Nervous Results Next: Forex and Equities Wait for Jobs Data

Tomorrow’s jobs numbers from the U.S will get plenty of media coverage. Typically the Non-Farm Employment Change data is used as a selling tool by brokers to get their traders motivated and speculating on Forex and stocks via CFDs with the promise of swift price action. Many times the jobs numbers prove to have limited value, serving mostly as entertainment for back office risk managers at Forex houses as the whipsaw value changes wipe out speculators across the board. However, tomorrow may prove different.

Friday’s Non-Farm Employment Change and the Average Hourly Earnings statistics may produce dynamics worthy of their news coverage. Financial institutions are actually quite interested in tomorrow’s coming reports as the U.S Federal Reserve lingers in the shadows having spoken boldly about raising the Federal Funds Rate in November. It would take a weaker hiring result from the Non-Farm Employment Change data, and lower inflation numbers from the Average Hourly Earnings outcome to change financial institution outlooks regarding the U.S central bank.

EUR/USD One Month Chart as of 5th Oct. 2023

The trend of the EUR, GBP and JPY clearly demonstrate the value that has been lost against the USD over the past three months. While many financial institutions and speculators believe the USD will begin to lose strength eventually, timing the moment this is going to start happening in earnest is difficult. U.S Treasuries have come off of highs in recent trading, but nervousness remains abundant and recent heights remain in sight. Tomorrow’s U.S jobs number could reignite fear and spark behavioral sentiment which is reactionary.

As a side note, while U.S indices turned in some gains on Wednesday, the moves higher were not exactly momentous which sets up the U.S stock markets to produce a sudden reversal lower if widespread nervousness is produced today and tomorrow.

Importantly, hiring is believed to be weakening in the U.S by some analysts, but there is plenty of talk about a lack of qualified workers to fill important jobs still. So while the Non-Farm Employment Change number may come in below estimates and could spark hope among financial institutions the U.S Fed will be given a reason to sit on their hands, it is the Average Hourly Earnings inflation numbers which should be watched even more closely. If the costs of paying wages is more expensive than the previous month, this would spark concerns about price pressures remaining problematic.

Analysts have also continued to speak about concerns regarding revisions being made by the U.S government to past jobs reports, which means financial institutions are wary of positioning themselves fully based on the current month’s reporting. Accurate reporting from the U.S government has become problematic, and is causing nervous and conspiracy minded chatter in some trading corners.

WTI Crude Oil One Month Chart as of 5th Oct. 2023

Another factor which day traders may want to consider is the price of Crude Oil which has sunk below 84.00 USD per barrel in the footsteps of a one week decline. If the price of the commodity can remain muted and show a solid trend downwards this would help reduce hawkish rhetoric from the Federal Reserve.

As we go into tomorrow’s jobs numbers from the U.S, the broad markets do continue to exhibit nervousness which appears justified. The results of the Non-Farm Employment Change and Average Hourly Earnings may produce results which cause a reaction which shakes the outlooks of financial institutions and carries strong implications for day traders that matter.

Risks Ahead: Tranquil Data Mixed with Loud Nervous Chatter

Last Friday finished with stronger than expected Non-Farm Employment Change numbers, which essentially collided with dovish rhetoric via two U.S Federal Reserve FOMC members from the middle of the week; this while inflation clearly remains stubborn in the U.S.

All of which sets up this coming week for nervous trading results and until the 14th of June, when the Federal Reserve’s Federal Funds Rate pronouncements will be brought forth. Plenty of talk about interest rates will be heard in the days ahead and traders should expect to hear debates as the chatter grows louder.

