In a World Filled with Bread and Circuses, Now a Dose of Transparency

10: The Risk Reward Show: Sommer and Petrucci will return to the airwaves this coming week, via sources like Spotify and YouTube, with their podcast starting after a long break (absence).

9. Hardball: Major League Baseball is back and the sport continues to attract more fans and growing attention with its quicker games, a new computerized strike zone, and maybe even more dislike of the Los Angeles Dodgers. Yes, Shohei Ohtani remains a dominant and positive force in the baseball world.

AMT Top 10 for the 19th of April 2026

8. Populism: Politicians on both sides of the Atlantic continue to display a wide display of nonsensical rhetoric and bold asinine actions equating into empty spectacles. An example from the Left is Zohran Mamdani the mayor of New York City with his socialist platform, which is certain to fail and equate into more people and companies leaving NYC for less expensive and friendlier tax environments. And from the Right Italian Prime Minister Giorgia Meloni who talks a tough game but consistently falls short of backing up her words when she senses she could lose control of her power base. The putrid smell of trying to please voters with rotting bread and circuses prevails.

7. Speculation: Gold finished Friday’s trading near $4,837.50, Silver around 80.78. Bitcoin is close to $75,570.00.

6. AI: While the Artificial Intelligence hangover has been widely discussed for a handful of months, health continues to be seen via Nvidia which closed above $201.00 going into this weekend, and Anthropic PBC which appears to be aiming for an IPO in late 2026 or early 2027. At this moment Anthropic has an estimated valuation of 800+ billion USD. If Nasdaq is able to secure a listing with Anthropic it will immediately factor into the Nasdaq 100. Are some investors betting on upside now which they believe will be seen when Nasdaq reorganizes its index?

