AMT Top Ten Miscellaneous Concerns for the 6th of October

10. Ya Gotta Believe: The New York Mets are finding ways to score in the late innings. Having won with last minute runs against the Atlanta Braves in the 8th and 9th innings early last week to save their season, hitting a home run to take the lead against the Brewers in the deciding game of the Wild Card in the 9th, and last night’s 5 runs in the 8th to take the lead in Game One against the Phillies in the Division Series has been rather remarkable. Game two between the Mets and Philadelphia will be played later today.

9. Information Technology: OpenAI’s value is now estimated around 157 billion USD, this after their latest round of investments garnered that includes both Nvidia and Microsoft funding. The search engine arms race will continue to get tougher and more competitive, but recent data released by Statcounter shows that Google still has over 90% of the U.S search engine traffic. While it has lost some ground in the search engine battles to upstarts statistically, Google remains dominant. Microsoft has made inroads with Bing, and Yahoo has also gained, but Google’s stranglehold via browser usage remains strong.

8. Helene Meets Milton: A pair of hurricanes – this if Milton fulfills forecasts and becomes a major storm – are not helping create easy days in the U.S Southeast, nor for the Biden administration. Criticism regarding a lack of government help has been heard in the aftermath of Helene and with another potential punch about to be delivered by Milton, U.S relief agencies like FEMA will certainly be pushed to the limit organizationally.

