Energy and Commodities in a World Where Legacy and Infrastructure Collide

Google (Alphabet) finished yesterday’s trading near $ 317.69, as of this moment WTI Crude Oil is around $88.50. It might seem rather odd to pair the two into the same paragraph, but this is not a coincidence. Both are now relevant regarding energy costs for consumers and produce an abundance of legacy products the world over. And oddly enough their one year charts almost look as if they are dancing in step.

Google is facing headwinds in recent trading as questions surround its capability to produce revenues because of its push into Artificial Intelligence and always growing need for more data center power. AI which has been an abundant source of bullishness in the Nasdaq 100 and had a knock-on effect into the S&P 500 the past couple of years has become shadowed by concerns of turning into a commodity.

Alphabet (Google) One Year Chart as of 24 July 2026

As competition in the AI sector increases this is creating pressure on prices in order to allure customers away from competing brands. China is also stepping into the world of Artificial Intelligence and it will certainly use its ability to produce less expensive products moving forward. Profit margins are being fought over by competing companies

Google is not a poor company, but there are growing doubts about its debt and revenue ratios. The costs to power its worldwide data ability for its users and its investment into AI via Gemini and its DeepMind technology does not have a particularly easy solution. Estimates from a variety of sources claim that Google has reduced its staff between 1,500 to 3,000 through employee reductions and reorganization, this as the company needs to pile more cash into infrastructure.

The onslaught of other companies able to produce AI which is seen as more robust and capable have also caused a marketing headache for Google, which has an effect on behavioral sentiment. GOOGL was trading at apex levels only two months ago when it was traversing above the $400.00 mark. The downturn thus far has been bad, but not catastrophic.