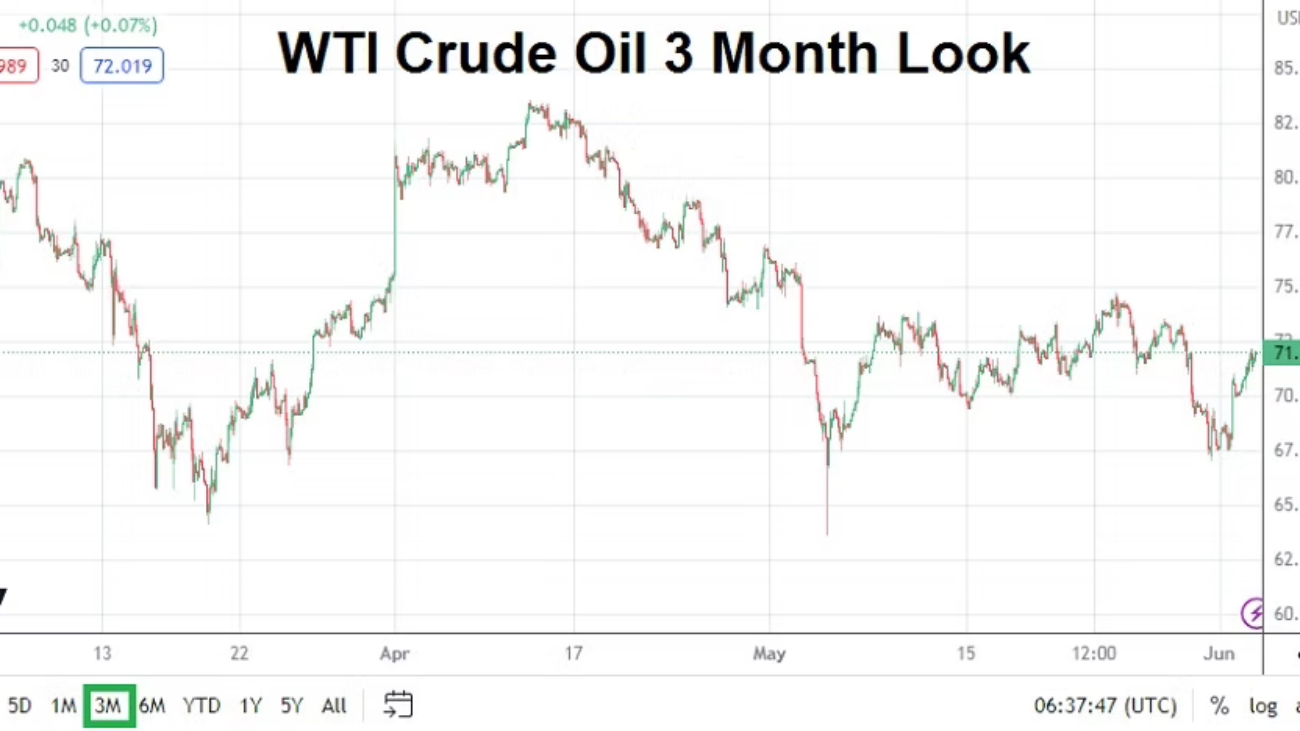

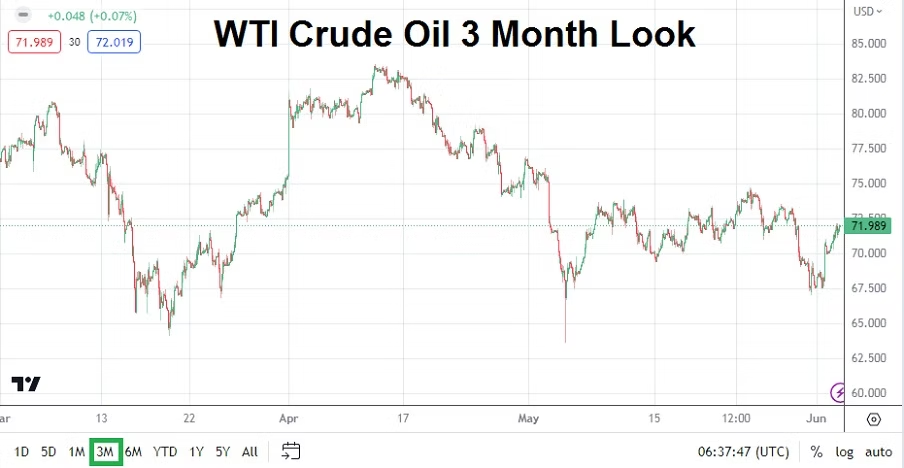

Commodity traders may be interested in the outcome of the OPEC+ meetings taking place this weekend. The cartel’s decisions regarding oil production will affect not only prices of Crude Oil futures, but is a direct reflection regarding global demand, which also tells us about the organization’s viewpoints regarding global economic conditions.

