Forex Volatility as Central Banks, GDP, U.S Equities Shadow

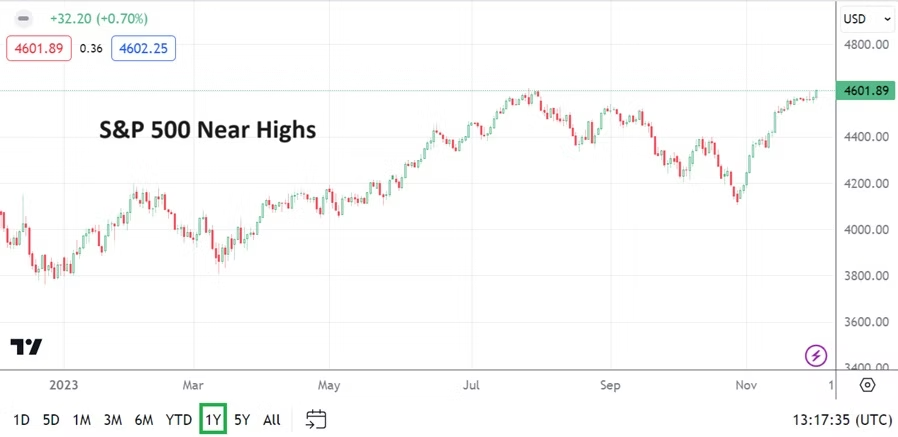

Perhaps it is good that today will see a lack of important economic data which will affect the markets. It might give a chance for day traders to relax and to gauge the thinking of financial institutions and investors before Central Banks, and important growth and inflation numbers shift behavioral sentiment later this week. While Forex has remained a minefield, U.S equity indices have soared to record heights. More volatility will come.

Risk assessment is always critical, it needs to be mentioned the Shanghai Composite Index is again facing severe selling pressure. This is a direct result of foreign investors losing faith in China’s economic policy and political maneuverings. The slump in Chinese equities is also hitting the Hang Seng Index in Hong Kong badly. Deflation is a legitimate fear in China. The dual consequences of a failing housing sector and crumbling equity values is harming Chinese citizens.

While the strong selloff in Chinese equities would have caused a massive amount of reaction in the global markets a few years ago, the ability to shift assets elsewhere by foreign investors who were active in China has likely reduced potential knock on effects in other global equity markets. It must also be pointed out that China continues to sit on a massive amount of USD holdings. China is a large investor in Africa and their attempt to steer influence there remains abundantly clear.

India has directly benefited from the outflow of investments from China. A look at the Nifty 50 Index shows the upwards momentum India’s equity market has enjoyed as it has started to attract more direct foreign investment. The ability of the India stock market to go up while China struggles is a barometer worth studying. Outflow vs. inflow.

Monday, 22nd of January, U.S Conference Board’s Leading Index – the reading is not at the forefront of consideration for investors, they will be watching the results of U.S Treasury yields and stock indices more closely than this report.

Tuesday, 23rd of January, Bank of Japan Monetary Policy Statement and Outlook Report – no major change is expected from the BoJ quite yet. The USD/JPY has been volatile and provided a solid trend upwards since the start of January. Day traders looking for a reversal lower to develop should be extremely cautious. Data from Japan has been mixed and the BoJ is likely to remain conservative. The weaker JPY helps exports from Japan it must be remembered, but it also may factor into inflation creeping into the Japanese economy.

Tuesday, 23rd of January, New Zealand Consumer Price Index – the inflation report is expecting a result of 0.5%, which would be below the previous result of 1.8%. The NZD/USD has taken a bearish dive since late December. Like all major currencies the New Zealand Dollar remains USD centric. Volatility in the NZD/USD may occur via the inflation numbers from New Zealand, but like the USD/JPY it may find its biggest impetus coming from afar – U.S data and the Federal Reserve outlook.

Wednesday, 24th of January, E.U and U.K Flash Manufacturing and Services PMI reports – Germany and France are anticipating slightly better Manufacturing Purchasing Managers’ Index numbers. Services numbers are expected to be slightly weaker from Germany. Solid results from these combined publications could help the EUR/USD create a bit of bullish momentum.

The U.K numbers via their Manufacturing PMI is expected to be slightly better than the previous outcome, but the Services number a bit worse. Economic data from Britain remains mixed to lackluster. Higher inflation numbers last week did the Bank of England no favors. The GBP/USD will be affected briefly by the results, but trading in the Forex pair is likely to remain geared towards thoughts about U.S data coming this Thursday and Friday.

Wednesday, 24th of January, Bank of Canada Rate Statement and Monetary Policy Report – the key lending rate from the BoC is expected to remain unchanged. However, Canadian economic numbers have been problematic, and while the BoC may want to wait for the U.S Federal Reserve to move first regarding interest rates, critics of the BoC are becoming louder. The USD/CAD will react to the Bank of Canada’s rhetoric, but unless there is a major surprise the currency pair will remain heavily USD centric.

Thursday, 25th of January, European Central Bank Main Refinancing Rate and Monetary Policy Statement – the ECB is expected to provide no major changes. The 4.50% interest rate is anticipated to stay in place. The ECB will likely ‘sound’ a calm tone and say while improvements are being seen in the E.U, that areas of difficulty remain but are understood and being managed.

Thursday, 25th of January, U.S Advance Gross Domestic Product – the key growth number from the U.S is anticipated to show a gain of 2.0%. This number will get a reaction in Forex, equities and bonds. The Federal Reserve’s FOMC meeting is next week and this GDP result will factor into their monetary policy rhetoric. Because it is an election year in the U.S, this number will also get an additional ‘sounding board’. Day traders should be careful before and after the noise caused by this growth report.

Friday, 26th of January, U.S Core Personal Consumption Expenditures – the vital inflation number carries an estimated gain of 0.2% before its release. As much as the Fed watches the GDP number, the inflation result via the Core PCE is a huge component of the U.S central bank’s thinking. The USD will react to this report and Forex traders should brace for a reaction from financial institutions. If the number is weaker than expected the USD could find selling momentum, if the number is stronger more USD strength could be seen. Folks looking at the GDP and Core PCE reports should also look for potential revisions to previous months results, which could cause another wave of volatility in the markets if they are significant.