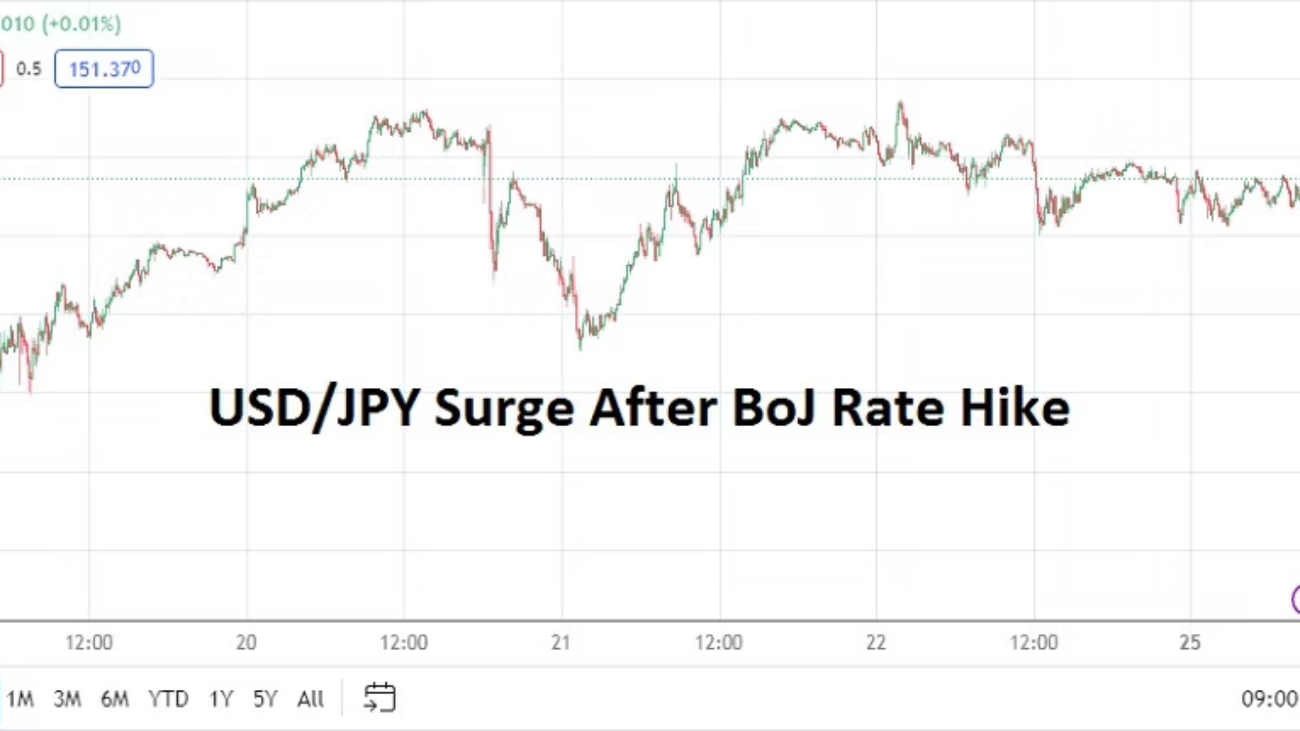

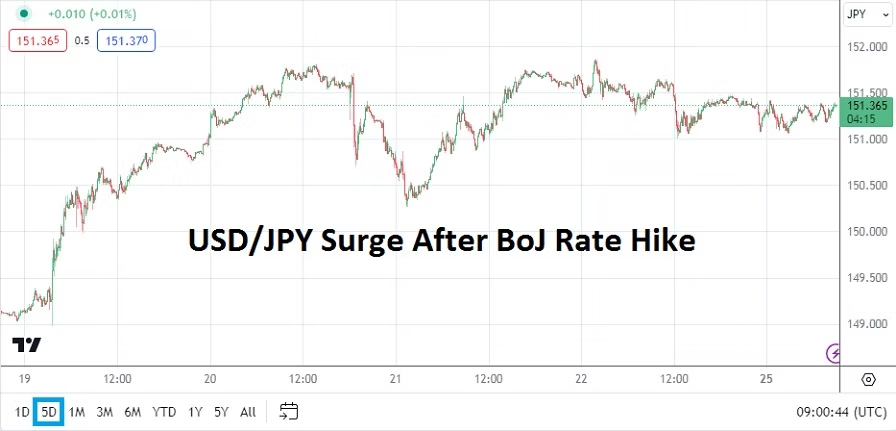

USD/JPY Five Day Chart as of 25th March 2024

While the Bank of Japan finally changed its interest rate policy and moved to a Policy Rate of 0.10% early last week, this did not create selling momentum in the USD/JPY. The Federal Reserve’s dangling of potential interest rates to come this year caused temporary weakness in the USD, but as financial institutions and their clients looked at the prospects for a more dovish Fed they apparently became unimpressed as the days passed.

WTI Crude Oil Six Month Chart as of 25th March 2024

The Fed seems to be betting on weaker jobs numbers developing, and there has been data which points to part-time jobs increasing, and full-time jobs becoming harder to find in the States. Jerome Powell said last week that if jobs numbers start to show weakness that the Fed would be willing to begin cutting interest rates even if inflation remains sticky. Lagging economic data correlations have not eased the Fed’s problems.

The Fed has also admitted inflation in housing, transportation and food remains problematic. WTI Crude Oil spent much of last week above 80.00 USD per barrel as its price has begun to show signs of rising incrementally again; and there is little the Fed can do about more expensive energy costs should they be seen. Higher costs for logistics will not make anything cheaper. Pricier mortgages, more expensive rent and insurance rates for cars and gasoline is creating serious knock on effects.

And for the sake of acknowledging the screaming prices in Cocoa, please have a look at the chart below which should explain why your chocolate products are going to be more expensive in the coming months. The price of the most delicious commodity in the world has tripled in less than a year’s time and is around 8931.0 USD per metric ton as of this writing.