WTI Crude Oil Three Month Chart as of 4th of June 2023

Monday, the 5th of June, European Services PMI – Germany, France and Italy and will release their Purchasing Managers Index readings. The German outcome could prove interesting because the nation is suffering from recessionary pressures. The PMI results could affect the EUR/USD a bit. The U.K will also release their data too.

Monday, the 5th of June, U.S ISM Services PMI – this report will be of interest because some are expecting a better outcome compared to May’s results. A potentially strong reading could prove problematic and put more pressure on the Federal Reserve to raise interest rates next week.

Tuesday, the 6th of June, Australia RBA Rate Statement – the Reserve Bank of Australia surprised people with an increase of their Cash Rate last month. No increase is expected now, but the RBA’s rhetoric should be listened to as they comment about domestic and global economic conditions.

Wednesday, the 7th of June, Canada BoC Overnight Rate – Bank of Canada is expected to hold its borrowing costs in place, but inflation is still creeping into prices and the BoC’s Rate Statement may prove intriguing.

Thursday, the 8th of June, U.S Weekly Unemployment Claims – following in the footsteps of the stronger than expected jobs numbers last week, this report could get some media fanfare. However, it also may prove to be a lot of noise and have little real affect on market direction.

Friday, the 9th of June, China CPI and PPI – the inflation reports from China could prove interesting in wake of recent lackluster economic data from the nation. Last Thursday’s Caixin Manufacturing PMI results came in slightly better than expected, but data from China the week before was negative. The data from China gives investors and traders insights because of its importance as a global supplier of consumer products.

Monday 15th of May, U.S Empire State Manufacturing – N.Y manufacturing sector report regarding business conditions, which serves as a sentiment reading. A lackluster outcome could put a bit more pressure on the Federal Reserve to lessen their aggressive stance, and certainly point out nervousness among U.S corporations regarding profits.

Monday 15th of May, U.S TIC Long-Term Purchases – report shows results from between domestic and international purchases of U.S Treasuries. While not considered a major data release, this one could give an impetus to investors in U.S banking sector who may find intriguing potential correlations. An increase in the number of domestic purchases compared to international buyers would be of interest. Large dark shadows on the U.S mid and small size banking sector still exists, pressures boil as depositors are still considering parking their money elsewhere, and corporate share values remain fragile.

Tuesday 16th of May, China Industrial Production and Retail Sales – China economic results are a barometer of global health due to the fact the nation is a large supplier of worldwide products. Industrial Production results if they are lagging in China, would indicate decreasing demand and global economic weakness. Retail Sales figures from China is an indicator of consumer sentiment within the nation.

Tuesday 16th of May, U.S Retail Sales – results indicate buying power and confidence among U.S consumers. Underlying numbers also focus on how Americans are spending, in other words – are they paying the full price being asked or are they looking for discounted goods as inflation continues to hit wallets.

Wednesday 17th of May, Japan Preliminary Gross Domestic Product – No real surprises expected from Japan’s growth numbers, but the results are always appealing to economists who debate the nation’s ability to remain among the wealthiest without any truly outstanding GDP numbers produced in years. In other words a lot of noise for traders without much real impact.

WTI Crude Oil – One Month Chart as of 14th May 2023

Wednesday 17th of May, U.S Crude Oil Inventories – another report that seems important for commodities traders, but without any real surprises has limited impact. Many times even among WTI Crude Oil speculators, they are often looking at other data they have gathered like production numbers from OPEC, Mexico and Canada. And also oil tanker movements around the globe.

Thursday 18th of May, Australia Employment Change and Unemployment Rate – outcome from these numbers could factor into AUD/USD momentarily, but without a major surprise will likely have little impact on global speculators for more than a couple of hours.

Thursday 18th of May, U.S Existing Home Sales – housing numbers are under some scrutiny as they reflect behavior of current U.S home owners as they react to growing interest rate pressures on mortgages and stay within their current homes to avoid higher borrowing costs.