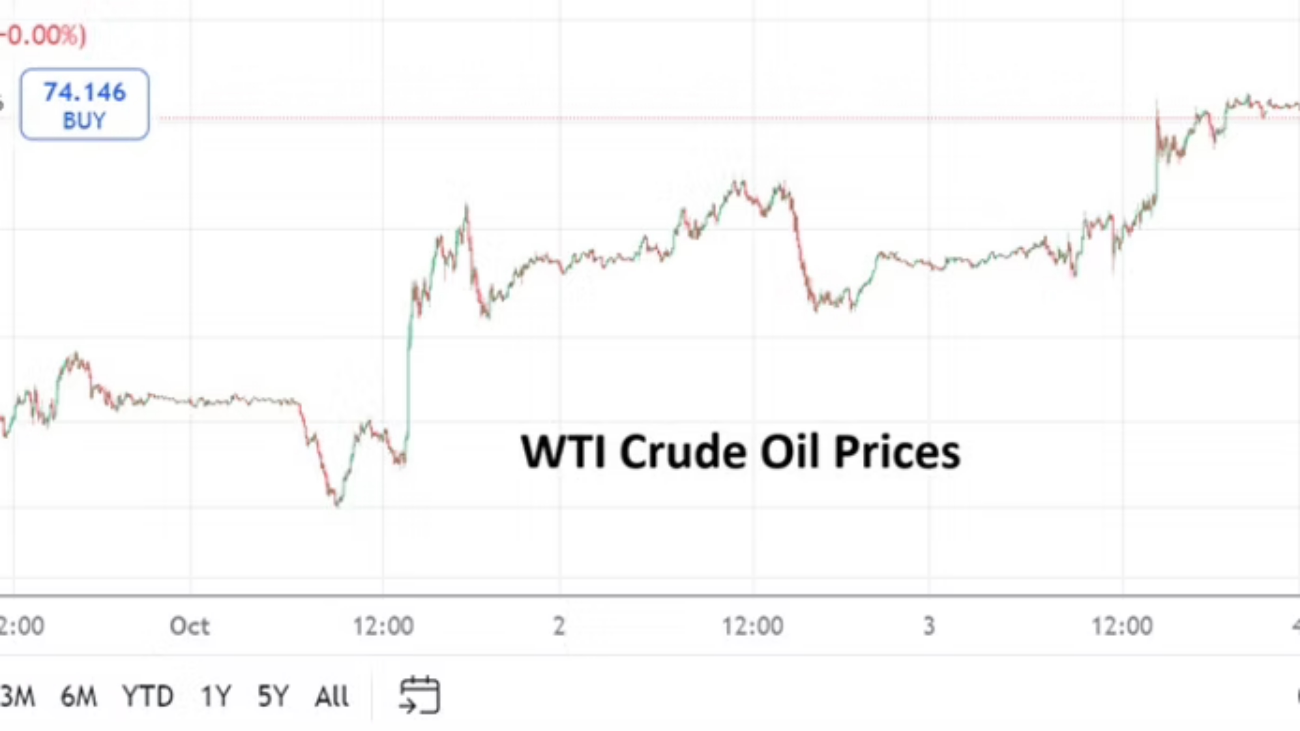

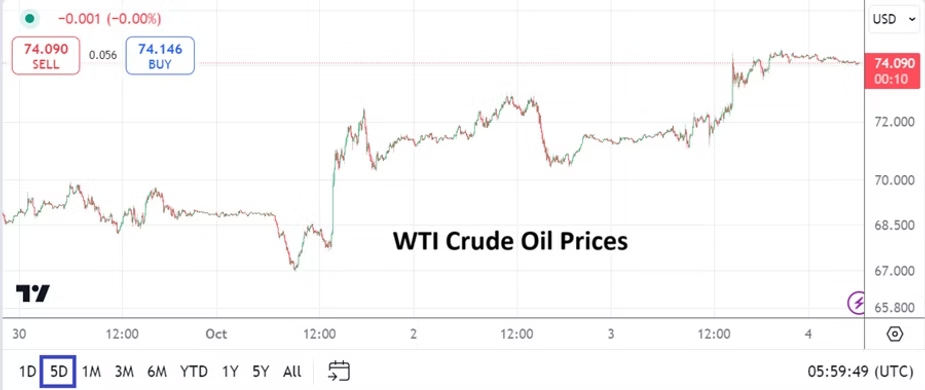

7. Oil Alerts: WTI Crude Oil went into the weekend close to 75.00 USD per barrel as nervousness increased about the potential of an attack on Iranian oil infrastructure. While many nations in the West do not purchase Iranian Crude Oil openly, the Iranian commodity is sold to China at nearly an 89% ratio. This allows oil from other suppliers like Saudi Arabia, the U.S and Mexico to sell elsewhere and the price of Crude Oil to remain relatively tame. However, if the supply of Iranian Crude Oil were suddenly to be crippled for any length of time, the price of the commodity from the other major suppliers would certainly go higher if expanded demand needs to be met. Speculators should pay attention to strike prices in the energy sectors via options trading in the future markets to understand potential vulnerabilities that large players may be anticipating.