Cocoa One Year Chart as of 25th March 2024

Gold turned in a violent week of trading too as it reached 2224.00 last Wednesday, only to fall back to a known value around 2165.00. Day traders are dealing with violent cycles in Forex because sustained trends have been nearly impossible to find. While U.S equity indices are fighting upwards, speculators who are afraid of heights are likely being cautious if they are betting merely on the daily results from the S&P 500, Nasdaq 100 and Dow Jones 30 instead of investing for the long-term.

This week’s coming data from the U.S is important, financial institutions are already dealing with plenty of noise, and they will have to be careful regarding their interpretations regarding the coming economic statistics. Meaning day traders who are speculating in all financial assets should use risk taking tactics that are planned significantly in advance.

Monday, 25th of March, U.S New Home Sales – a slight gain is expected, but mortgage rates continue to shadow the housing sector and cause concerns.

Tuesday, 26th of March, U.S Consumer Confidence via the Conference Board – the reading is anticipating a slight increase. Consumer numbers from the U.S have come in mixed recently. A stronger result than estimated might not be welcomed by traders with bearish sentiment regarding the USD. The Fed wants its cake and to eat it too, they would like to see weaker consumer numbers and a soft economic downturn. If U.S shoppers remain confident this could help sustain inflation. It should be noted too, that Core Durable Goods Orders data will be released one and a half hours before the Consumer Confidence numbers.

AUD/USD Six Month Chart as of 25th March 2024.

Wednesday, 27th of March, Australia Consumer Price Index – inflation numbers are expected to come in slightly higher than the previous results. Like most other central banks, except for the BoJ, the Reserve Bank of Australia would enjoy seeing inflation erode. The AUD/USD will react to the results certainly, but the price action might prove complicated because of USD centric notions.

Thursday, 28th of March, U.S GDP, Weekly Unemployment Claims, Pending Home Sales, and Revised Consumer Sentiment from the University of Michigan – put bluntly day traders will have to be well prepared for the combination of data from the States. Spectators who do not have large trading accounts and cannot take on a great amount of risk, should seriously consider sitting on the sidelines until most of the data is published. The GDP numbers will be watched carefully, while they are expected to match last month’s total, any surprises will affect the USD immediately in Forex. Weaker growth numbers might cause USD sellers to ignite positions.

However, before traders react too much to the Gross Domestic Product numbers, the Weekly Unemployment data will also impact the financial market. Financial institutions are anticipating a higher amount of unemployment claims this week. Also, at the same time as the growth and jobs numbers, the Final GDP Price Index numbers will be brought forth. The mixture from these reports could cause speculative whiplash.

The housing sector numbers and consumer numbers which come one and a half hours later will finish off a very big day for traders and institutional investors. The wide array of data could make this coming Thursday rather loud, and again rather dangerous for retail traders to participate.

Friday, 29th of March, Japan’s Tokyo Core Consumer Price Index – the inflation numbers are expecting to show a slight decrease to 2.4%. The result should certainly be watched by USD/JPY and GBP/JPY traders. If the number were to come in higher than expected, this could cause additional volatility for the Japanese Yen. Financial institutions seemed to indicate last week they would like to see the BoJ become more aggressive with their Policy Rate.

Friday, 29th of March, U.S Core Personal Consumption Expenditures Price Index – the reading is expected to be below the previous month’s total. Traders should be on the lookout for revisions to past results. Financial institutions know this inflation number is important for the Federal Reserve, but they are concerned the U.S central bank doesn’t have the ability to combat inflation which is not part of the Core number. Energy and food costs which are hurting U.S consumers are not part of this report and likely making the Federal Reserve gun shy regarding monetary policy – which has caused a large part of the USD whipsaw trading results that Forex has experienced.

Forex: Powell, ECB and U.S Jobs Numbers as Gold and Oil Run

Day traders and investors received a dose of optimistic ‘news’ last week as U.S economic data came in weaker than expected. While Forex certainly proved choppy as anticipated, the USD has shown signs of stability and perhaps has created a durable resistance level up above regarding its potential value looking into the mid-term.

