U.S Growth (Lack of it) and Inflation Report Key to End of Week

Day traders may believe they are being confronted by another wave of data and news which is going to make their endeavors more difficult. The announcement by Joe Biden that he will not run for re-election in November however was not a major surprise. The handwriting on the proverbial wall has been clear for nearly a month that Biden was under immense pressure to step aside. It appears Kamala Harris will get the Democratic nomination per reports that delegates are starting to pledge their loyalty.

Financial markets which may have been interpreted yesterday as cautious due to the Biden and Harris news may actually not have had a tremendous effect. It is quite possible investors and traders have started to position their assets for a Trump victory. Love him or hate him, the polling numbers appear to suggest the Republicans are potentially going to win big in November. Except the word November is the key, there are still over 100 days for things to go wrong for the Republicans. Nothing is settled and day traders need to understand that a lot can change. Economic data from the U.S will be plentiful in the coming days. Also, China has lowered key borrowing costs in an effort to try and fuel spending in the nation as consumers remain hesitant and a sign the nation is battling a troubling economy.

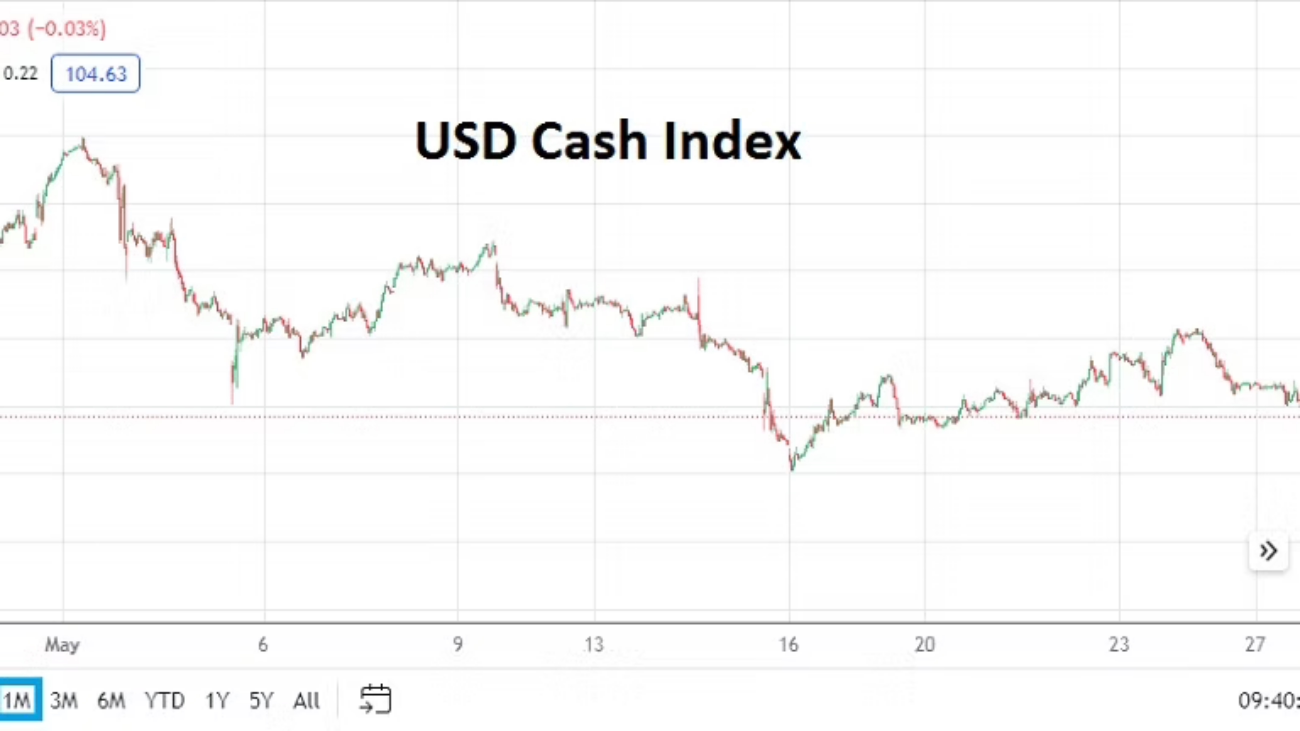

Traders who have been trying their hand in Forex have seen the EUR/USD and GBP/USD sink in value via short-term price changes. While retail speculators may look at the moves over the past day as vicious, they should note that since Wednesday of last week the USD has been stronger in Forex. It is doubtful financial institutions were betting on Biden to drop out of the race last week or for China to lower their interest rates. What in fact might be playing out is the possibility that most financial institutions believe the USD had been oversold and now want to position for the economic statistics coming this week. Results this week will help motivate notions the Federal Reserve will have to become dovish in September and proclaim a weaker U.S economic outlook through the end of this year, or for more idle chatter as the Fed undertakes a soundtrack which pleads for caution if inflation numbers remain stubborn.

Monday, 22nd July, China One and Five Year Loan Prime Rates – borrowing costs were cut officially yesterday. The interest rate reductions of 0.10% were small, but China hopes this change helps propel stimulus for its struggling economy. It may not. But before folks sell China short, the nation continues to be a dynamic economic and political force and this power is not going to abate soon. The USD/CNY has incrementally risen since the start of 2024, but it is still below the higher values seen from August into early November of last year. It seems possible the Chinese government will continue to allow the Yuan to lose value in an attempt to reignite export.