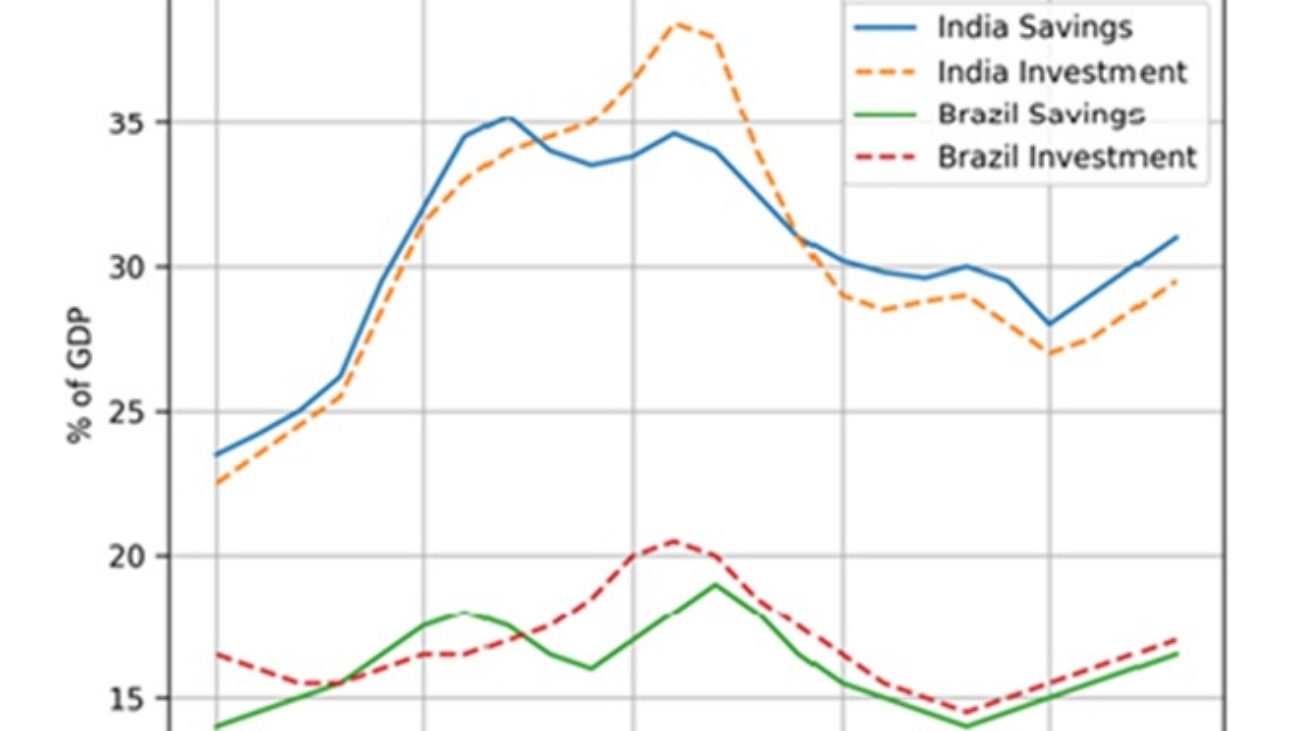

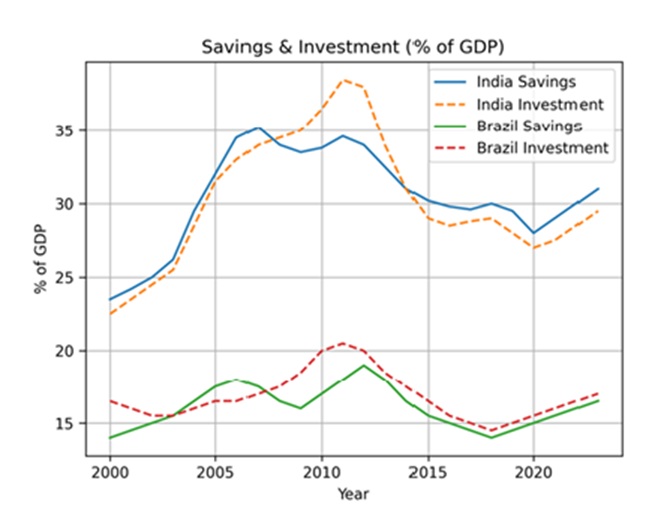

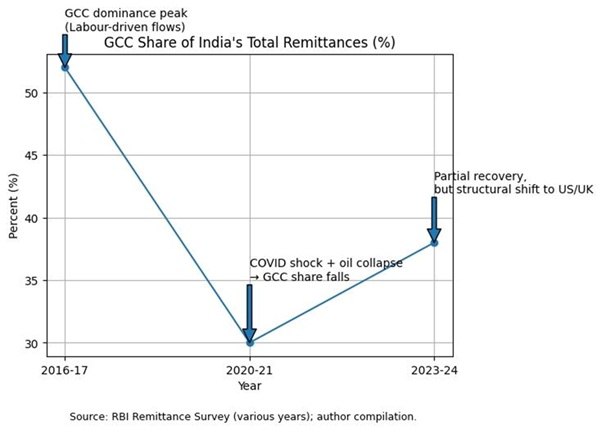

5. Optimism: India, South Africa, Brazil and other emerging markets have experienced Forex volatility like all nations the past month and half due to the Iranian war. However, in the past two weeks the Indian Rupee, South African Rand and Brazilian Real have performed better as global markets have calmed. The ZAR and BRL have actually outperformed major currencies over the past handful of months showcasing existing optimism within financial institutions dealing with these currencies.

4. Money for Something: Lefarge, a French company specializing in concrete, was found guilty this past week of paying ISIS (Daesh) and other terrorists groups money in the years from 2012 into 2014, this in order to maintain their business operations in Syria. While Lafarge claims they paid the money to keep their operating staff safe, a French court ruled Lafarge was buying not only safe passage to allow employees to work, but also paying for physical resources needed from quarries that were controlled by the terrorists. Critics of Lafarge point towards the company’s massive infrastructure investments leading up to 2012 and a decision to seek profits no matter the costs of dubious morality. Some Lafarge former senior executives involved have been sentenced to prison including Bruno Lafont and Christian Herrault. Lafarge and Holcim (a Swiss conglomerate) merged officially in July of 2015.

3. WTI Prices: The value of the world’s most famous Crude Oil went into the weekend near $83.30 via futures markets. The commodity is certain to open with volatility early on Monday, this as folks weigh in via their existing behavioral sentiment which will range from speculative perceptions to insights they hold to be true (but that could prove false). WTI Crude Oil challenged 79.00 USD momentarily on Friday, before sparking upwards as cautious attitudes likely ignited doubts about what would happen this weekend in the Middle East regarding potential developments. Wagering on WTI in the coming days for day traders may be akin to spins of the roulette wheel.

2. Apex Heights: The winning streak and surge upwards for the Nasdaq 100, S&P 500 and Dow 30 via gains have caught some investors by surprise and standing on the sidelines. Some large financial institutions may find they have to explain why they did not participate in the rally which has unfolded since late March. The S&P 500 has gone up around 9.5% during this time.

1. Straight Talk: The Hormuz and whether or not the strait is open for oil tankers will remain a catalyst for all global assets until clarity is gained. In the meantime a whirlwind of noise and threats from President Trump, the U.S White House and Iran will remain a menace for all traders – small and large. Is the Strait of Hormuz open or closed?