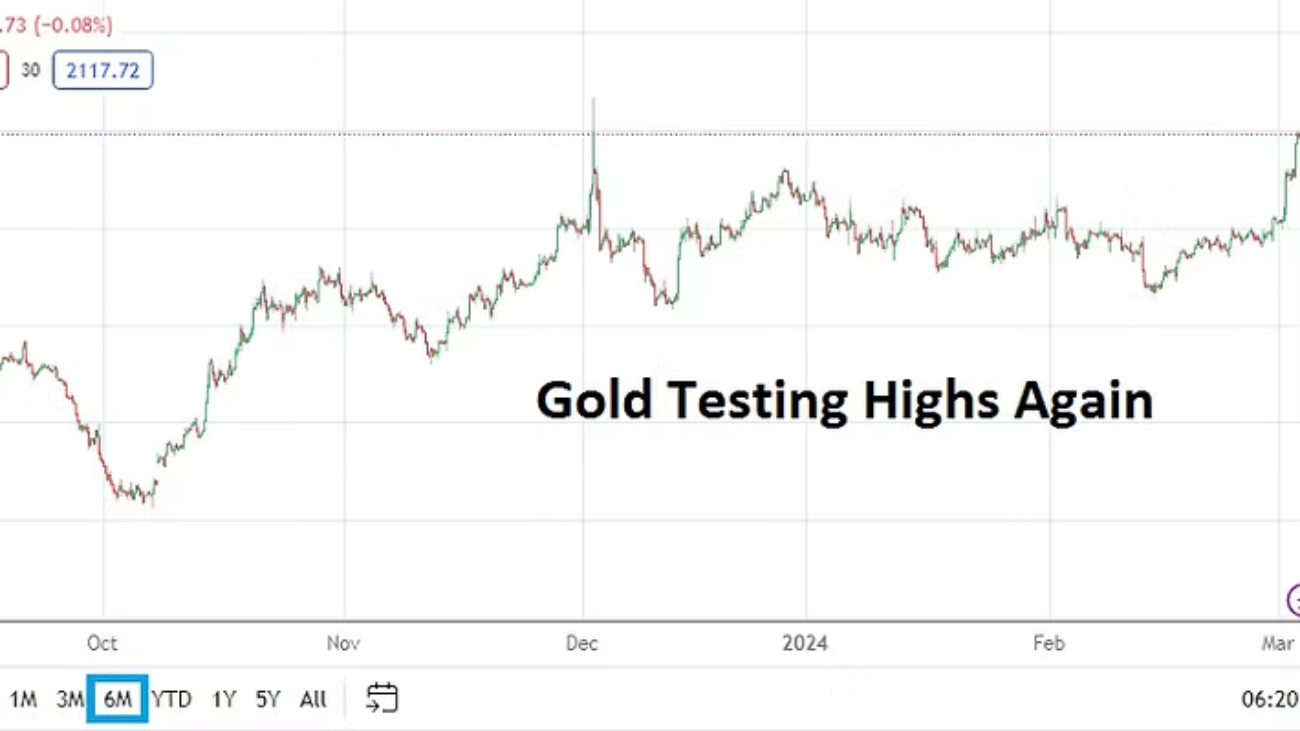

Gold Six Month Chart as of 5th March 2024

A potential telltale sign regarding the USD in Forex is the current price of Gold which is testing highs and as of this writing is near 2115.00 USD. While below the speculative heights of early December, the precious metal is above prices seen in late December when the USD was being sold heavily. The value of Gold is a rather solid barometer regarding outlook for behavioral sentiment in Forex. A weaker USD translates into a higher Gold price in many cases.

U.S Treasury yields have also decreased slightly over the past handful of days. And while U.S equity indices are within sight of record values, traders should monitor developing news regarding U.S regional banks and concerns about New York Community Bancorp (NYBC). For the moment it appears investors have not turned too nervous when considering the bigger picture of stock markets. Perhaps last year’s regional bank crisis has made investors in equity indices feel immune to fears of contagion stemming from bad commercial real estate lending. Or perhaps many folks are marching along merrily and refuse to pay attention for fear of missing out when their associates continue to parade into the indices.

The cryptocurrency market has come out of its deep freeze and sunshine is pervading the mindsets of speculative gamblers in crypto assets. U.S run ETFs are raising a lot of money. Folks have driven the market sky high again in the digital asset Bitcoin and its fellow travelers like Ethereum, Binance Coin, and there have been signs of pure casino like wagering in Dogecoin and Shibu Inu. Be carefu if you are considering dipping your toes into this ‘market’. Volatility and changes of sentiment can happen in the flick of an eye.

USD/JPY Six Month Chart as of 5th March 2024

Monday, 4th of March, Japan Capital Spending – a huge jump of 16.4% was reported yesterday. This points to better economic sentiment. The Bank of Japan has been getting a lot of attention the past handful of months because some financial institutions expect the BoJ’s monetary policy to begin changing. The USD/JPY remains near important resistance levels, but below the highs of last October and November 2023 values. Mid-term speculators may be leaning towards bearish sentiment in the currency pair, but a trend lower has not been established yet.

Tuesday, 5th of March, U.S Service PMI via ISM – last week’s growth and inflation data from the U.S was less than expected. While the U.S economy has shown rather stubborn growth, the American economy may be showing signs of slowing. Today’s reading is expected to come in below the previous month’s outcome.

Wednesday, 6th of March, U.S Federal Reserve Chairman Powell – the Fed chief will testify before the Senate via the Semi-Annual Monetary Report over a two day span. Because it is an election year a rather aggressive amount of questions will be asked. However, Powell is a skilled speaker and it unlikely he will be rattled by political rhetoric. Of interest will be any comments regarding inflation, this as the Fed Chairman is asked for insights regarding the Federal Funds Rate outlook. While this testimony in Washington D.C is usually a polite get together, the notion that some politicians may try to score points will make this a potentially important calendar event for investors to pay attention regarding financial market gyrations. Powell is expected to remain cautious regarding his answers.

WTI Crude Oil One Year Chart as of 5th March 2024

Wednesday, 6th of March, U.S Crude Oil Inventories – last week’s U.S supply report posted increased results, yet the price of WTI Crude Oil jumped the end of last week. The value of the commodity remains within the lower part of its one year range and should be watched. Recent speculative action has shown some buying momentum. The price of energy is a big component within global inflation and should be watched as the 80.00 USD Crude Oil level is challenged.

EUR/USD Six Month Chart as of 5th March 2024

Thursday, 7th of March, European Central Bank Main Refinancing Rate – once again the ECB is expected to not act. The question is if financial institutions may try to send the European Central Bank a message because of its ‘inaction’ as inflation remains stubborn in Europe and growth hard to achieve. The EUR/USD has returned to value above the 1.08000 mark again, but visions of a stronger EUR have been hard to attain. The combination of the ECB Monetary Policy Statement and Press Conference, as Fed Chairman Jerome Powell is addressing politicians in Washington D.C could make for an interesting day of volatility in Forex.

Thursday, 7th of March, U.S State of the Union – President Joe Biden will deliver his address to Congress.

Friday, 8th of March, U.S Non-Farm Employment Change and Average Hourly Earnings – weaker jobs numbers and diminishing wage escalation are expected. U.S economic data last week came in below estimates. This report will be a solid barometer for financial institutions. While the work force numbers in the U.S are said to be tight – meaning there is full employment – layoffs have certainly been taking place in some sectors. Also worth paying attention to in the ‘back pages’ of the report, will be the amount of average hours worked by employees which have seen a statistical decline emerge.

AMT Top Ten Miscellaneous Raindrops for 16th of February

10. Bitcoin is trading within sight of 52,000.00 USD, the digital asset was trading near 38,700.00 on the 23rd of January, which is over 34% in less than a month. That’s a lot of air in the balloon folks.

9. Gold: The precious metal has climbed above 2000.00 USD, this after a drop to 1985.00 USD on the 14th of February. Sentiment is uneasy.

8. Not April Fool’s Day: Iran has announced ‘plans’ to build a naval base on Antarctica, after declaring ‘property rights’.

7. WTI Crude Oil: The price of the commodity continues to battle the 77.00 USD level. Higher energy costs will not be looked on favorably by inflation hawks.

6. U.S Treasuries: Yields should be watched today after having provided anxious results this week, U.S equity indices will continue to react to the ‘bonds’ market.

5. Nvidia: After delivering superlative results in 2023, the company has announced the release of Chat with RTX, which allows independent AI chatbot capabilities to interface with your own documents, videos, etc., providing insights from personal queries.