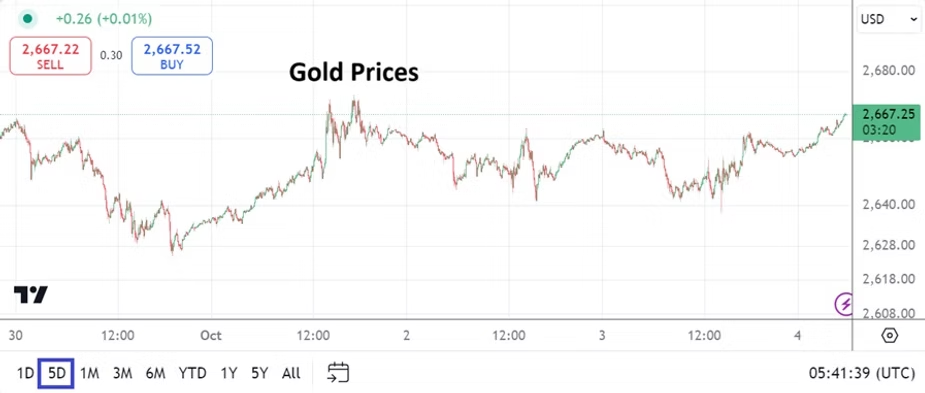

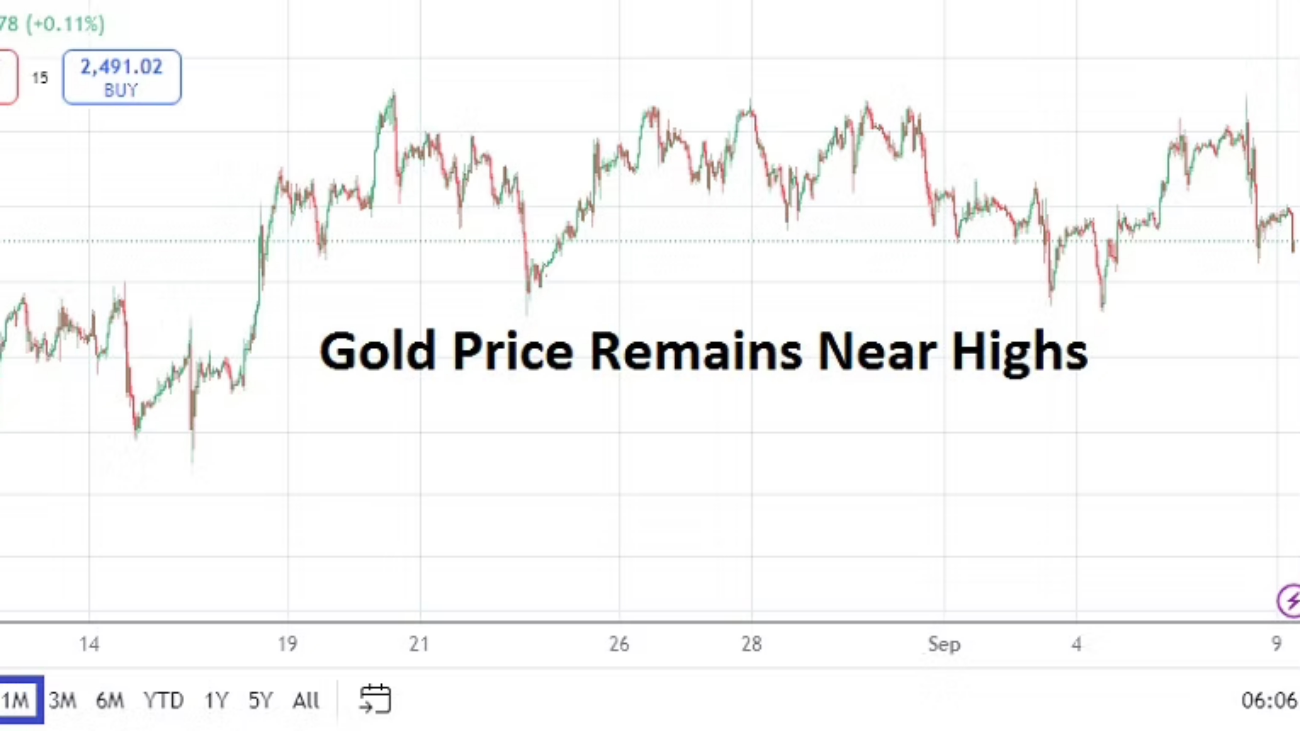

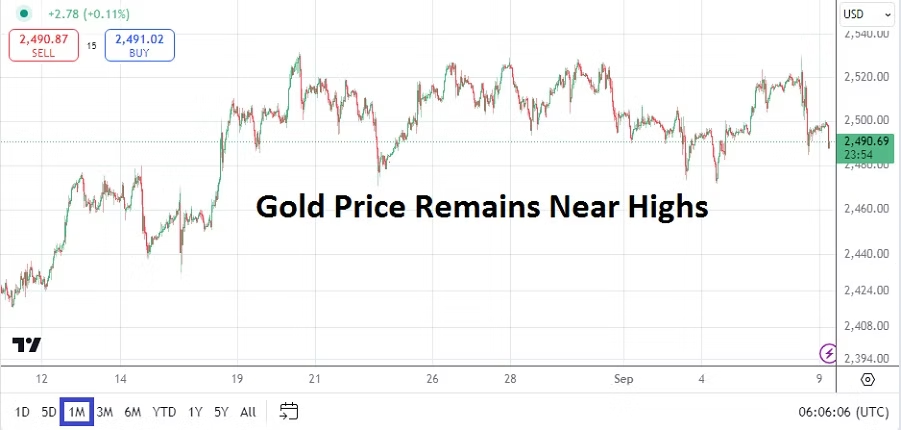

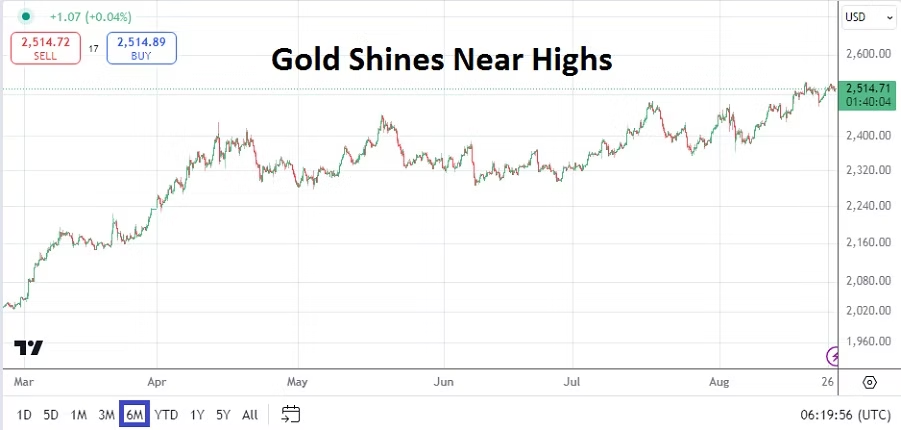

6. Precious Metal: Gold prices remain within sight of record values, but below the apex values seen on the 26th of September. Risk sentiment, speculative forces and long-term investors are seemingly creating resilient support levels. Gold went into this weekend near the 2,653.00 USD ratio. Silver remains near 32.00 USD per ounce, which is where its price was traversing in May. Speculators intent on betting that silver will rise because nervous market conditions will create more demand need to be careful. A vast supply of silver exists in known mines globally, and producers simply need to extract more of the commodity to garner profits which is relatively easy. In other words, gold and silver do not correlate as much as some people believe.

