Narrative Storms, Complaints and Observations

10. Mo’ Money: The Los Angeles Dodgers surprised nobody when they acquired Detroit Tiger’s pitcher Tarik Skubol in an effort to solidify their chances of a World Series three-peat. Don’t blame the LA Dodgers for playing by the rules, even if many don’t like the results. Expect a MLB strike in the coming year when owners try to change the salary structure in baseball.

9. Staggered: SpaceX is below $110.00 as trading gets set to begin today. Financial institutions are likely bracing for the open window that begins the 6th of August via a large amount of unblocked initial equity from pre-IPO shareholding that will soon be given freedom to sell.

AMT Top 10 Miscellaneous Interjections on the 3rd of August 2026

8. Fidel Castro: Mayor Mamdani and a gang of other U.S utopian (and sometimes bigoted) politicians continue to make headway. Authoritarian failures like Venezuela and Cuba are prime examples of the paradise offered to U.S voters who lean left for the coming mid-term elections.

7. Takeover: Citadel’s takeover of Situational Awareness – which seems to have proven it had none – this past week in the wake of multi-billion dollars of losses has put Leopold Aschenbrenner’s smirk on hold for the moment. Have no fear fans, Aschenbrenner is likely to land on his feet and extol his methods once again to those who love leveraged speculative ventures while embracing unproven hedge fund saints.

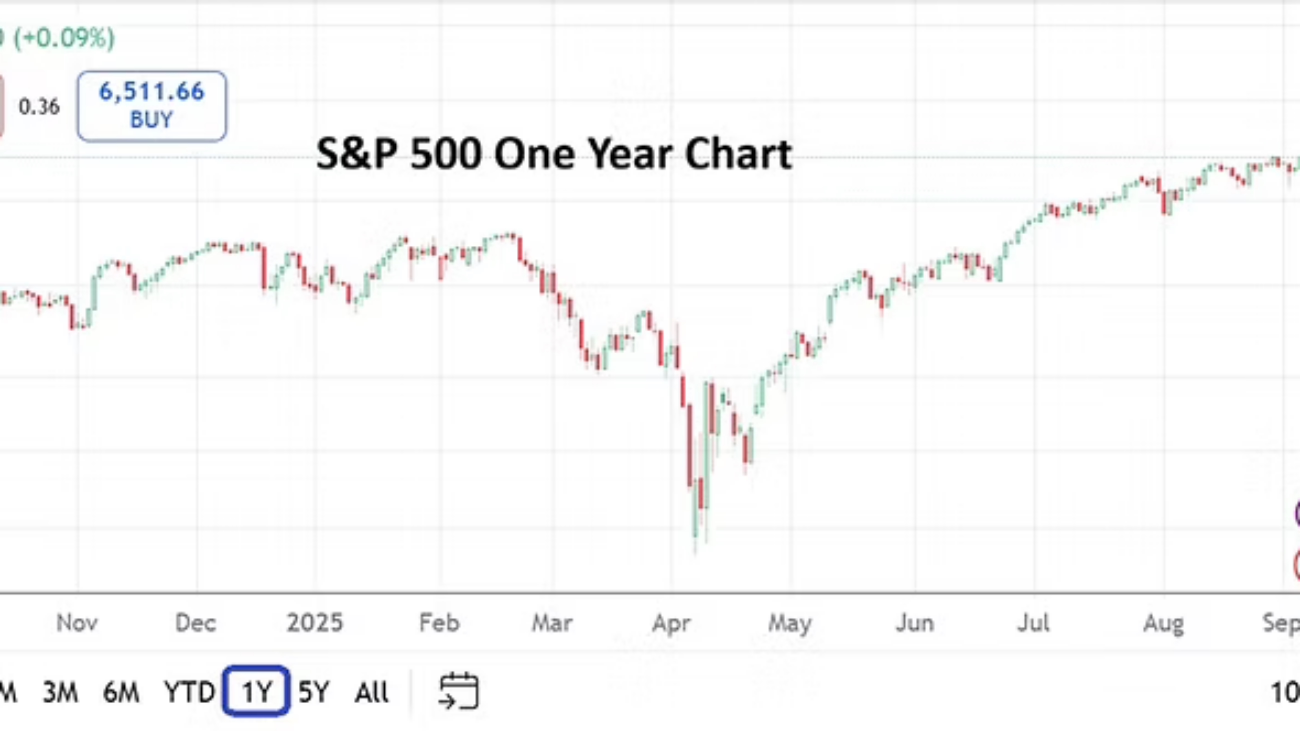

6. Fragile: The VIX Index appears asleep as it remains a hair under 16 as it measures the volatility of the S&P 500 Index’s options. 10-Year U.S Treasury yields are around 4.68% and within sight of apex highs. The Nasdaq 100 futures are higher as of this writing as the cash market and a full week of trading awaits, having finished Friday’s session at 28,274.

5. Anthony Fauci: Takes the Fifth and now hopes his pardon covers contempt.

4. Bitcoin: BTC/USD is near $62,850 in the wake of confirmed cold storage hacks via a generated random prediction onslaught using AI against Coldcard hardware. In other bad news Strategy’s MSTR value is around $93.35. And, yes, Michael Saylor has reportedly whispered he is thinking about buying more BTC soon. The ship appears to be sinking folks.

3. $80.00: WTI Crude Oil has shown price velocity lower today again, this after another flip-flop in behavioral sentiment was sparked by the announcement this weekend of a ‘rough framework’ agreed upon by Iran and the U.S. The Strait of Hormuz is seemingly quiet for the moment. At this point WTI Crude Oil price reversals are beginning to look like a well practiced dance routine. What will the next steps look like?

2. Forex Freakout: USD/JPY traders are listening to a myriad of narratives regarding the BoJ’s intervention. All experienced large players in the USD/JPY had to know an intervention was coming. While folks are pointing to the N.Y Fed and U.S Treasury selling of positions to bolster the JPY last week, they apparently need to be reminded the Treasury had the N.Y Fed start preparing the groundwork for such maneuvers earlier this year with steps including the ability to check on and counter USD/JPY Forex rates in January.

While folks are accusing the Fed/Treasury of hurting the USD, they should note the move is to counter weaker JPY which Treasury Secretary Scott Bessent likely had been pressed by ‘higher ups’ to manage in order to make sure Japanese products didn’t become too cheap in the States. There had been at least two other interventions in the past handful of months from the BoJ, as of this writing the USD/JPY is near 156.600.

1. Unilateral: President Trump’s decision making has become bewildering entertainment as he practices a comedic like opera trying to convince people about his opinions which he seems to change relentlessly. President Trump should learn the Art of Sparse Talking. Will the Republicans harness the President after the mid-term elections?