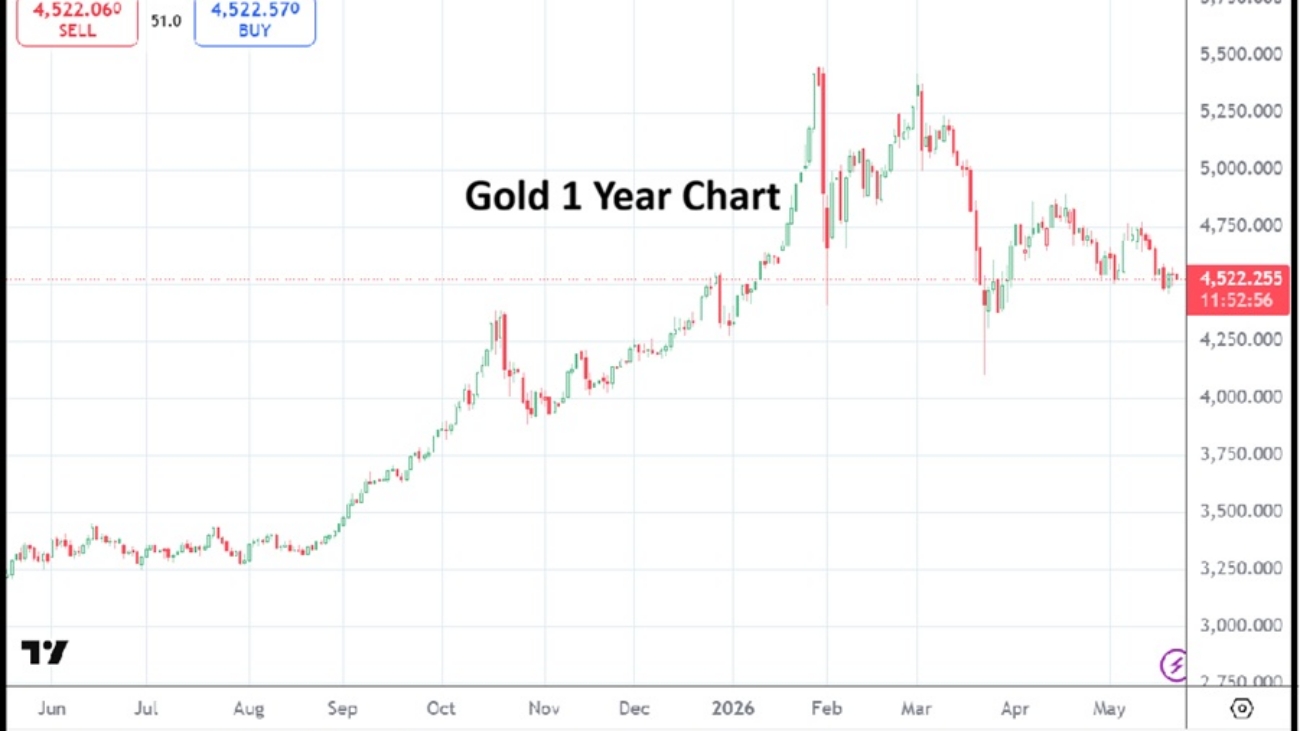

WTI Crude Oil One Year Chart as of 24 July 2026

While nervous sentiment can be blamed on the situation in the Middle East the past handful of months, the downturn which has occurred for Google and other important companies on the Nasdaq 100 involved or seen as having an ancillary association with AI needs to be considered a legitimate reaction because of worries surfacing regarding the ability to simply pay for all of the research and infrastructure.

In order to power AI it is becoming clear that energy costs are part of investing frameworks. Concerns about an AI bubble started to gather an audience last fall and the rumblings have grown louder, yet it can be said the ability of Google and many other companies to gain the past year in value still outweighs this current downturn experienced the past couple of months.

The Iranian war which is ongoing, appears to be entering a phase in which financial institutions are having to succumb to the notion of higher prices not only for WTI Crude Oil but other energy resources with a mid-term viewpoint. While there is abundant supply of Crude Oil worldwide, the current problems surrounding navigation and logistics are causing pandemonium in a consistent manner via WTI’s price as Middle East nations try to ship to their clients. This is causing many Asian nations to look elsewhere for their energy, Brazil has seen an increase in orders. And because of the upwards trend in fuel costs again, the Federal Reserve will have to look hard at inflation data and play a game of interest rate mania, which investors will have to calculate into their outlooks regarding debt ratios.

What does this have to do with Google and AI?

People like nations will search for the easiest and most cost efficient pathway to access their needs. Anthropic, OpenAI, Kimi K3, Microsoft Copilot, DeepBlue Technology, Meta, Sakana AI, IBM, Nvidia are only some of the companies involved in sourcing software and providing hardware to users. Many nations are involved in this AI chase and understand the importance of cybersecurity, data sharing and the problems surrounding the costs to power all of these machines.

Many of these companies above including Google are searching for a holy grail via energy supply and discussing the financing and building of energy infrastructure including nuclear capabilities. But as Google and other companies search for more energy to fuel their dependence on powering their systems for clients, they continue to be confronted by a growing wave which will eventually drown some of the companies in debt that they will not be able to recover from.

I am not forecasting an apocalypse, but I am suggesting not all of these companies which we think of as part of our everyday lives will survive this fight. Legacy companies eventually parish, just like many start ups. The realization that many companies are merely providing what the public is starting to see as necessity is a simple competitive evolution. BlackBerry, Nokia and Motorola are examples of giants falling.

It appears many investors are starting to ask hard questions about costs compared to future earnings in AI. The allure of the next big thing, which AI has been part of the past couple of years, is running into well-practiced investment cycle as froth erodes and financial institutions start to look at the accounting of the companies they are being asked to consider as long-term endeavors. Not all that glitters is gold will certainly start to create a patina on many of the so-called AI companies as they are forced to prove their worth as suppliers of a commodity.

The AI world has run into the time honored financial realization that many exotic tastes soon turn into another form of vanilla. The next big thing is always being anticipated and hoping to attract the deep pockets of investors. Certainly many of the big companies including Google are going to survive the current headwinds. but real profits could become harder to attain. Investors and speculators should not be surprised that reality has a tendency to reduce momentum. Entropy is part of the investment world, investors and speculators always have to be ready for new disruptions and systems to emerge.