Wednesday Federal Reserve Prediction and Central Bank Unity

Later today the Federal Reserve will release its Federal Funds Rate and FOMC Statement. Jerome Powell will also field questions. My prediction regarding the Fed today is that the Federal Reserve will hold (pause). It will say inflation remains problematic and stubborn, and the Fed continues to monitor economic conditions it finds complex. The high costs of energy (Crude Oil) will be presented as part of the problem.

The Fed will say they will strongly consider an interest rate hike next month, thus bracing the markets for what financial institutions have already traded into the system. This because trading houses have listened to the Fed already and believed that a pause would be seen for a few months, but cracks in sentiment quickly appeared in mid-July because of the Fed’s cloudy rhetoric as it spoke out of both sides of its mouth. Ratings downgrades and worries began, the USD sprung to significant values, higher U.S Treasury yields have flourished and increased fears for the long-term investment world. All the noise has certainly helped doomsayers.

The problem for the Fed and they should be aware of this, is that their interest rate hike threats have little direct affect on the price of Crude Oil. The rise in oil prices is directly due to Saudi Arabia cutting back on production. The U.S has much less influence on Saudi Arabia then it would like to believe it does. The Saudi Arabia government is interested in sustaining a profitable price for the commodity. At 90.00 USD per barrel, Saudi Arabia is making significant profit, but under 80.00 USD per barrel they grow concerned. After all someone has to pay for the ‘Line’ project of Neom.

Getting back on point, if the Fed is so intent on raising rates they should do so now. Not next month. But as the Federal Reserve and other major central banks often demonstrate, they are reactive – not proactive. Meaning if the Fed has no direct influence on the high price of energy that they should go ahead now and influence the marketplace instead of rattling a sword which only creates nervous global behavioral sentiment.

And yes, a hike of the Federal Funds Rate would be problematic for credit and cash reserves of consumers and businesses, which face more expensive obligations regarding loans and bonds. However, if you are merely going to threaten to do something, why not do it now and say without a doubt – like the ECB did last week – this will be our last hike for the foreseeable future. But the Fed is likely to prove they have limited desire to act swiftly and try to remain painfully polite, very much like when they refused to acknowledge inflation was a real threat when it started in earnest over two years ago.

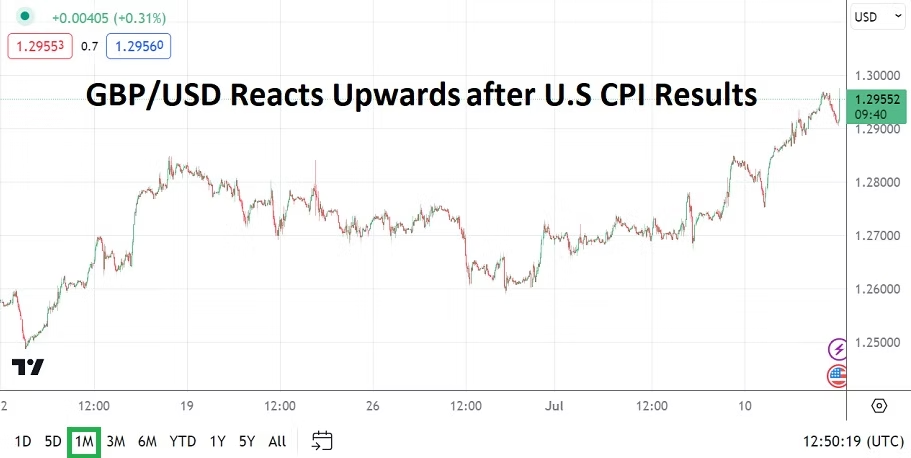

Lastly, the Bank of England will make their pronouncements tomorrow, and some are suggesting the BoE because of today’s ‘weaker’ inflation results will not raise the Official Bank Rate. However, I disagree, inflation is still high in the U.K and the Bank of England may also feel it has to protect GBP value.

Last week’s interest rate hike from the European Central Bank, which I didn’t believe would happen and was wrong about, suggests the BoE and ECB may have privy knowledge regarding the Fed’s inner thinking. It is quite possible the European’s raised rates last week not only to fight inflation, but because they had been warned by the Federal Reserve that the U.S central bank wants to ‘sound’ aggressive. There is reason to believe if the Fed doesn’t raise tonight, but groans on about a complex economy and stubborn inflation and the need to consider raising rates next month, the BoE will feel very compelled to still hike the Official Bank Rate by a quarter of a point tomorrow.

Nothing quite like coordinated banter between the major central banks which have already demonstrated a rather stark level of mistakes over the past two years. Why not add onto the shenanigans today and tomorrow? Good luck to us all.