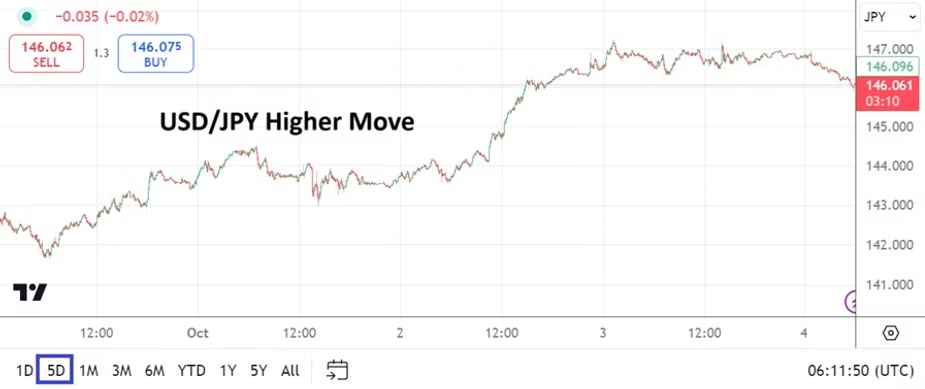

5. Forex Chaos: Day traders of USDJPY, NZDUSD, EURUSD and a slew of other major currency pairs were taken on a wild ride last week as USD centric strength surged and fragile conditions in global markets grew. The coming days will remain difficult for FX retail traders as they face a whirlwind of threats. Technical and fundamental traders are being hit by shifting winds generating via a myriad of worries. Speculators without deep pockets are advised to remain cautious in the coming days because trading dynamics are not likely to ease. Yes, there will be price velocity which allows for quick profits, but those who are willing to bet on the prospects of fantastic gains must also accept the dangerous proposition that wildly expensive losses if they are on the wrong side of a trade are equally possible. Brokers will certainly welcome their clients with open arms this coming week because the volatility may entice many with the potential of getting rich. However, brokers will not tell you about the poor house on the other side of the street.

4. Unscripted: There are a little more than four weeks before the 2024 U.S elections on the 5th of November. Trump appears to be gaining momentum in polls, but certainly remains vulnerable per his ability to speak without a script and create verbal firestorms. Kamala Harris ran into problems recently with a suspected malfunctioning teleprompter and her inability to escape repeating the words ’32 days’. While the two candidates battle for voter supremacy, questions persists about the current leadership from the White House and who exactly is running the show.

3. Noisy Data: The Federal Reserve and economic data remain concerns. This Thursday the Consumer Price Index data will be released. If the inflation statistics can come in below expectations this may soothe financial institutions who have leaned into the notion the Fed needs to remain aggressive in November. Another interest rate has been expected, but some are nervous the Fed may not be able to cut as fully as wished. However, day traders need to also understand politics are playing a role in the bombastic soundbites being generated by the media, this as they try to deliver messaging which reflect their viewpoints. If inflation numbers remain under control the mid-term outlook continues to point towards more interest rate cuts. While the U.S jobs numbers on Friday were better than expected it should be noted revisions downward were seen again. There is one more Non-Farm Employment Change report before the election, by then it will probably not have an impact on potential voters, but its affect on the Fed will certainly be felt.

2. End Game: As the Iranian and Israel conflict escalates and threatens to become a dark spiral, some are still hoping for an avenue which will allow normality to return. That appears to be wishful thinking for the moment. Reports, perhaps paranoid, regarding an earthquake in Iran yesterday with a magnitude 4.5 seismic rating which was 48 kilometers from Semnan was noted by the USGS. The reason why it is potentially scary notion is because some are questioning if this was a nuclear test being conducted by Iran.

1. Risk Adverse: A trifecta of nervous behavioral sentiment is shadowing the financial markets via Fed outlook, Middle East tensions, and the approaching U.S election. Unfortunately none of these components are likely to disappear soon and in fact may grow in stature as outlooks potentially create more anxiousness. Safe havens in the USD, gold and U.S Treasuries may find they deliver some calm for those that are nervous. However, it must be noted that U.S equity indices gained nicely late last week after gains on Friday. The Dow 30 and S&P 500 remain near apexes and the Nasdaq Composite is within sight of highs. In other words, for all the talk about dark days, financial markets and investors are still active.