4. Chinese Property: Investments dropped by over 9% in 2023. China’s government faces a clash between socialistic ideology in order to help the market versus practical supply and demand realities.

3. U.K: Gross Domestic Product numbers came in with negative results yesterday for Britain, the combination of recessionary GDP and stubborn inflation is stagflation. Bank of England faces a difficult decision. Will the BoE get proactive and cut interest rates before the Federal Reserve? GBP/USD is below 1.25800 this morning.

2. Data: Stronger than expected U.S CPI statistics caused bedlam on Tuesday, but yesterday’s Retail Sales came in weaker. The ‘disappointing’ consumer spending numbers were likely welcomed by the Federal Reserve and financial institutions. Producer Price Index statistics will be published today, surprise inflation results could jostle financial markets.

1. Forex: Day traders witnessed whipsaw results early this week and should remain cautious going into this weekend. Patience will be needed as USD centric outlooks adjust to nervous shifts in behavioral sentiment.

Friday's Forex Violence and Coming Attractions for Traders

While the past month has continued to produce positive trends upwards for traders speculating on equities via U.S indices with record breaking values, Forex has been rather brutal for many day traders if they have remained stubborn.

Short-term trading conditions in Forex again proved violent this past Friday, as the Non-Farm Employment Change and Average Hourly Earnings reports came in stronger than anticipated and set off fireworks in the major currency pairs.

Fed Chairman Jerome Powell offered a clue to speculators paying attention last Wednesday, during the Fed’s Press Conference in which he spoke about the tight labor market. It seems likely the Federal Reserve knew the jobs data was going to be rather robust and hinted.

The Federal Reserve did continue to speak about interest rate cuts, but they certainly have not given an exact timetable when more dovish policy will begin. This has left many speculators, corporations and financial institutions nervous and the results via choppy trading conditions the past handful of weeks are proof.

USD strength the past month has caused headaches for many Forex speculators, but it needs to be said that many major currency pairs are lingering near values post-December 13th 2023, this was when the Federal Reserve made it ‘official’ that a more dovish monetary policy would develop in 2024.

Early wagers by financial institutions in December indicated they believed a March Federal Funds Rate cut would be seen, but after last Wednesday’s Fed’s FOMC Statement and Friday’s jobs numbers it seems more likely for the moment a May interest rate cut could be a legitimate target.