Tuesday, 23rd July, U.S Existing Home Sales – the past few months have seen a decrease in the housing data. However, last month’s outcome was stronger than anticipated. These numbers tend to get a lot of fanfare, because they are a solid barometer of U.S outlook regarding interest rates and potential inflation. If folks feel like they should not sell their homes because their current payments are cheaper via their existing mortgages compared to taking on higher costs which are being offered now due to more expensive interest rates, this causes existing home sales to often fall. This because those with homes are not looking to move and simply want to stay in place, also making the potential of finding a house for folks who want to enter the market a more expensive proposition. Again, the outcome of this data is more of a barometer and doesn’t tend to affect financial markets like equities or Forex too much.

Wednesday, 24th July, Europe Manufacturing and Services PMI – E.U nations and the U.K will publish their readings. Last week the ECB kept their key lending rate in place. Political questions still linger in France which is more of a thorn in the side of the E.U than the potential outcome of these data reports. France and Germany expect better results from the Manufacturing and Services numbers. The broad E.U estimate also is optimistic about better results. Great Britain too is expecting better numbers. However, Forex traders will likely be more focused on coming U.S data and stay in a USD centric mindset the remainder of the week when making their forward considerations. And it should be noted the E.U and U.K economies are still struggling.

Wednesday, 24th July, U.S Manufacturing and Services PMI – these reports will be important certainly regarding the sentiment of Purchasing Managers, but the index reading may not be the biggest thing on investors minds. U.S data statistics on Thursday and Friday will be the outcomes that are being prepared for regarding potential affects. The Manufacturing number is expected to match the previous result, the Services figure is anticipated to be weaker.

Thursday, 25th July, U.S Advance GDP and Advance GDP Price Index – last month’s growth number came in below expectations, this GDP number is anticipated to produce slightly better numbers. The U.S economy via data has been showing signs of slowing the past few months and this Gross Domestic Product number is going to get a lot of airplay not only because of investors who will use it as an outlook because they believe the Fed will be paying attention, but also because the GDP result will start to become a political football for the Republicans and Democrats. If the growth numbers are weaker than anticipated this could propel USD centric weakness. However, day traders need to keep their eyes on the GDP Price Index stats too – if the inflation report comes in below expectations this could also fuel USD selling. Day traders need to pay attention to the USD Index charts later this week. While the short-term has seen some bullishness, the range of the USD remains near important support levels via a six month perspective and as the Fed comes under more scrutiny, traders should expect more tests in the near-term.

Friday, 26th July, U.S Core PCE Price Index – last month’s report matched expectations. If this inflation number meets the anticipated outcome, or comes in below the estimate this could sustain USD centric bearish momentum into the weekend and early next week.