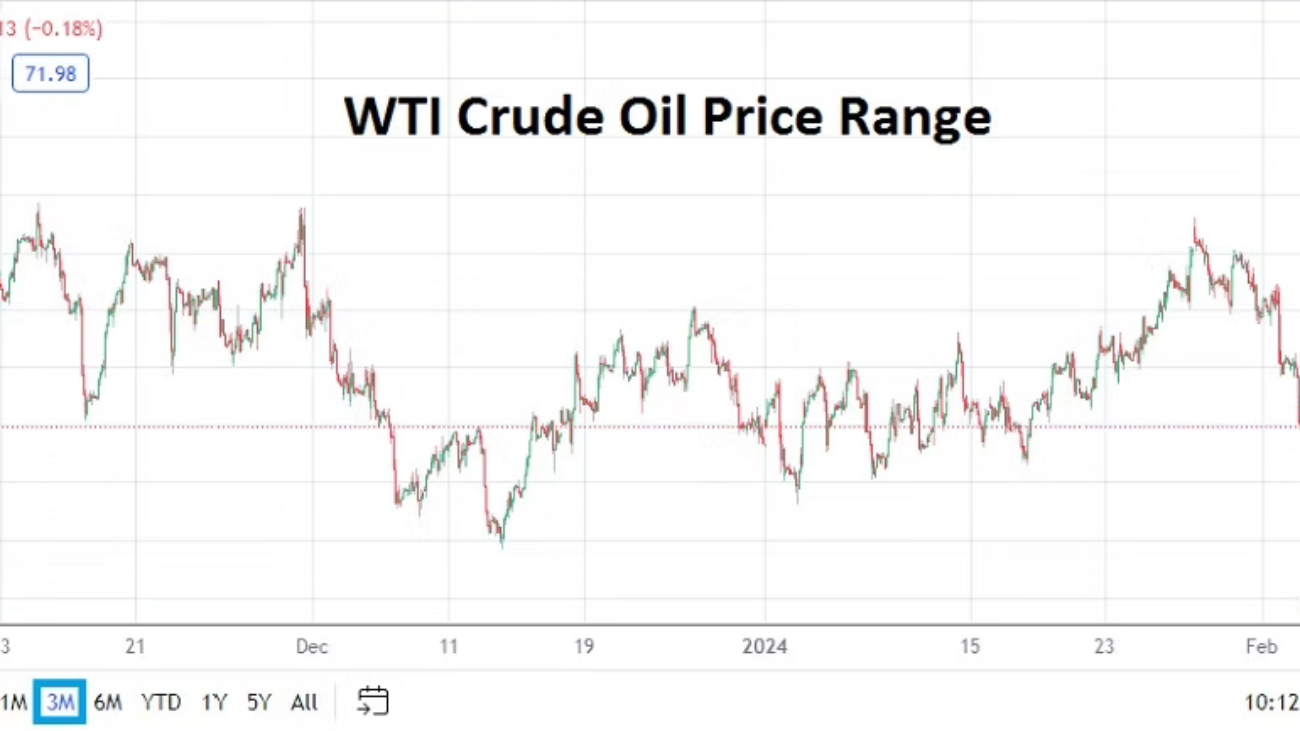

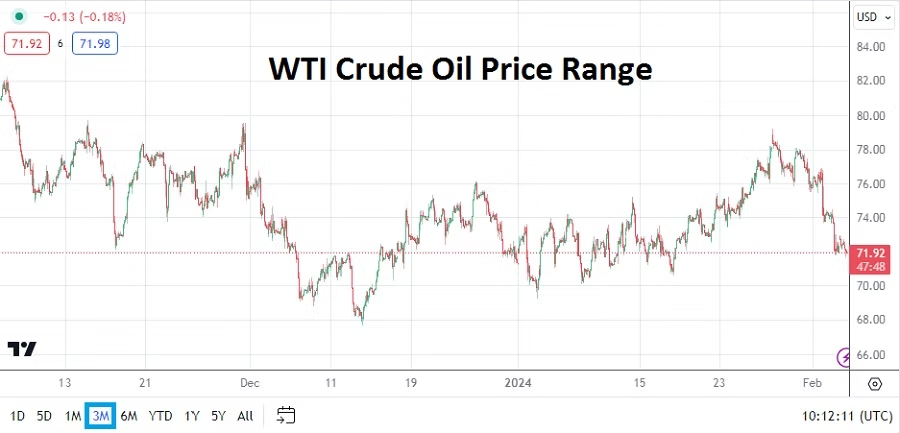

WTI Crude Oil Three Month Chart as of 5th February 2024

Risks do Abound and Speculators Should Remain Cautious Near-Term

Inflation concerns via knock-on affects from logistical complications via Red Sea chaos which disrupts the Suez Canal shipping is a legitimate threat and needs to be monitored. However, the price of WTI Crude Oil traded in a remarkably stable manner last week as noise was heard from the Middle East. In early price action this morning the commodity has been polite and remains within sight of 72.00 USD per barrel. The lack of a nervous reaction in Crude Oil thus far could keep global investors calm.

This week will be limited regarding important economic data. However, there will be plenty of rhetoric offered by U.S Federal Reserve members in the coming days via conferences and interviews. Forex traders have needed to combat an array of reversals as price equilibrium has created rather tenacious price realms and this may continue near-term.

There are time periods when traders should be willing to accept that methods regarding short-term trading tactics need to be adjusted. January has shown that financial institutions were of the mindset the USD had gotten too strong. And although it appears financial institutions continue to lean towards a weaker USD outlook in the mid-term (as proven by lower moves in the USD leading up to the jobs report on Friday), the surprisingly good jobs data certainly caused the USD to bounce upwards.

Technical considerations of the USD at this moment are important, fundamental data is still coming in rather mixed, this as financial houses wait on central banks to start reacting with interest rate cuts due to lackluster economic data. It is important to note that some analysts have started to murmur the ECB and BoE may have to move first regarding interest rate cuts – if they have the courage to take this action sooner rather than later. The U.S economy has remained rather strong regarding consumer sentiment and this is causing angst among Fed observers. The U.S jobs numbers on Friday highlighted this nervousness.

Monday, 5th of February, U.S Services PMI via ISM – an outcome of 52.0 is the expected reading, which would be higher than the previous result of 50.6. If the Services number meets its estimate and doesn’t exceed the expectation, this would calm nervous financial institutions which may believe the U.S economy may be too strong for the Federal Reserve’s liking, and cause some hawkisk sentiment regarding monetary policy to linger. A weaker number from the Services PMI could help the USD selloff slightly, a stronger outcome could result in more USD buying short-term.

Tuesday, 6th of February, Australia Cash Rate and Monetary Policy Statement via RBA – no major changes are expected from the Reserve Bank of Australia. Global central banks have taken a wait and see approach as they likely remain nervous regarding the potential of inflation to remain stubborn in the mid-term. The RBA is probably going to follow the ECB, BoE and Fed’s stances from last week and remain conservative.

EUR/USD Six Month Chart as of 5th February 2024

Wednesday, 7th of February, Germany Industrial Production – though this report is not viewed as a major economic event for traders the results should be watched. The EUR/USD has been hit by rather volatile conditions as financial institutions try to anticipate central bank moves. If the German data comes in weaker than expected (a minus -0.4% result is anticipated) this could make the EUR/USD slightly more bearish.

Shanghai Composite Index One Year Chart as of 5th February 2024

Thursday, 8th of February, China CPI and PPI – economic data from China has not improved and foreign investors are not showing an appetite for risk. Deflation remains a concern in China, and although the official government rhetoric promised sunnier days ahead, fundamentals in real estate, manufacturing and consumer driven data offers troubled prospects. The Consumer Price Index from China is anticipated to be worse than the previous month’s outcome. The downturn in the SSE (Shanghai Composite Index) is now challenging the 2,700.00 vicinity.

Friday, 9th of February, Canada Employment Change – Canadian economic data has been lackluster and analysts have been quite critical of government policy. Having said this the USD/CAD is largely going to stay in a USD centric mode going into the weekend.

AMT Top Ten Miscellaneous Flakes for 19th of January 2024

10. Music: Come On, Come Over performed by Jaco Pastorius. The bass playing on this song is magnificent.

9. Cybersecurity: Prospect of quantum computing is making Central Banks nervous, quantum development will impact blockchain and make current payment systems vulnerable and perhaps obsolete. Post-quantum cryptography development is vital.

8. Frigid Weather: Tesla owners have dealt with battery power failures as winter temperatures have plummeted in Chicagoland and elsewhere. EV energy solutions need to improve.

7. China: Over the past 11 months FDI (foreign direct investment) has dropped more than 10% in the nation, an estimated short fall of 145.51 billion USD. China’s Foreign Direct Investment release has seemingly been pushed off to next week. Shanghai Composite (SSE) near 2832.28.

6. Energy Sector: WTI Crude Oil still priced politely as ‘interactions’ with Houthis flare. Natural Gas values remain near lows while North America suffers from a deep freeze.

5. Risk Assessment: Iran and Pakistan, although expressing ‘brotherly love’ for each other, have exchanged missiles across their respective border aimed at extremists.

4. U.S Treasuries: Inversion has almost ended completely, 5-Year Notes up to 30-Year Bonds yields have returned to ‘norms’.

3. Gold: Price of the precious metal near 2027.00 USD having bounced higher after challenging the 2000.00 vicinity on Wednesday.

2. Data: Consumer Sentiment reading via University of Michigan on the schedule today, this could provide impetus to markets that appear to be waiting for the next big push.

1. FX Volatility: USD strength has pushed the greenback towards important mid-term resistance in Forex as many day traders are likely still fighting the trend.

Forex Calm After the Storm? Volatility and Coming Holidays

The weakness of the USD was anticipated last week, this as the Federal Reserve essentially admitted its aggressive interest rate hikes policy has come to an end. While Fed Chairman Jerome Powell tried to sound neutral, most financial institutions reacted to the FOMC Statement and the Fed’s Press Conference last Wednesday with a rather demonstrative amount of USD selling, largely showing they were prepared to react.

The EUR, GBP and JPY all gained, and many other currencies added value against the greenback too. Gold flourished upwards and even WTI Crude Oil came off its lows. However, after producing strong gains late Wednesday and into Thursday, gold and major Forex pairs did reverse slightly lower on Friday as the USD gained some footing.

Gold Five Day Chart as of 17th December 2023

Risk appetite likely has enough positive behavioral sentiment influence to continue its desire for dynamic buying on U.S indices. The Dow Jones Industrials will start Monday at record heights, the S&P 500 and Nasdaq Composite are approaching one year highs.

Yes, potential headwinds can develop, so day traders should not bet blindly on bullish gyrations to mount without reversals being expected too. As the GBP and EUR gave back some of their gains on Friday, financial institutions may have been reacting to the notion price velocity higher had been too robust in the near-term. Speculators received another reminder that one way trends tend to meet with reversals that can still cause harm.

Risk adverse traders who have their eyes on global affairs should monitor the situation in the Red and Arabian Seas. Houthi extremists continue to fire at international ships sailing in the areas, and this may generate a reaction at some point from allied navies which are supposed to protect vessels and commerce. If the U.S Navy reacts to the Houthis in a strong manner this could deliver a cold short-term shiver into markets.

Speculators also need to understand this is the last ‘full’ week of trading before the Christmas and New Year holidays, which can cause a massive decline in volumes. This Thursday’s trading will begin to decrease from norms, and Friday’s price action will likely be affected by offices around the world starting to shutter as employees disappear for extended vacations. Day traders who want to participate in Forex, commodities, and equities via CFDs should be prepared for the emergence of quiet markets the end of this week with occasional volatility disrupting technical charts.

However, this Monday and Tuesday will pose questions regarding possible reactions to the weaker USD which has emerged, and U.S equity indices showing signs of speculative zeal. U.S Treasury yields continued to trend lower last week, and U.S bonds should be watched early to see if market participants continue their optimistic paces, or show signs of becoming more passive as the holidays approach. Traders with strong convictions regarding directions may feel inclined to remain active throughout this week and cannot be blamed, but some caution should be practiced.

EUR/USD Five Day Chart as of 17th December 2023

Monday, 18th of December, Germany ifo Business Climate – the reading is expected to show a slight improvement over the last month. EUR/USD traders may believe they should react to the results from this report, but the EUR is likely to stay within a USD centric mode driven by existing outlooks. The ability of the EUR/USD to hit the 1.10000 level late last week confirmed positive mid-term bullish outlook. The reversal lower on Friday may ignite speculative buying positions early this week, but day-traders may want to be conservative.

USD/JPY One Month Chart as of 17th December 2023

Tuesday, 19th of December, Bank of Japan Monetary Policy Statement and Press Conference – the BoJ is not expected to raise their interest rates quite yet. However the end of the BoJ’s negative monetary policy may be coming to an end in 2024. The BoJ bet on the notion that inflation would come down eventually, even it maintained a negative interest rate policy – this seems to have been proven correct. The USD/JPY has reacted the past month with a rather incremental decline. Perhaps Japanese financial institutions have been positioning for a stronger JPY over the mid-term. The USD/JPY trajectory lower remains intriguing for speculators.

Wednesday, 20th of December, U.K Consumer Price Index – the BoE sounded more dovish than many folks expected they would this past Thursday. Inflation numbers coming this week should be watched. The British economy remains lackluster, but sounds about ‘weaker’ inflation have been heard. The data from the CPI is expected to be slightly lower than the previous month. The GBP/USD could react to this report. The British Pound has delivered upwards momentum since late October. Traders should be careful regarding potential short-term reactions from the GBP/USD, and understand Forex volumes may start to decrease on Thursday and Friday which could affect results.

Thursday, 21st of December, U.S Final Gross Domestic Product – growth in the U.S has been better than most anticipated. While many analysts are still predicting a slowdown, the GDP number is expected to show a 5.2% gain. The inflation report via the GDP Price Index is anticipated to be 3.6%. While the broad markets typically would react to these statistics in a strong fashion, trading might be somewhat muted as financial institutions begin to focus more on the coming holidays.

Friday, 22nd of December, Canada GDP – a slight gain of 0.2% is expected regarding the growth statistics. Markets will be quiet and while the USD/CAD could see a momentary increase in trading, behavioral sentiment from earlier this week will likely have had a bigger effect.

AMT Top Ten Miscellaneous Thoughts for the 8th of December

10. Book: A History of Venice by John Julius Norwich.

9. Music: Gram Parsons (featuring Emmylou Harris) playing Ooh Las Vegas.

8. Artificial Intelligence: Speed and processing advances will continue to make AI a buzzword in 2024, this as quantum computing looms in the distance.

7. Trading Volumes: Speculators should note there are about two full weeks of trading left before ‘thin’ holiday markets will begin to be seen. Meaning financial institutions while being cautious, will also start to position their assets according to their outlooks for early next year.

6. Energy Sector: WTI Crude Oil, Brent, Natural Gas and Unleaded Gasoline continue to challenge support levels as long-term lows remain in sight.

5. China: Important inflation numbers via Consumer Price Index statistics will come from the nation early Saturday, negative results are expected.

4. Risk Appetite: Optimism continues to be encouraging within behavioral sentiment, this as U.S equities remain near highs, the USD leans towards a mid-term outlook with potential weakness, and gold stays above 2000.00 USD per ounce.

3. USD/JPY: Bearish momentum continues in the currency pair, price velocity built speed yesterday and this morning’s trading has been dynamic.

2. Data: U.S jobs numbers will be released today, the Non-Farm Employment Change and Average Hourly Earnings reports will create reactions. However, unless the results are surprising, this data may simply work as an affirmation for existing risk appetite.

1. Federal Reserve: The Fed’s next FOMC Statement will be on the 13th of December, this knowledge will shadow the broad markets today and early next week.

December Cheer, Full Volume, Considerations for Coming Week

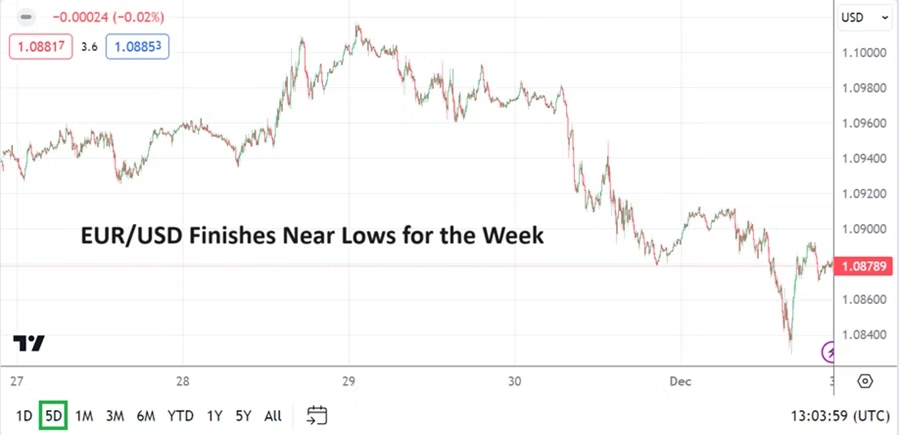

The EUR/USD finished the past week of trading below its starting point essentially closing this Friday around the 1.08790 mark. While the slight downturn may have hurt bullish day traders who kept on looking for higher ground in the short-term, the EUR/USD did trade above the 1.10000 on late Tuesday and held its ground briefly on Wednesday before starting to trend lower. A depth of nearly 1.08310 was momentarily challenged on Friday with solid price velocity, but the EUR/USD did exhibit some buying before going into the weekend.

EUR/USD Five Day Chart as of 3rd December 2023

Speculators who were looking for a higher finish for the week from the EUR/USD may have been disappointed, but the end of the trend upwards may not be finished. U.S Fed Chairman Jerome Powell sounded optimistic on Friday regarding Fed policy and mentioned a ‘soft landing’ and indicated interest rates at their current level will still need a bit of time to have their full effect. U.S growth numbers via the Gross Domestic Product came in stronger than expected on the 29th of November, but inflation data continues to show a slight erosion.

This puts the U.S Federal Reserve in position to actually sound rather neutral when the FOMC Meetings conclude in a week and a half. And if global events do not cause any sudden alarms to ring, it appears risk appetite is within a rather optimistic state. U.S equity indices continued to roll along merrily and the 3 big indexes are challenging highs. The S&P 500 and Nasdaq Composite are challenging July values, and the Dow Jones 30 is trading at ratios last seen in January of 2022.

While U.S Treasury yields have also continued to erode and are near mid-term lows, the USD/JPY continued to create a bearish trend for the week and is trading at values last seen in the second week of September. The GBP/USD finished the week within sight of highs attained on Tuesday and Wednesday, this as the currency pair also trades near values last seen in late August and early September. The EUR/USD is the outlier among the three major currency pairs and speculators may look at the EUR as potentially being in oversold territory as the week gets set to begin. Risk management as always is essential for wagering on Forex.

S&P 500 One Year Chart as of 3rd December 2023

The next two and a half weeks of trading will see full volumes, this before holiday trading starts to hit the broad marketplace. The upward moves in U.S equity indices may be seen as overdone by many analysts, but the trend has been strong and trying to step in front of the ‘optimism’ within the indexes may prove expensive in the coming days and weeks. Day traders should make sure conservative leverage is being used if they are attempting to climb aboard the moving train.

Some analysts are pointing out correctly, that if it weren’t for a few ‘workhorse’ corporations in the U.S equity indices, declines would have been seen. But day traders who are wagering on CFDs via their brokers and financial institutions investing in the three major stock indices are likely enjoying their profitable returns.

Monday, the 4th of December, E.U Sentix Investor Confidence – the reading is expected to come in with a negative result, but slightly better than last month’s outcome of minus -18.6. About a hour and a half before this European survey, German Trade Balance numbers will be released. The EUR/USD may be affected by this data, but the currency pair is likely moving within the shadows of behavioral sentiment which is USD centric. Europe is struggling with recessionary conditions, but it is outlook which drives the marketplace. If the EUR/USD can find durable support it may prove that its bullish trend has not come to an end.

Tuesday, the 5th of December, U.S ISM Services Purchasing Managers Index – an improvement is expected compared to last month’s outcome. Recent data from the manufacturing sector came in less than expected, thus the services sector will be watched closely, but as long as the result is around the expectation this will not hinder broad market sentiment. Meaning the report could be a non-factor.

Wednesday, the 6th of December, Canada BoC Overnight Rate – traders will be keen to see what line of rhetoric is taken within the Rate Statement from the Bank of Canada. No change to borrowing costs are expected. The rate is anticipated to remain at 5.00%. The economy of Canada has been struggling as recessionary clouds are shadowing, but recent GDP data was slightly better than expected and inflation has shown signs of weakening. The USD/CAD went into this weekend near its lows and in sight of values seen in late September.

Thursday, the 7th of December, China Trade Balance – economic numbers via the manufacturing sector last week came in below expectations. The lackluster China data may be a factor in the weaker WTI Crude Oil prices, but perhaps that is only speculative. Some investors participating in China are worried about outlook over the mid-term. Analysts will comment on the Trade Balance numbers, but traders should make sure they separate the ‘noise’ which may be delivered from biased perspectives depending on ‘world view’ compared to actual outcomes and genuine insights.

Friday, the 8th of December, U.S Non-Farm Employment Change and Average Hourly Earnings – the jobs numbers will be looked at attentively by market participants. The data will be correlated to existing behavioral sentiment and risk appetite that has sustained a weaker USD, higher U.S equity indices, lower yields on U.S Treasuries and the high price of gold. If the jobs data comes in around expectations that will likely be enough for investors to remain calm and look forward to the 13th of December, this is when the U.S Federal Reserve will release its FOMC Statement – which may keep risk appetite strong.

AMT Top Ten Miscellaneous Nibbles for the 1st of December

10. Book: Kissinger: 1923 – 1968: The Idealist by Neill Ferguson

9. Music: Clifford Brown and Max Roach Quintet playing Joy Spring.

8. Bitcoin: Curious stubborn trend higher as ETF fever appears to be creating bets on perceived ‘forced’ upwards momentum. BTC/USD now above 38,000.00.

7. Charlie Munger: Passed away earlier this week. Extremely well regarded as a man and helped create the Berskshire Hathaway colossus.

6. Crude Oil: Cash price of WTI Crude Oil remains stable and hovering above mid-term support after OPEC and associates announced voluntary production reductions yesterday.

5. Data: While U.S GDP numbers came in with solid growth statistics on Wednesday, yesterday’s U.S Core Personal Consumption Expenditures results came in below last month’s data showing inflation is eroding.

4. Gold: The precious metal remains above 2000.00 USD in a rather strong fashion, short-term speculation has been vigorous. Caution is advised for day traders.

3. Jerome Powell: The Federal Reserve Chairman will be speaking in Atlanta later today and his comments while participating in a ’roundtable’ discussion could affect behavioral sentiment going into the weekend.

2. USD: Outlooks via tier 1 financial institutions and larger players keeping the ‘greenback’ weaker and near mid-term support against other major currencies, price velocity should be watched.

1. U.S Indices: Dow Jones Industrials touching highs not seen since January 2022. S&P 500 and Nasdaq Composite within sight of July 2023 apex levels, and if penetrated upwards would also bring these indices to heights of late 2021 and early 2022, this as risk appetite demonstrates backbone.

You can find more AMT Top Ten Miscellaneous lists in the AngryMetaTraders archive

To Risk or Not to Risk that is the Speculative Question

Last week U.S equity indices demonstrated a rise in value. The highs achieved in the Dow Jones Industrial Average, the NASDAQ Composite and the S&P 500 by the end of last week only touched values seen in the middle of October. And while their ratios remain below the highs of early August and falling values seen in September, the move upwards was certainly welcome by financial institutions and day traders who hold optimistic viewpoints.

U.S Treasury yields declined last week. While incremental decreases were made through Thursday, the U.S Non-Farm Employment Change and Average Hourly Earnings reports both coming in below expectations on Friday, created a stronger dose of lower yields. The 5, 7, 10 and 30 year U.S Treasuries are now trading near mid-September values. The 2 and 3 year notes are moving around early September numbers.

Gold One Year Chart as of the 5th November 2023

The USD grew weaker in slight movements against many major currencies last week, but upon the weaker jobs numbers found increased selling price velocity. Gold however remains suspiciously strong, which brings up the notion that risk adverse ‘insurance’ is still being held closely by investors who remain nervous.

The Middle East crisis is ongoing in Israel against Hamas and to a limited extent Hezbullah, but financial institutions have seemingly been able to digest the news and remain tranquil and vigilant. Another sign of calm coming into the global financial markets is the price of WTI Crude Oil which finished the week under 81.00 USD per barrel.

Economic data will be relatively light this coming week, and behavioral sentiment appears to be the potential larger factor until Friday regarding impetus for day traders and financial houses. Certainly loud global developing news could suddenly erupt and cause nervous investors to falter, but last week’s trading results showed signs of improving risk appetite.

The U.S Federal Reserve met expectations last Wednesday and didn’t raise the cost of borrowing. The mid-term seems to indicate interest rates will remain high, but that the U.S central bank will not raise the Federal Funds Rate anytime soon. The lower than expected inflation report via the Average Hourly Earnings before going into the weekend helped highlight this thinking, although it remains a consideration that is still speculative.

Officials from the major central banks including the BoJ, BoE and Fed will be speaking this week and could cause turbulence with their rhetoric. However, no major surprises will likely come from their mouths. Although the Bank of Japan may rattle the prospects of intervention to keep USD/JPY traders on their toes.

Monday, the 6th of November, Germany Factory Orders – the result is expected to be negative and highlight the nation remains within recessionary conditions. The Sentix Investor Confidence reading will also be released slightly afterwards for the European Union and a worse number than last month’s outcome is anticipated. But the EUR/USD is likely to remain mostly USD centric, even though these reports could cause momentary fluctuations.

AUD/USD Six Month Chart as of the 5th November 2023

Tuesday, the 7th of November, Australia Cash Rate – the Reserve Bank of Australia is expected to raise its interest rate by 0.25% to 4.35%. Will the RBA take a gamble and not raise the interest rate due to other major central banks holding their rates in place, or will the increase go ahead to fight stubborn inflation while trying inspire some confidence in the AUD? A hike seems to be the direction the RBA will decide upon, having said that, the Australian central bank have surprised financial institutions before.

Wednesday, the 8th of November, U.S 10-year Bond Auction – the results from this sale and the yields that develop within U.S Treasuries will have an affect on Forex. Lower yields than anticipated could signal a weaker USD. However, risk adverse elements will need to be calm for the bond auction to produce tranquil results.

Thursday, the 9th of November, China CPI and PPI – the data from these inflation reports will be watched closely. Chinese economic numbers has shown some signs of stabilization the past few weeks, both of these publications are expected to have negative outcomes. Concerns about the financial pressures domestic consumers are facing regarding housing market values in China and the way in which they spend due to lackluster prospects are concerning. The USD/CNY will be affected in the wake of these statistics, and the USD/SGD could see momentary volatility too if the results prove to be a surprise.

GBP/USD One Month Chart as of the 5th of November 2023

Friday, the 10th of November, U.K Gross Domestic Product – last month’s number came in with an unexpected positive gain of 0.2%, this GDP report is anticipated to show no change. The GBP/USD jumped in value on Friday and financial institutions will be geared towards behavioral sentiment most of this week, but the British GDP data could cause a reaction before going into the weekend.

Friday, the 10th of November, U.S Preliminary Consumer Sentiment via the University of Michigan – the reading is expected to be slightly below last month’s outcome. U.S consumers remain a strong point of light for the U.S Federal Reserve. American consumers have remained spenders, although they have seemingly curtailed purchases of large ticket items such as cars and big appliances. If this data comes in weaker than expected it could propel more selling of the USD. A stronger number than anticipated could spook financial institutions and cause a slight surge in buying of the USD.